The Ukrainian Retail Association presents the fourth annual analytical review of the Ukrainian e-commerce market and audience’ features of country’s leading online-stores in different segments

All retailers, including those working in online-trading, try to get to know its customers as best as possible. And at the same time it tries to compare: how its client differs from a competitor’s buyer, and who is generally interested in purchasing this or that product on the Internet. It is much easier for online-stores to collect and analyze such information than its offline-counterparts: modern services provide an opportunity to get almost any data.

What was considered

We set ourselves the goal to prepare the largest-scale analysis of the Ukrainian e-commerce market once a year, making an approximate portrait of domestic consumers buying goods online, as well as analyzing indicators of leading online-stores in different segments.

And then the obtained data compare with results of last year’s research and find out what trends prevail in Ukrainian e-commerce, what online-players should pay attention to, how consumer behavior has changed over the year, market coverage shares, and so on.

We used paid versions of services Similarweb and alexa.com, which were supplemented with data from open sources to collect information.

We prepare a detailed analysis for various e-commerce sub-segments in addition to the general report. We have allocated in a separate category department stores (such as Rozetka), where you can buy almost anything – from jewelry and lures to snowmobiles, yachts and professional equipment to avoid comparing players with incomparable indicators. At once, the report lacks classic marketplaces – olx, prom, and others – since it do not sell its own products, but act as a platform for contact between a buyer and a seller.

As was considered

The period from November 1, 2019 to October 31, 2020 was analyzed, since retailers of different profiles have different “peak” sales periods, and the selected time period makes it possible to cover all possible fluctuations in demand. The research looked at eight segments: department stores, electronics and gadgets, home appliances, fashion, sports goods, jewelry retail, children’s goods, cosmetics and drogerie. Each of it took into account several parameters: the users’ age, main login channels, devices used (PCs and laptops or smartphones and tablets), the number of unique visits and bounces, prevailing social chains in a particular segment.

There is no separate segment for portable electronics and gadgets this year, as most players have expanded its range far beyond this narrow specialization.

Why was considered

This report like any analytics allows online-retailers to learn about its strengths and weaknesses, to get acquainted with the portrait of the buyer and compare it with its own customer data. Besides, information about main traffic channels and most effective social chains will help adjust SEO- and SMM-promotion strategies to increase brand awareness and attract new users, assess the need and prospects for the creation and implementation of mobile applications and adaptive layout, and extract a lot of other useful information.

We hope you find our analytical report useful!

Ukraine

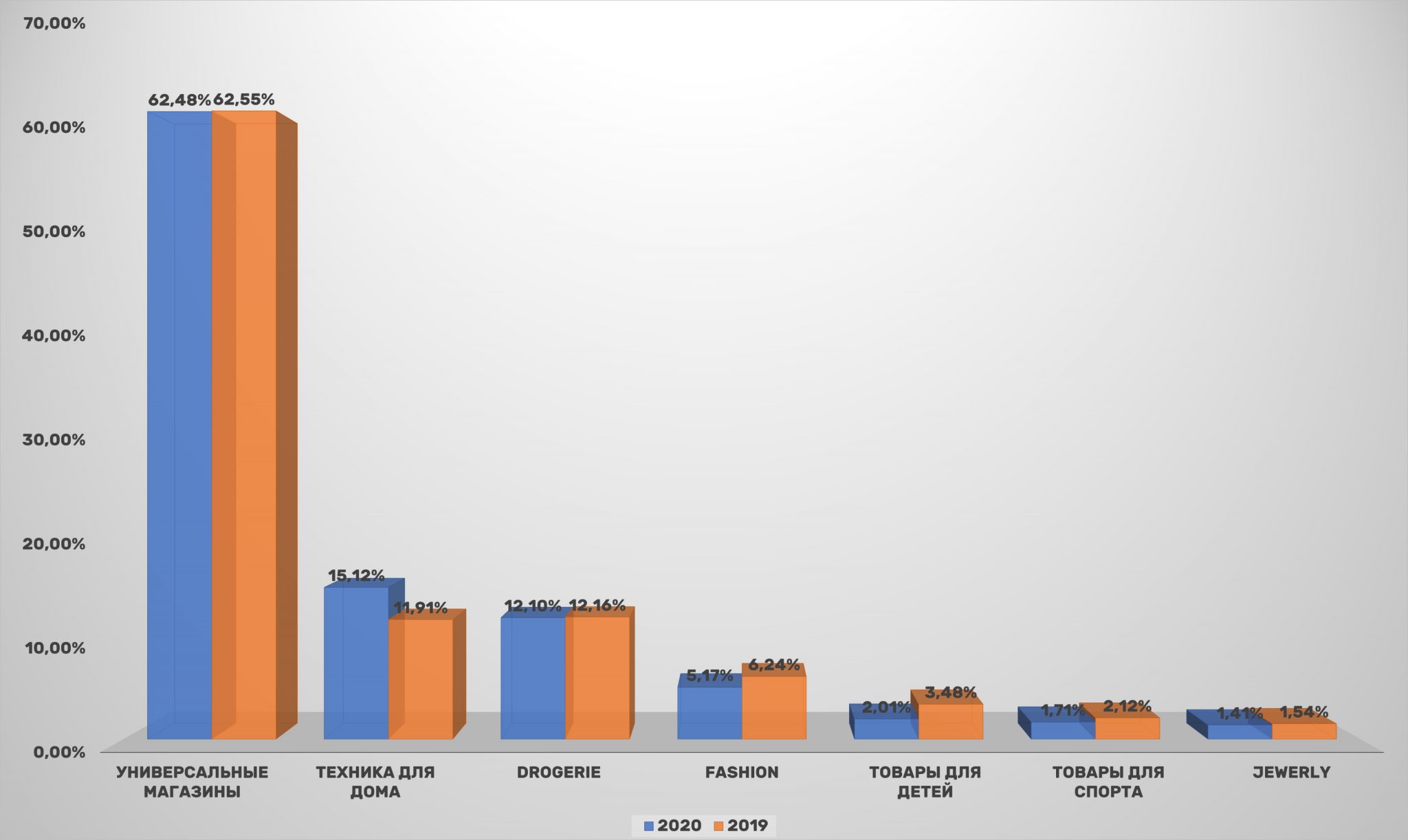

If we take domestic e-commerce as a whole, the most popular segment of online-stores remains unchanged: universal portals where you can buy everything – from toothpicks to gaming computers, as well as many other goods, including vehicles. Over the year since the last research, it practically did not change its audience coverage – 62.48% versus 62.55% UAnet users (revised data)

However, it still significantly outperform all other store’ categories combined.

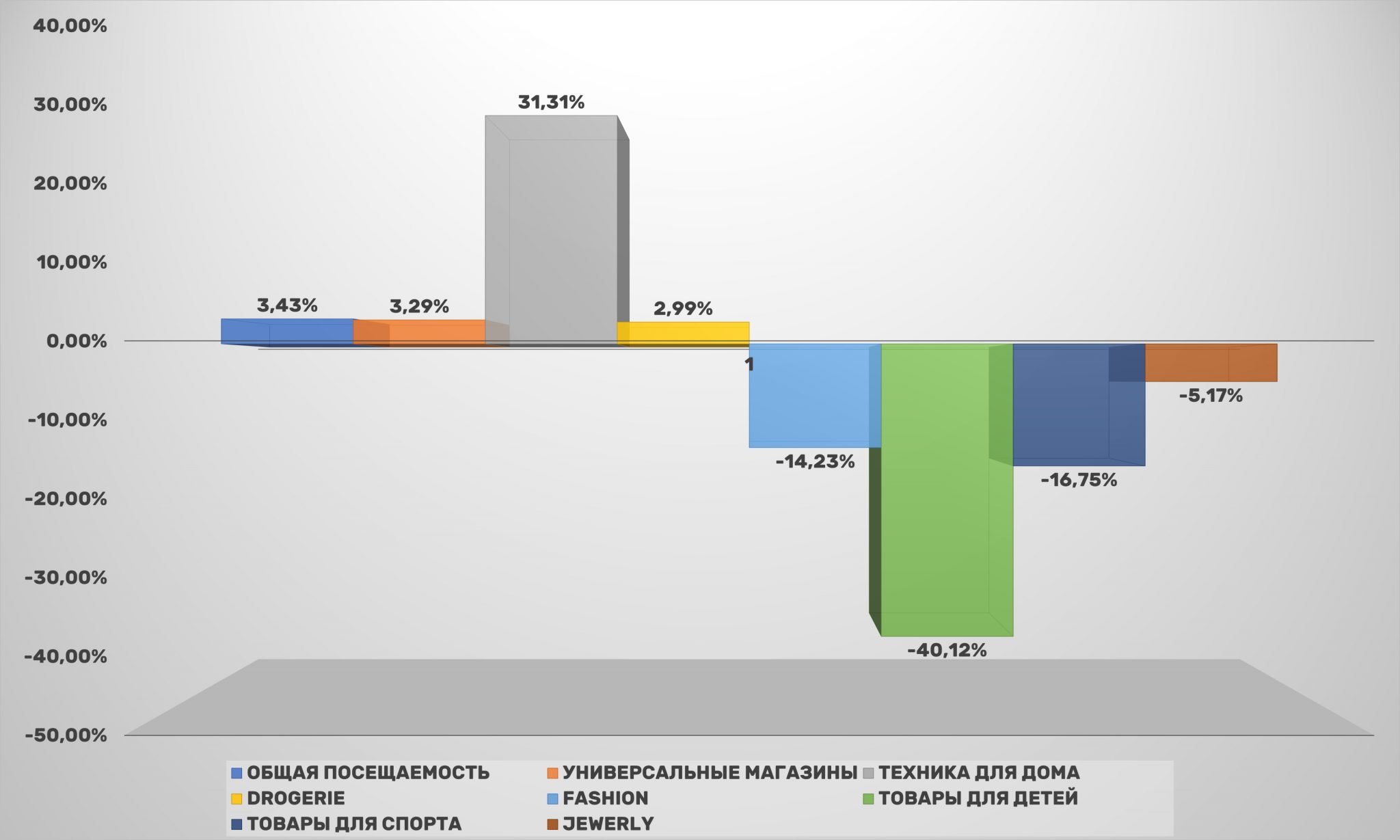

At the same time, other segments of Ukrainian online-commerce have undergone significant changes. Greatest success was achieved by online-shopping for home goods, which increased its audience reach by a quarter – from 11.91% to 15.12%. As a result, household appliances stores (Foxtrot, Comfy, Citrus and others) again surpassed the beauty and health segment in popularity.

This is due to the fact that during the pandemic and quarantine, people began to spend more time at home and less use of beauty products when “going out”. However, indicator 12.10% Ukrainian residents who went online would be the best in 2019, and in 2020 it guarantees a stable second place.

All diagrams can be enlarged by clicking on the image

The rest of categories have lost in coverage compared to 2019. Thus, the segment of goods for children sagged in absolute terms the most (more than 40% drop). It is followed by sports goods and the fashion category. If the subsidence of fashion-retailers can still be explained by the reduction in purchases by fashionistas who have become less likely to leave the house and change their outfits, then sports goods, on the contrary, according to various sources, are in high demand. One of explanations may be that these two e-commerce directions managed to achieve high conversions, and the drop in coverages does not affect sales growth in any way.

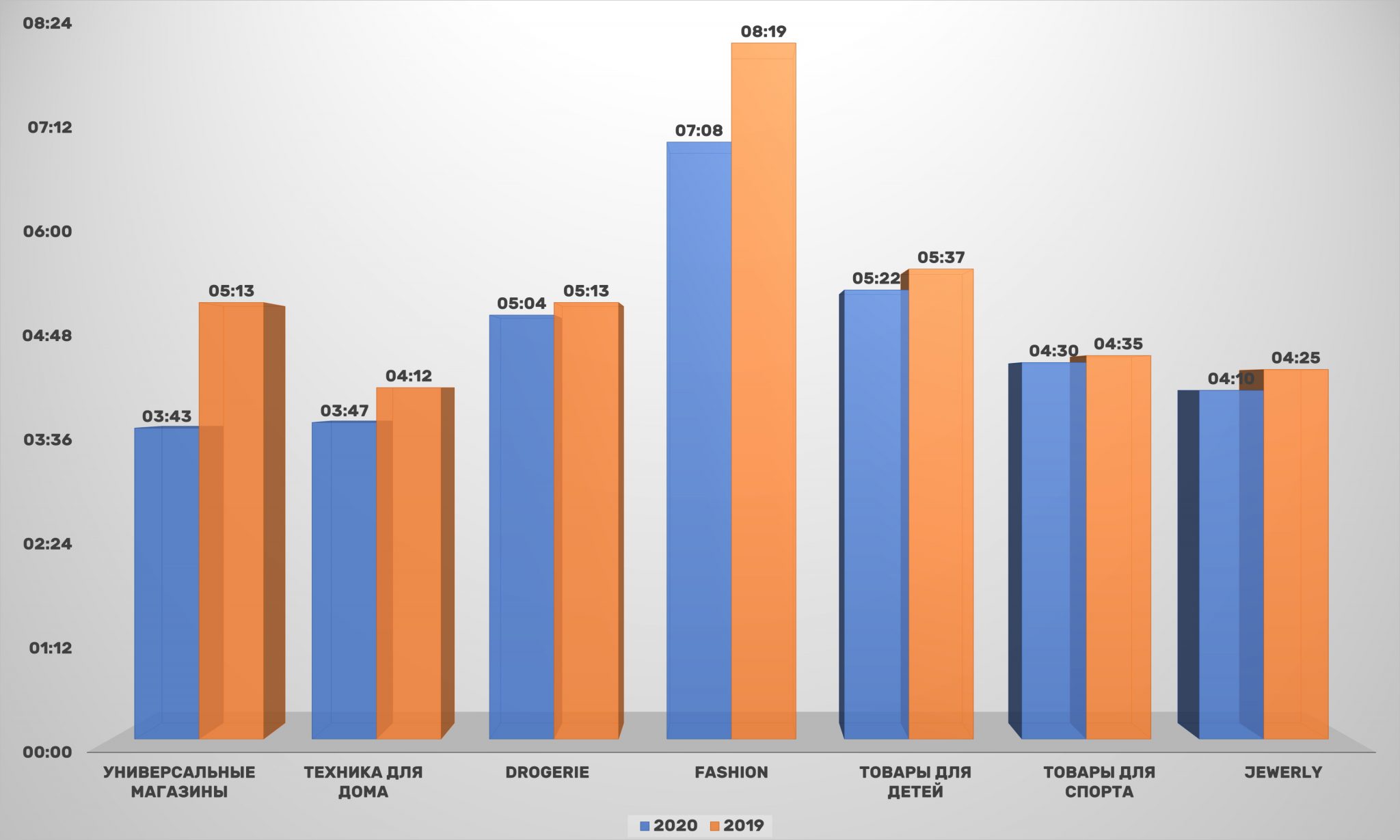

This is confirmed by other key indicators. So, other sectors are in the lead in time spent’ terms on the site and viewing ‘depth. The longest time users stay on websites of fashion-retailers: 7 minutes 8 seconds. This is less than a year ago, but it should be noted that the time spent on the site has decreased in all segments without exception. This may indicate that users are sufficiently familiar with online-shopping and are quicker to make a choice. So, goods for children are in second place, as before, where potential buyers spend on average 15 seconds less.

The third place in terms of duration is taken by cosmetics and drogerie segment, the fourth and fifth places are shared between sports goods and jewelry sellers.

Curiously, leaders in audience reach – department stores – are in last place in time spent’ terms on the site, just 3 minutes 43 seconds. Visitors spend a little longer on websites of home appliances’ retailers.

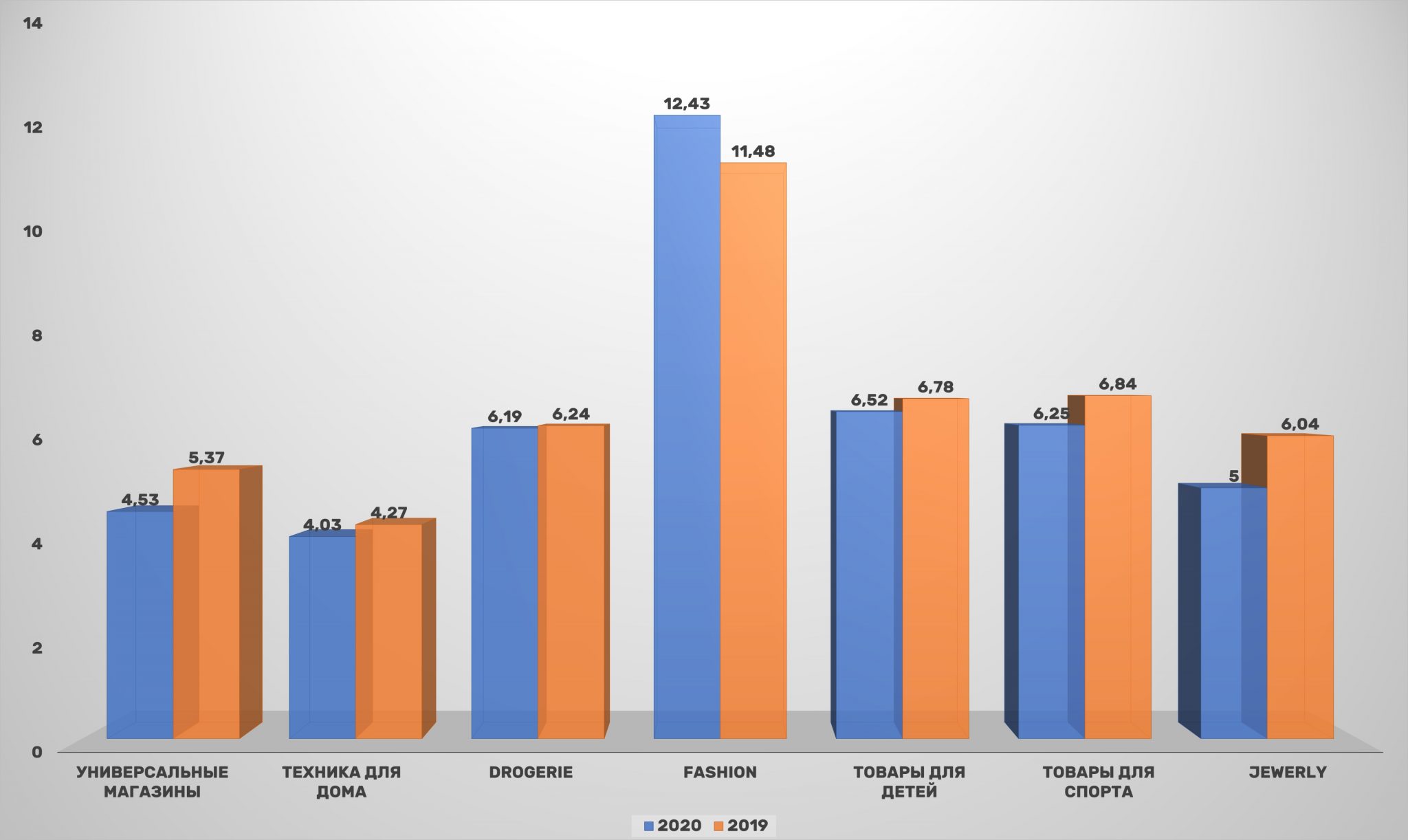

The viewing’ depth corresponds to the time spent on the site by fashion-retailers: on average, a user, to select a product they like, views more than 12 pages. For the fourth year in a row, this indicator has been steadily growing among sellers of clothing, footwear and accessories.

This is the only category in 2020 where the site exploration’ depth has increased.

A second place in viewing depth’ terms is now occupied by sellers of goods for children, and sporting goods have receded into the background. It turns out that Ukrainians have become even more careful in choosing a purchase for their children.

The number of transitions from page to page within the site is reduced for other online-retailers. Moreover, sellers of household appliances have the lowest indicator – only 4 pages. The fall continues for the fourth year in a row, what can’t but worry. For the second year, jewelry sellers also lose the viewing’ depth.

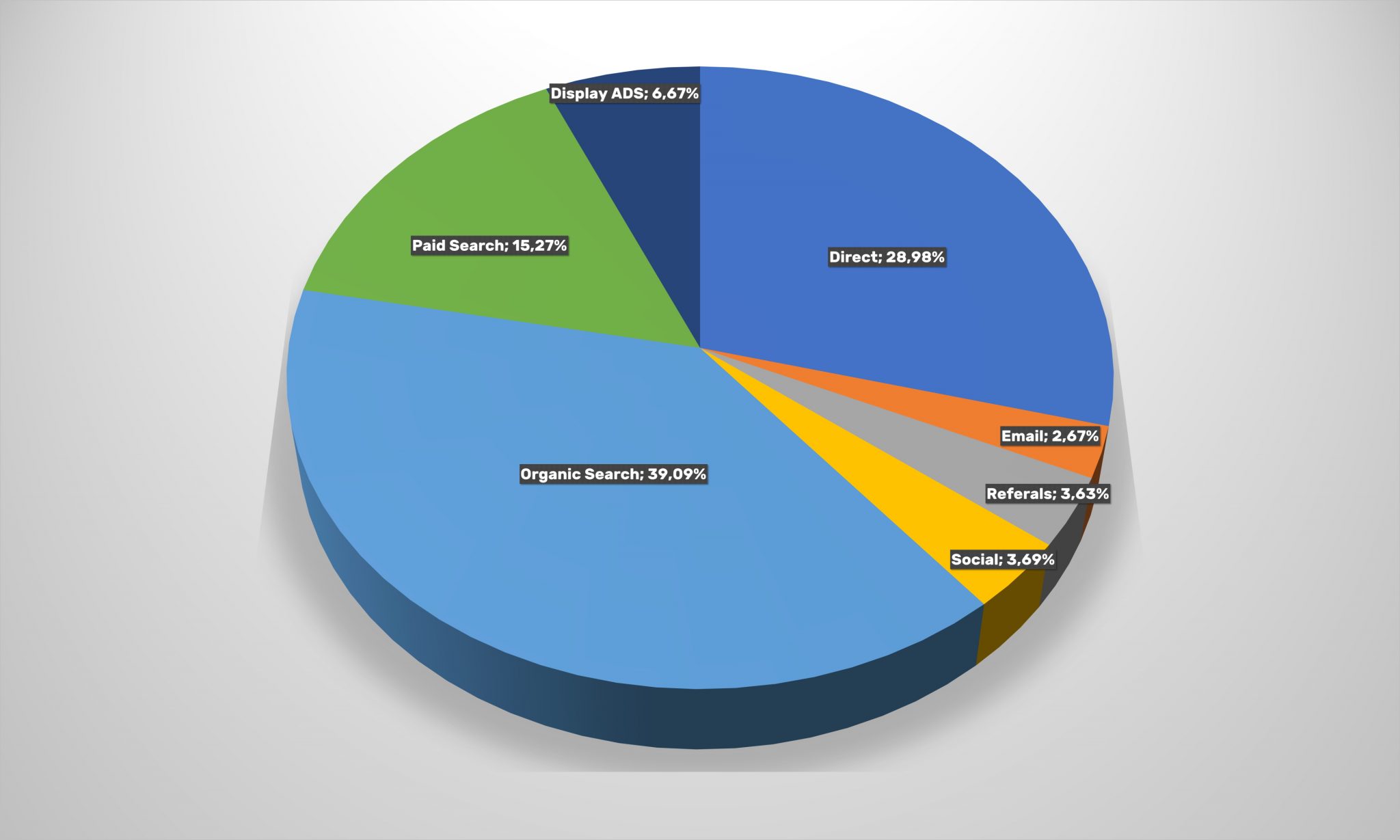

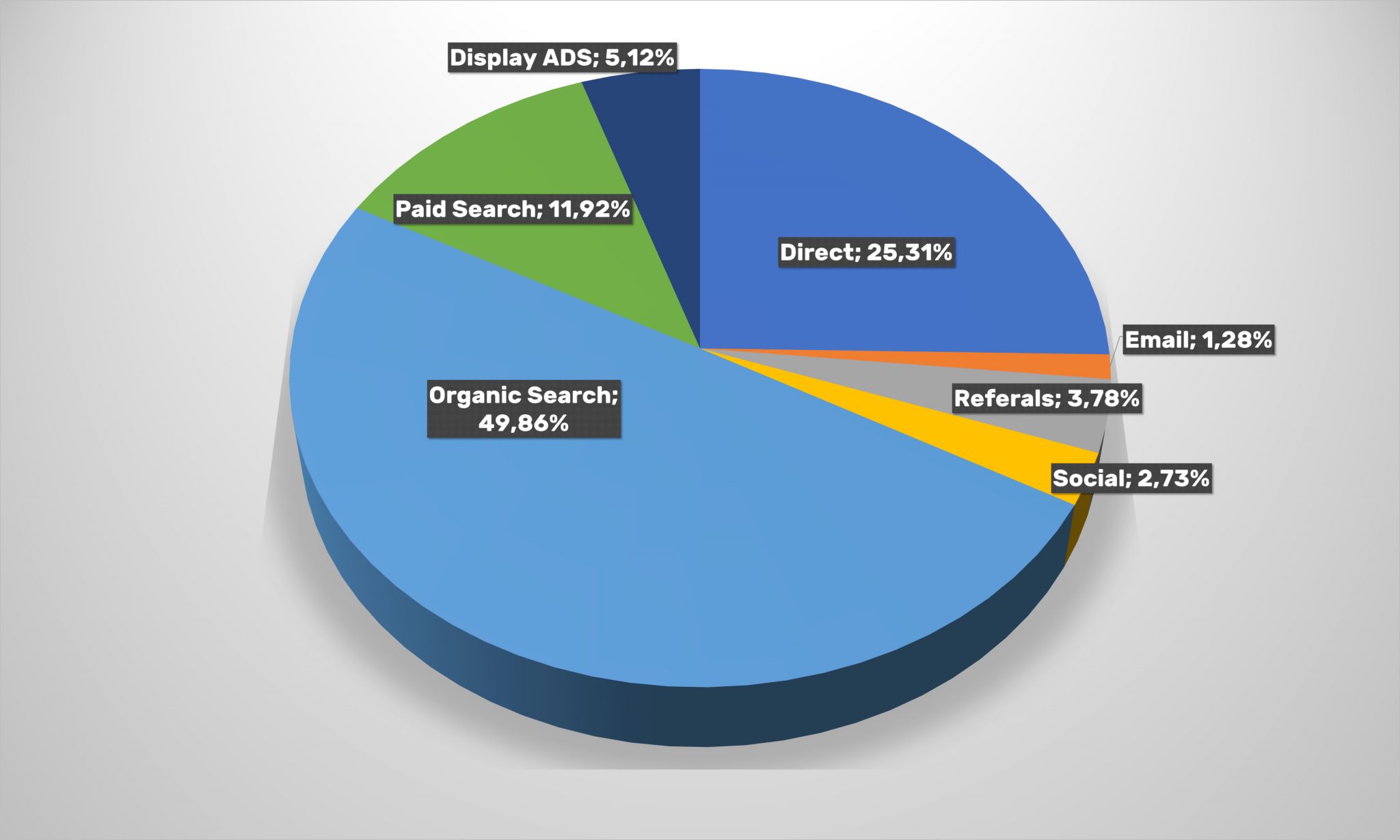

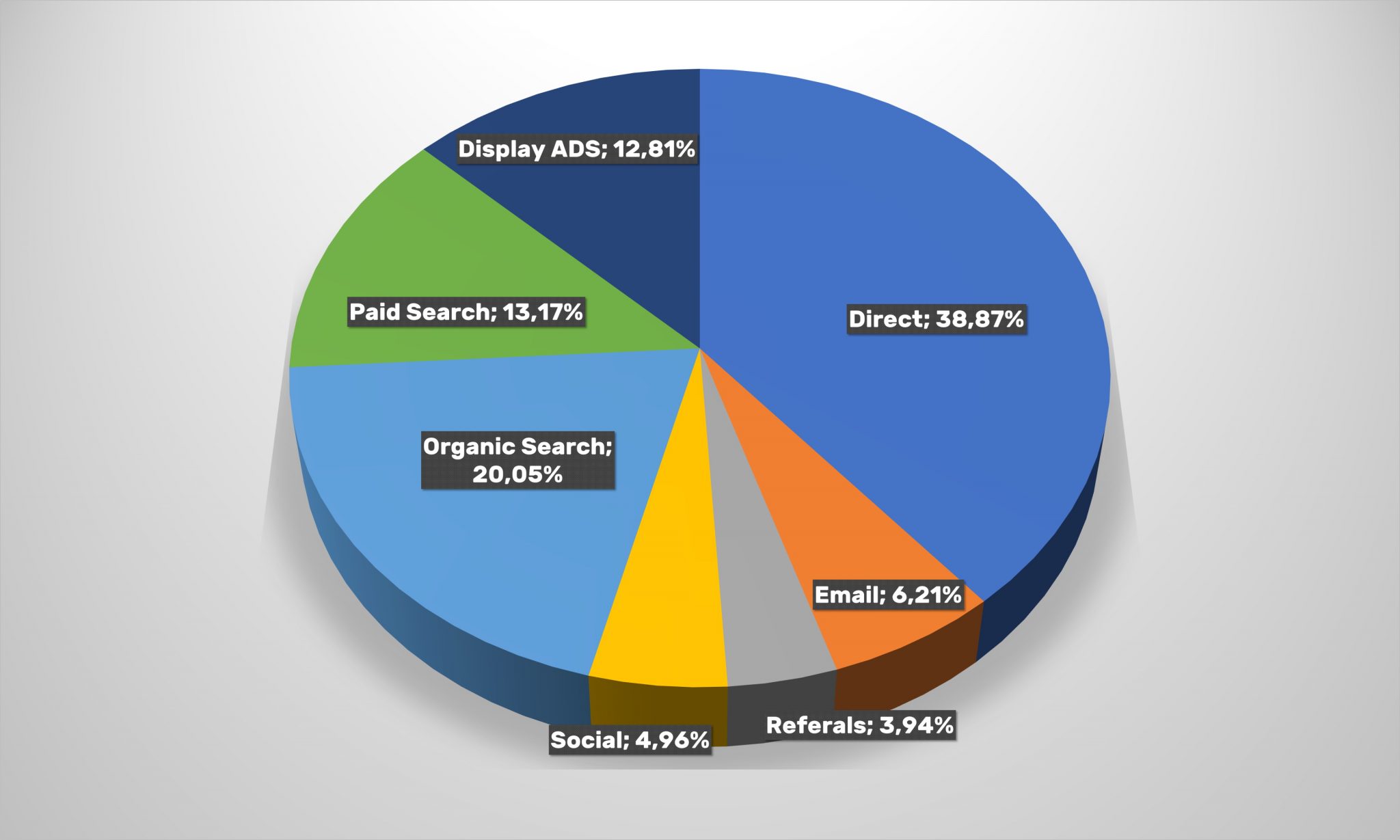

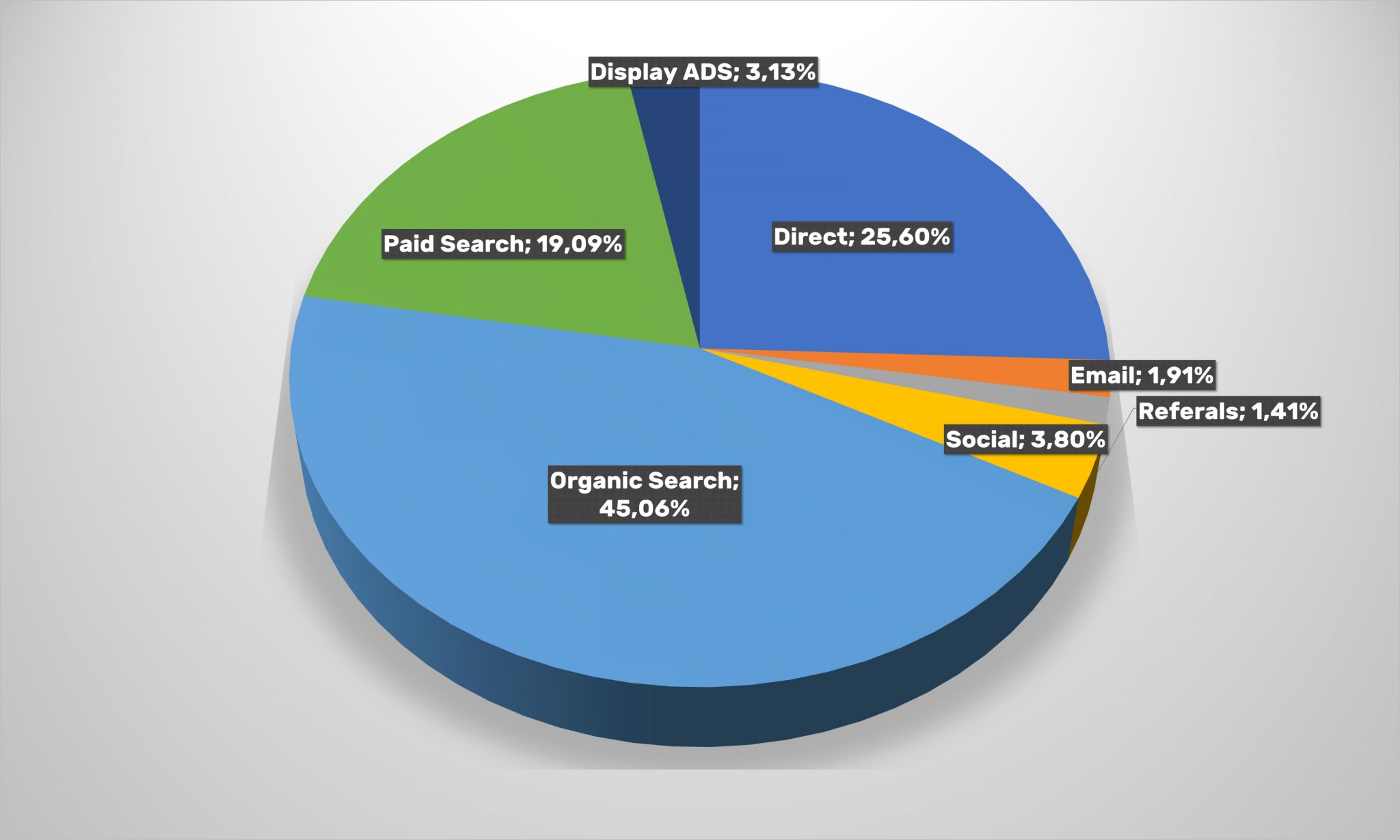

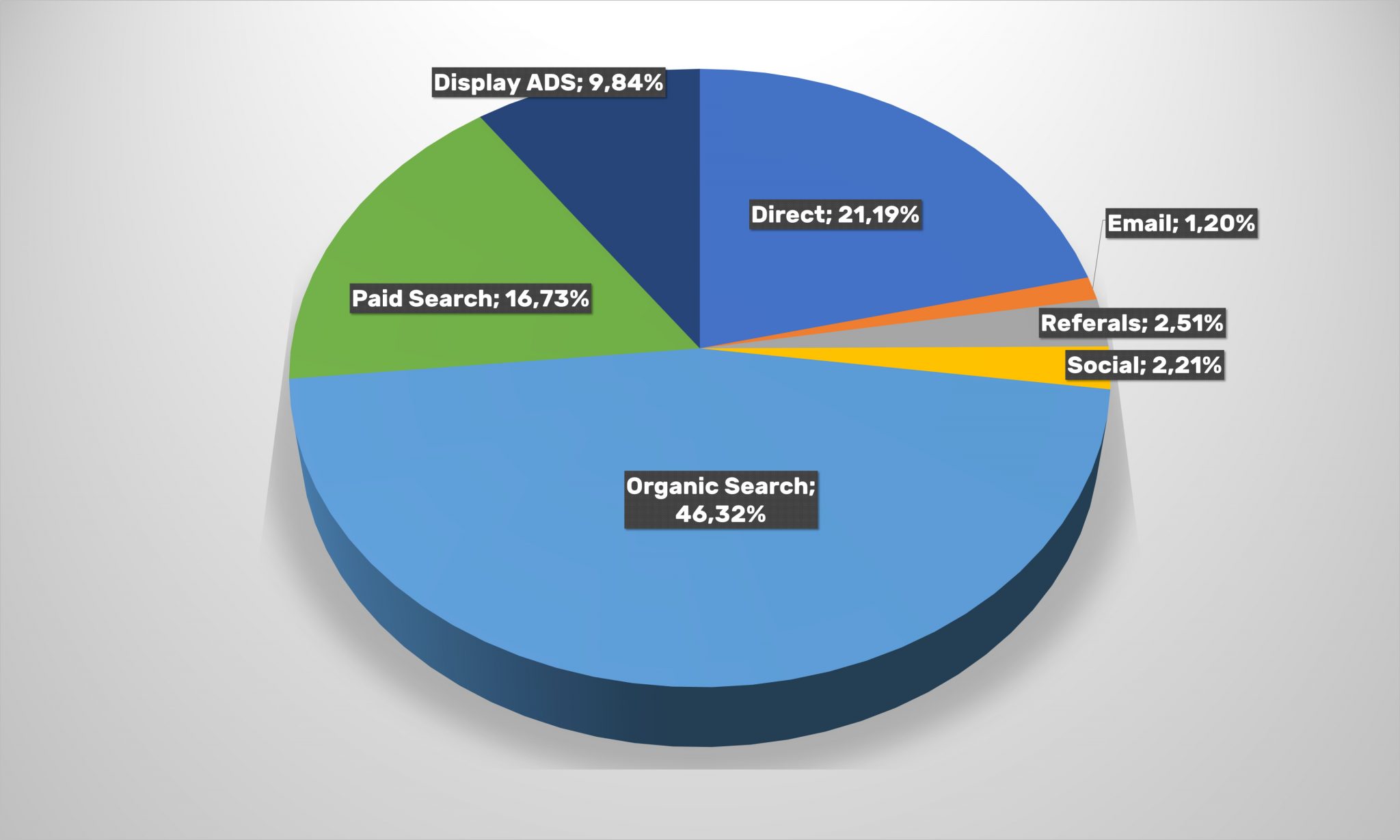

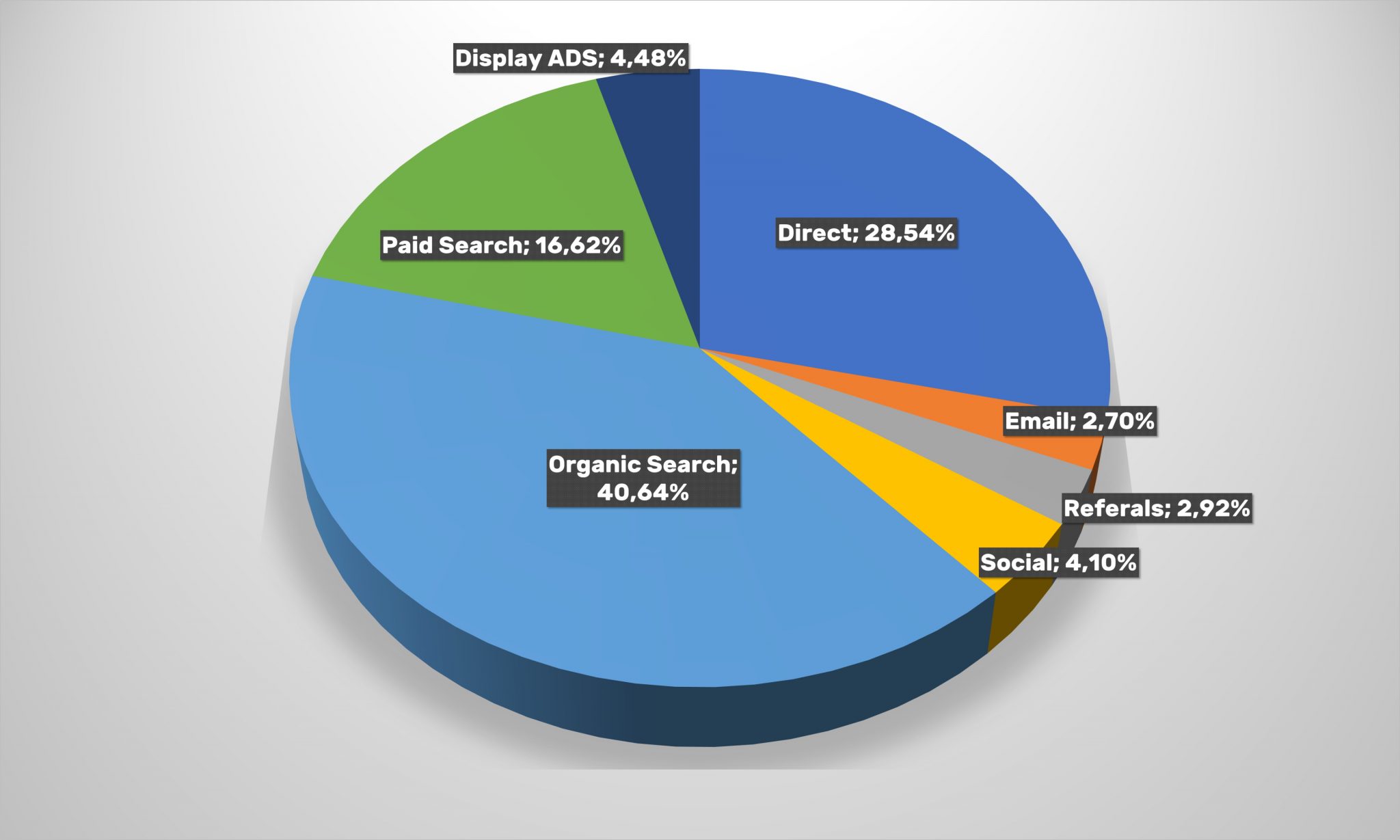

Let’s take a look at visit points, or how users get to retailer sites. As before, there are two main channels: organic search (on google and other search engines) and direct visits (direct, where the buyer goes directly to the store’s portal). The direct visits’ share continued to grow (+2 pp), while organic search managed to win back only a third of the drop in the previous period (+0.6 pp). The clicks’ share on paid contextual advertising and paid advertising itself has also slightly increased. But at the same time it is becoming an increasingly difficult task to lure users through e-mail newsletters or cross-links.

If we analyze traffic from social chains separately, then it continues to decline, providing only 3.69% conversions.

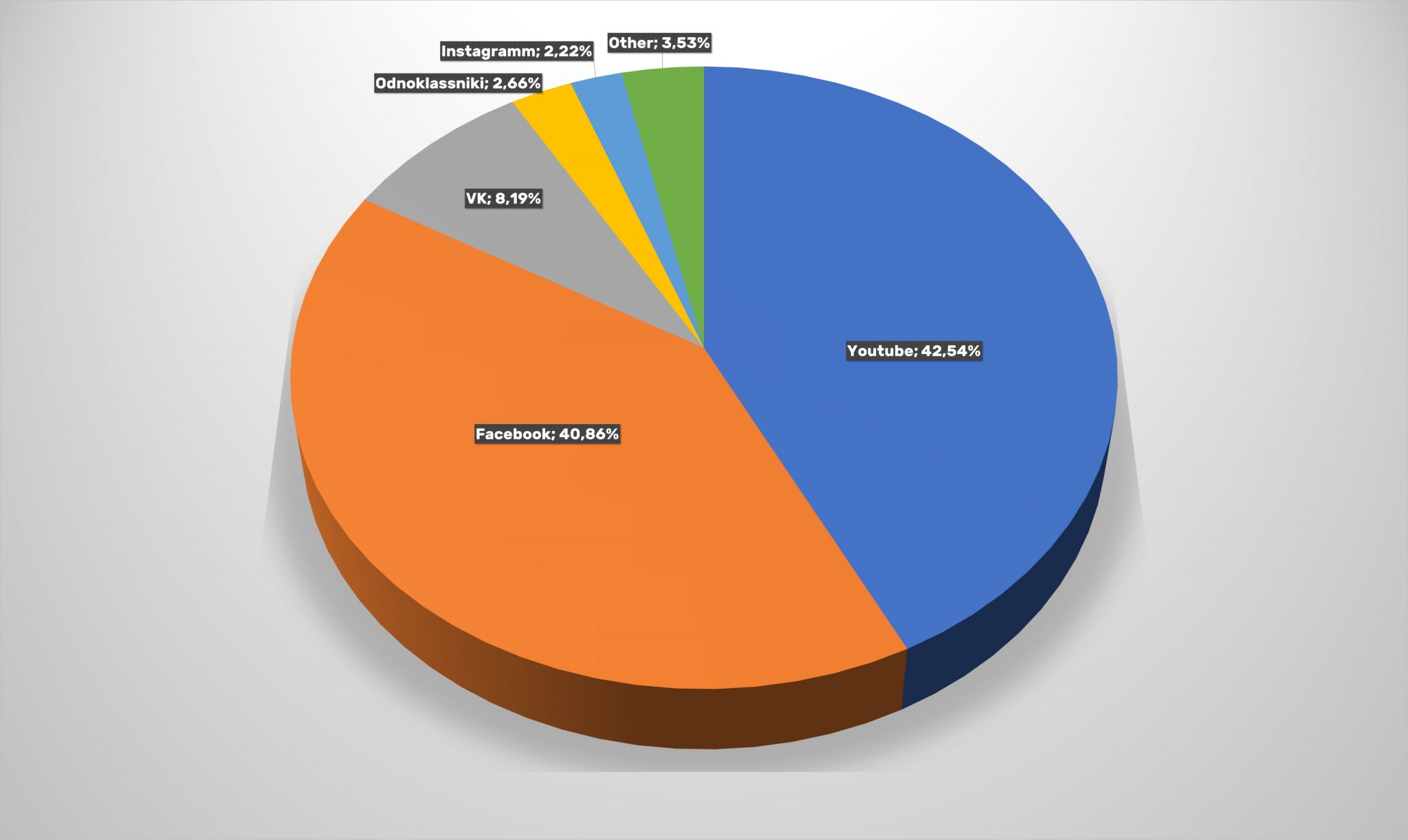

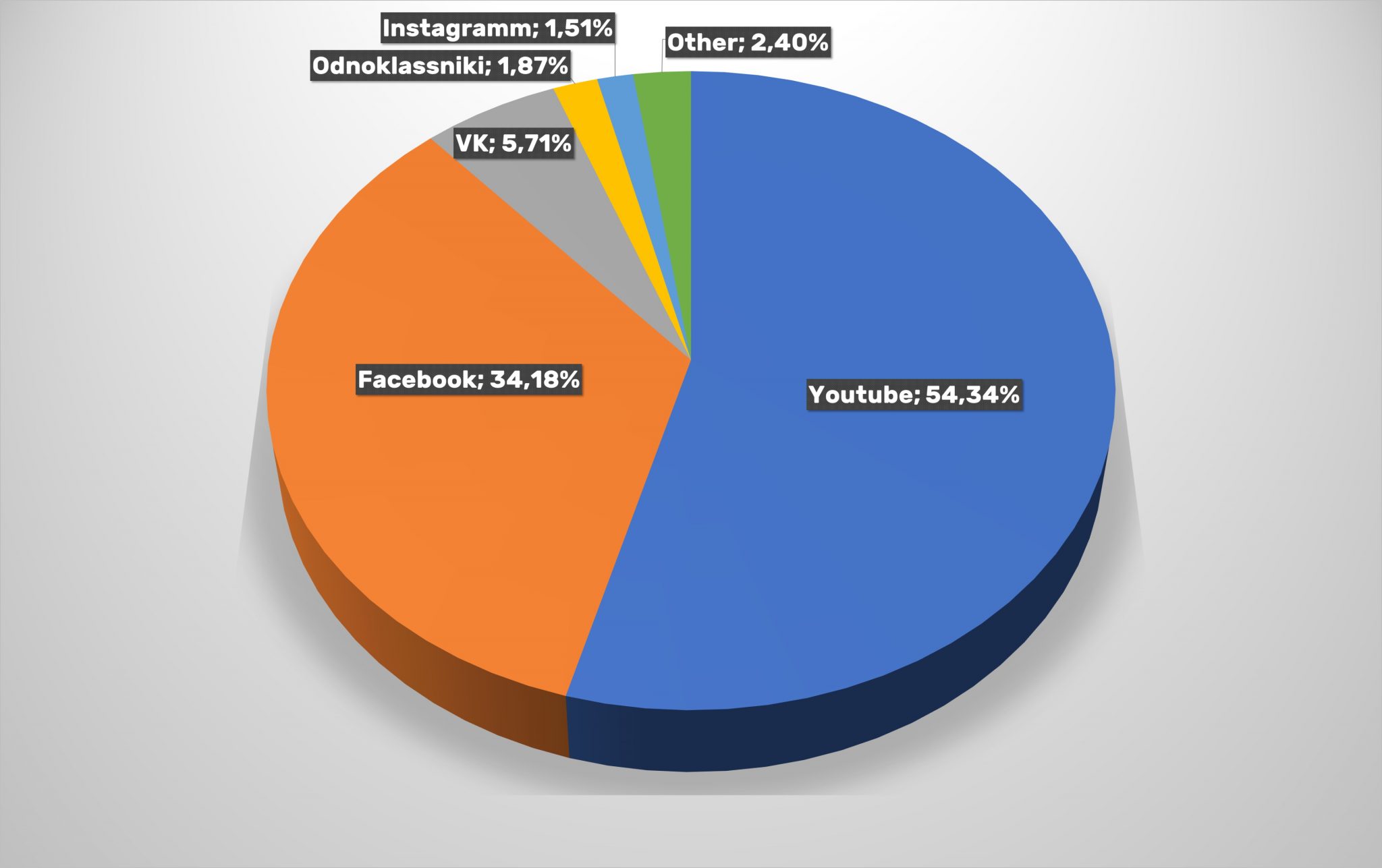

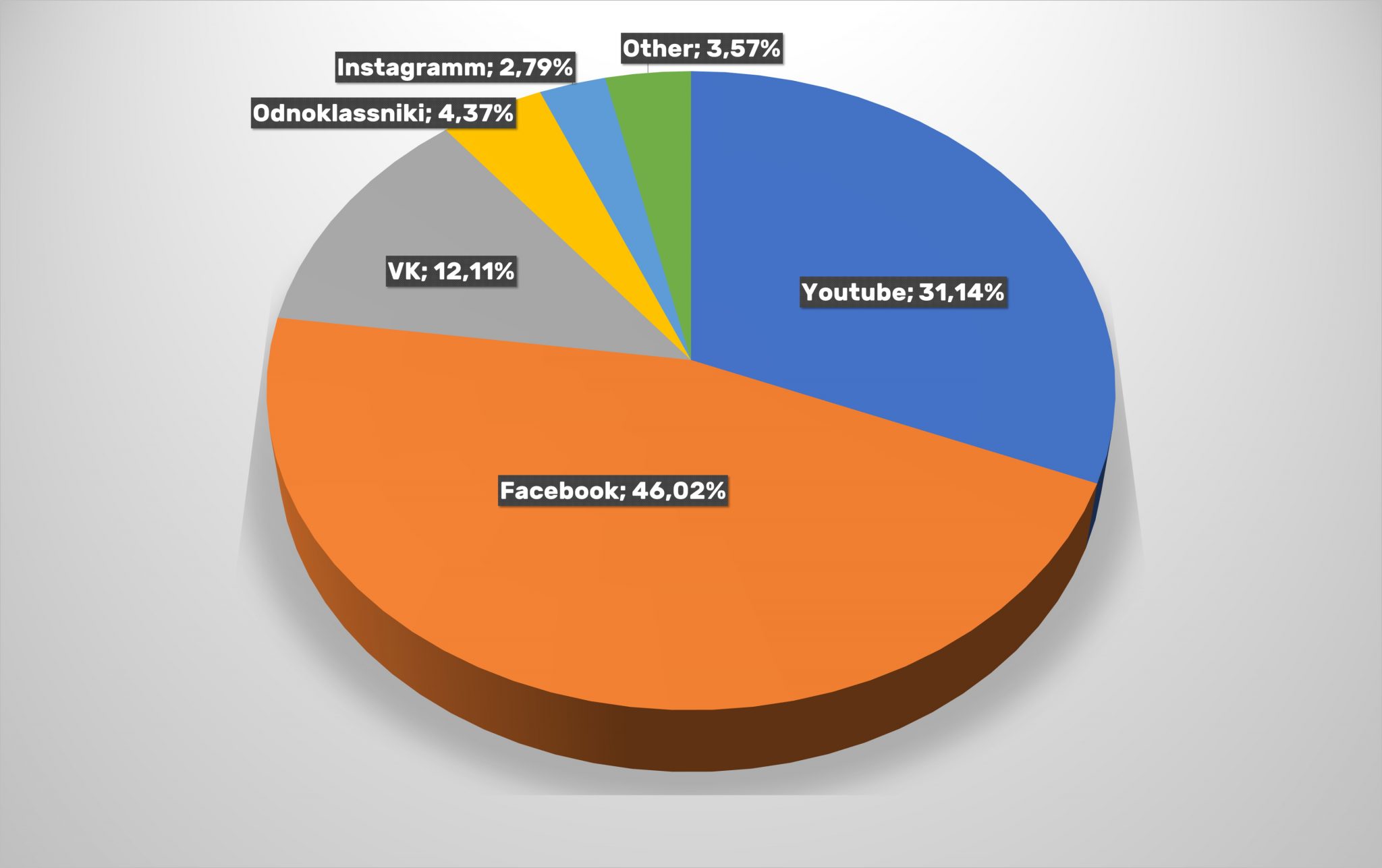

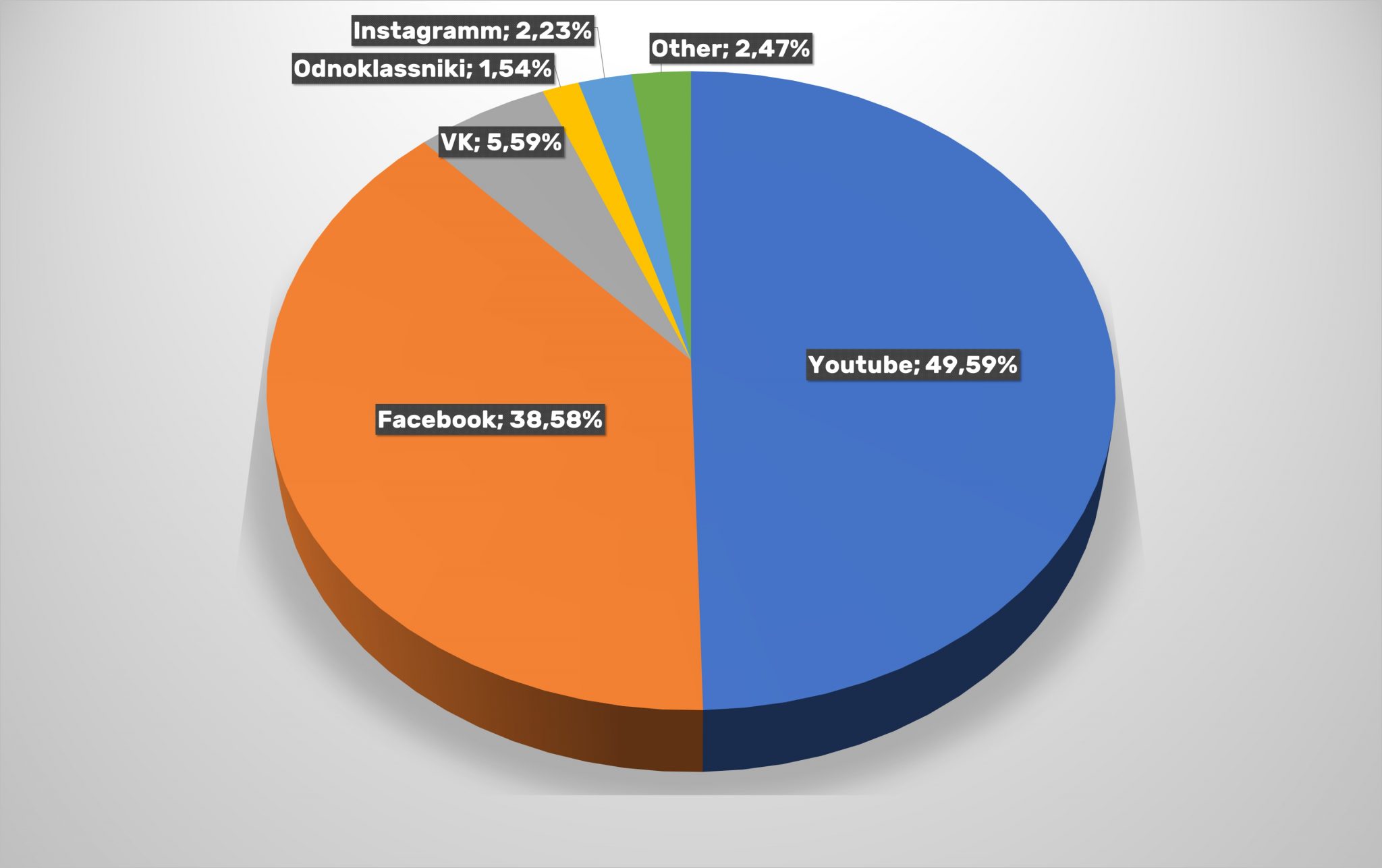

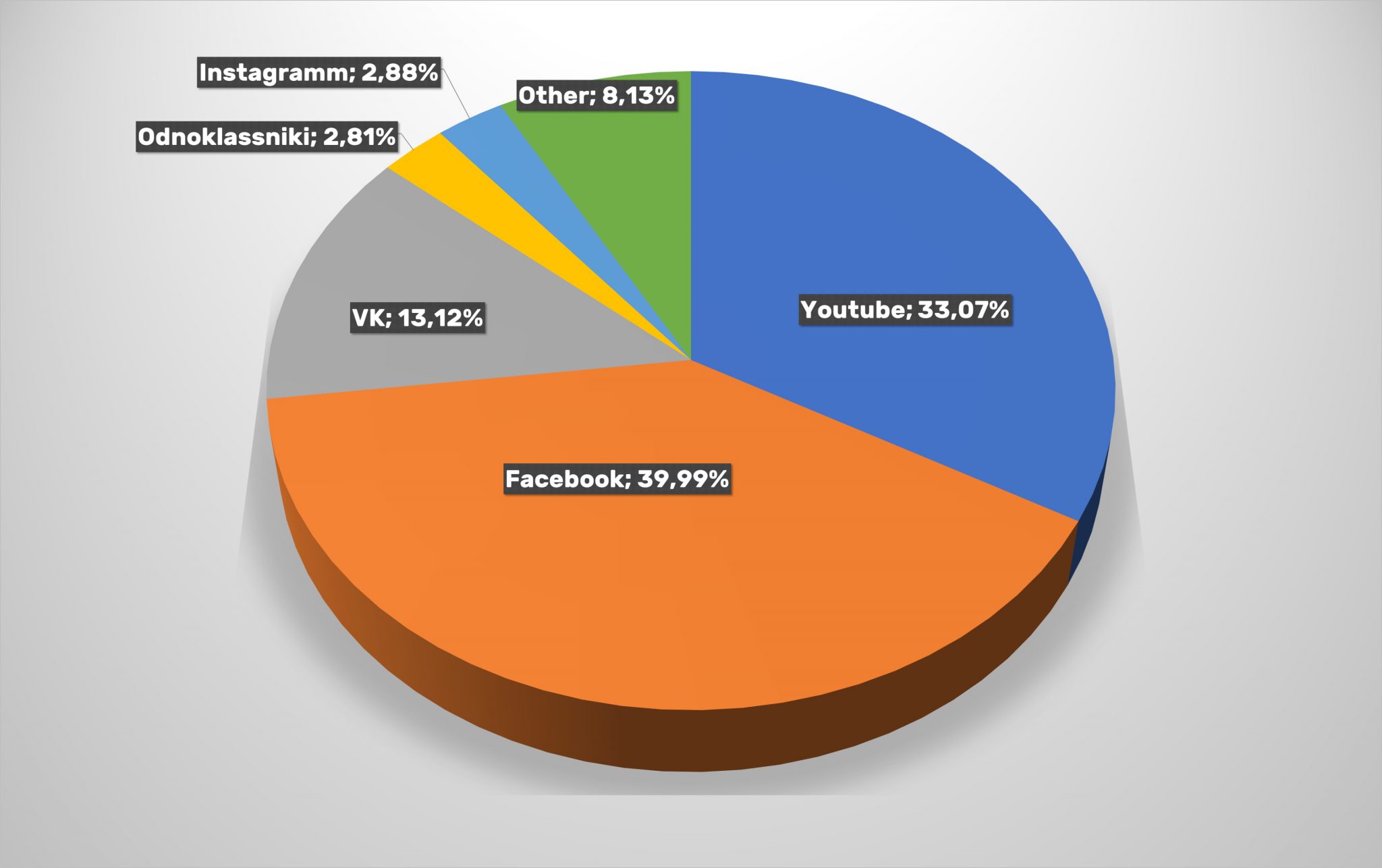

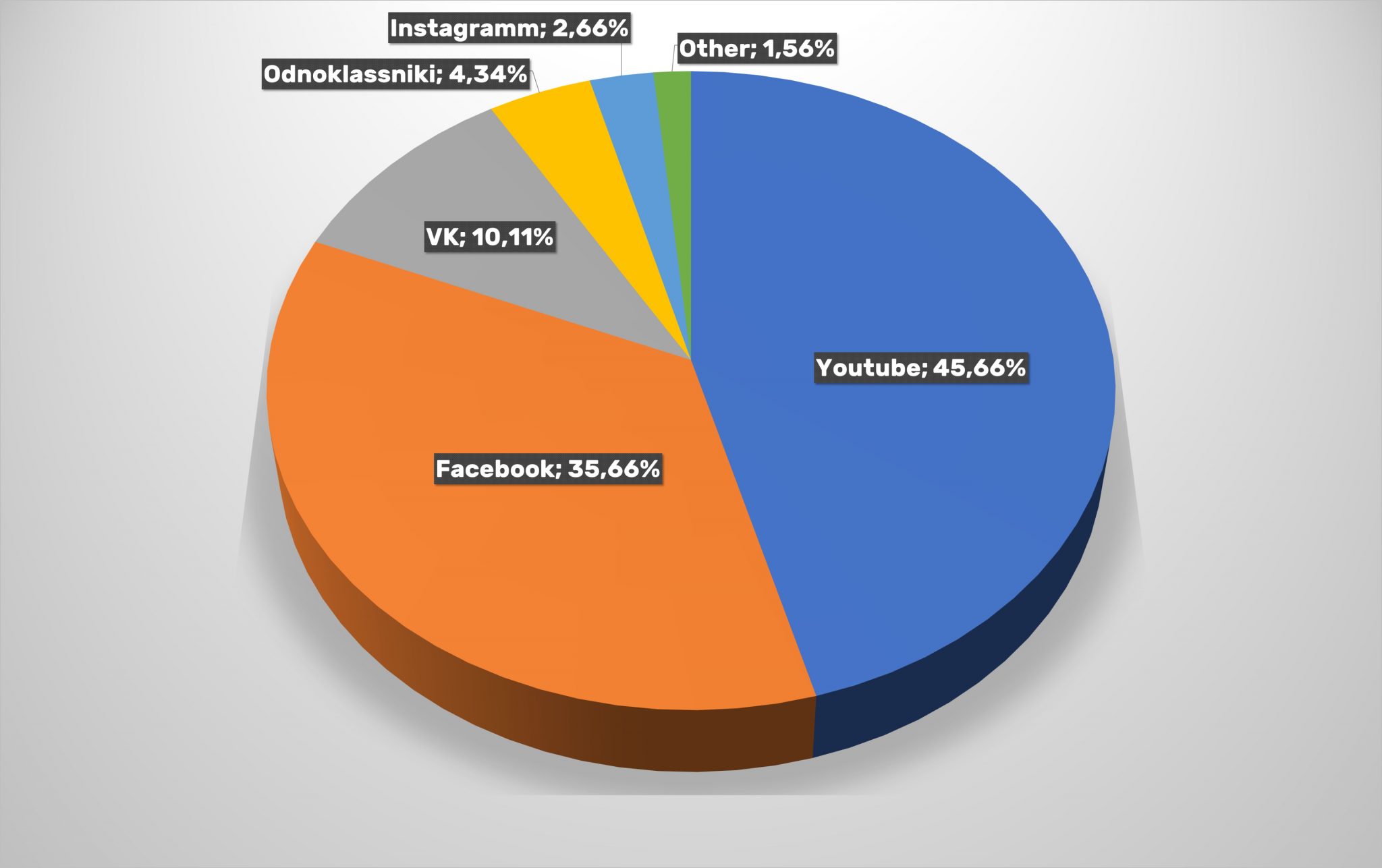

Facebook (40.86%) and YouTube (42.54%) are main traffic providers. Curiously, these two channels have reshuffled again: a year ago Facebook was in the lead with 43.31%, and YouTube provided 39.79%. This might be reassuring for marketers betting on video content, but given the overall decline in social click-through, pouring ad budgets into this space will likely require optimization.

Compared to 2019, the Vkontakte’ share has decreased – from 10.20% to 8.19%. The rest of social chains remain of little importance for attracting users to online-stores. Nevertheless, one cannot fail to note a noticeable increase in the number of conversions from Instagram, the share of which reached 2.22% – the highest rate in last four years.

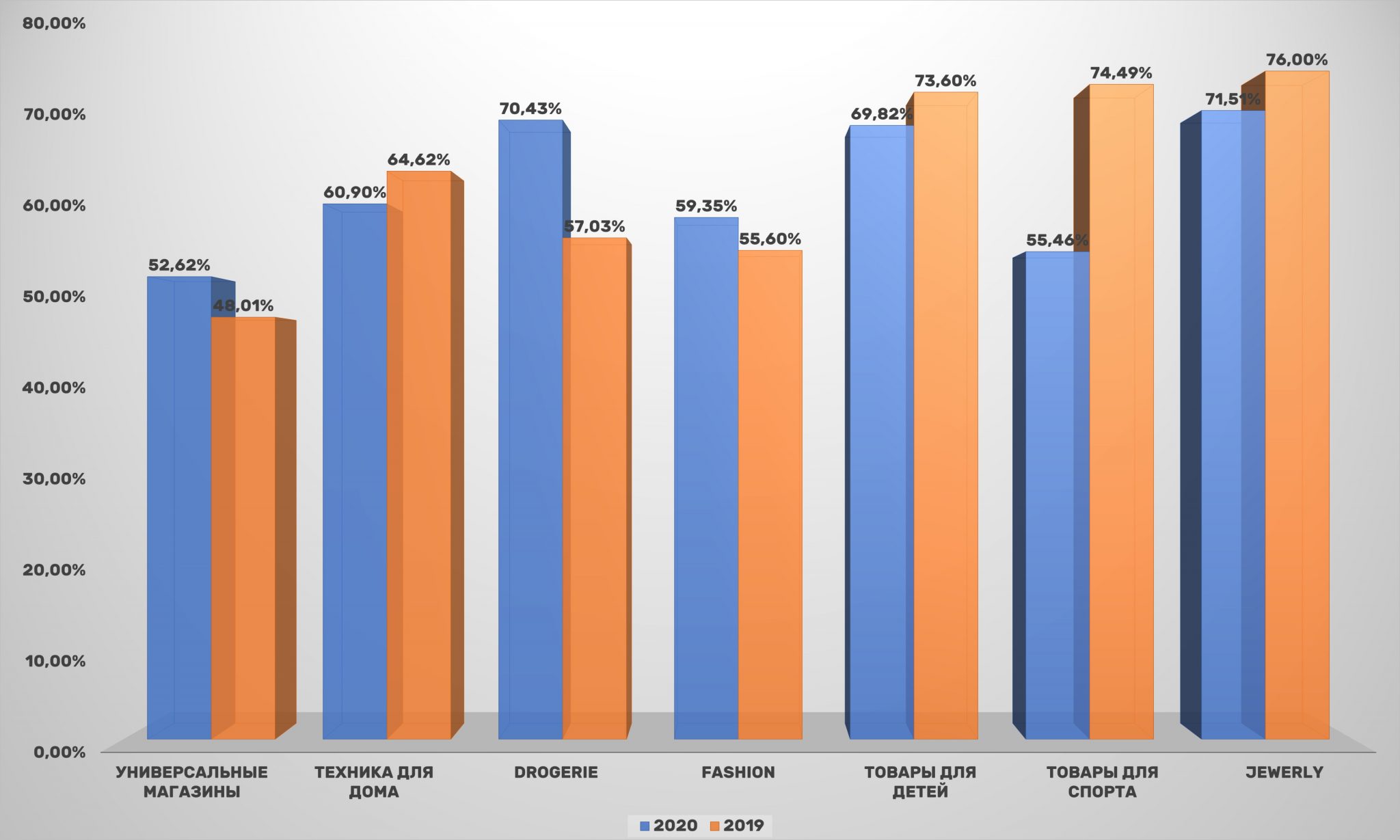

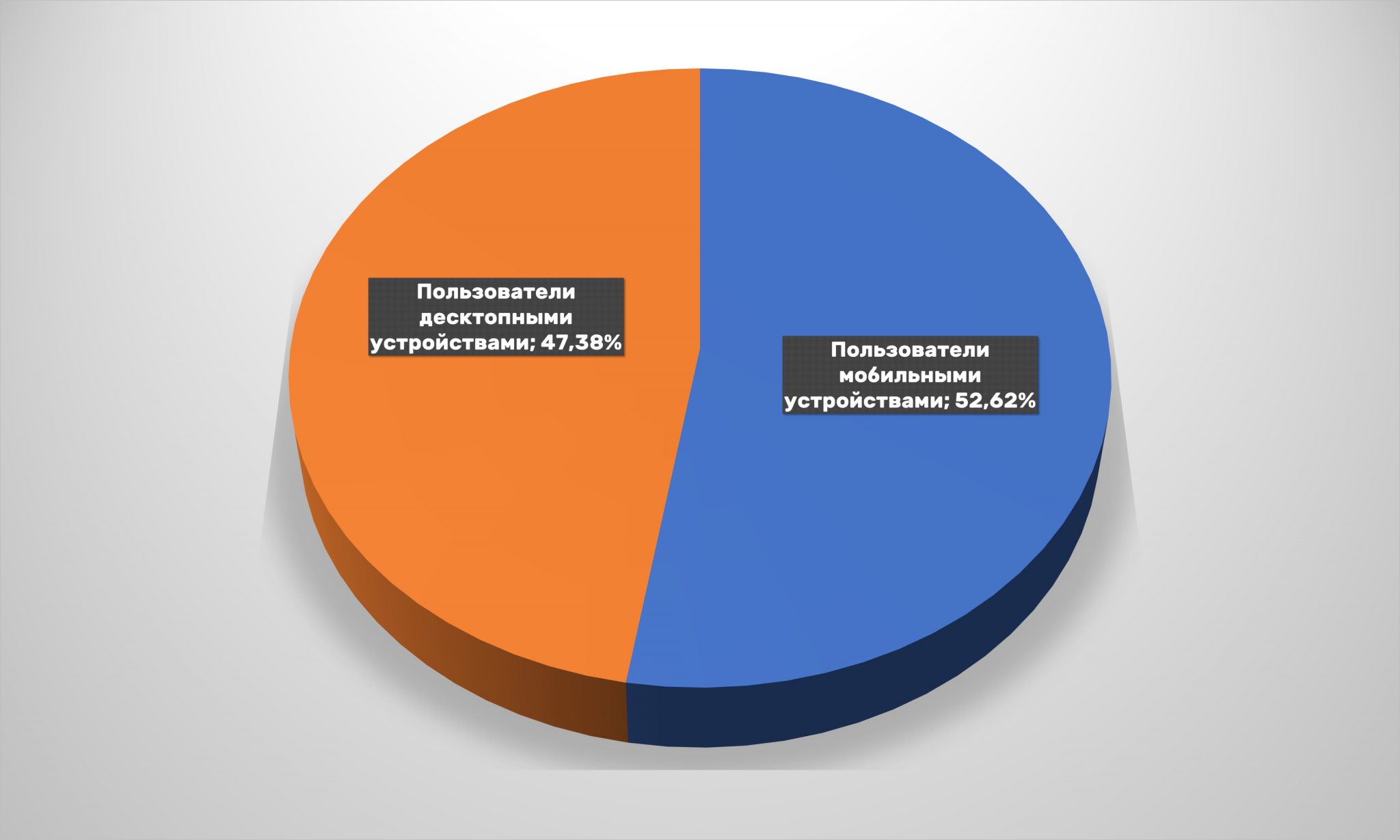

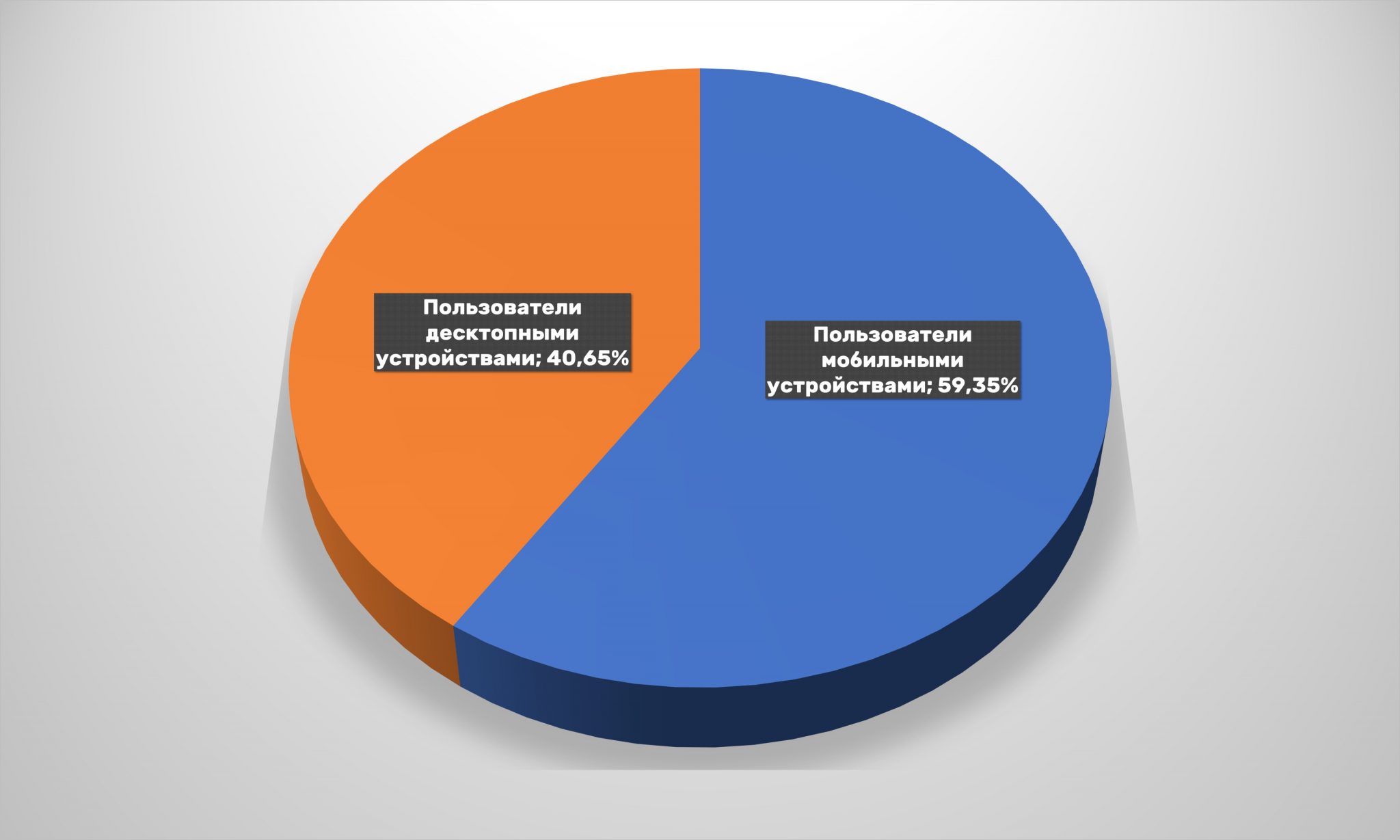

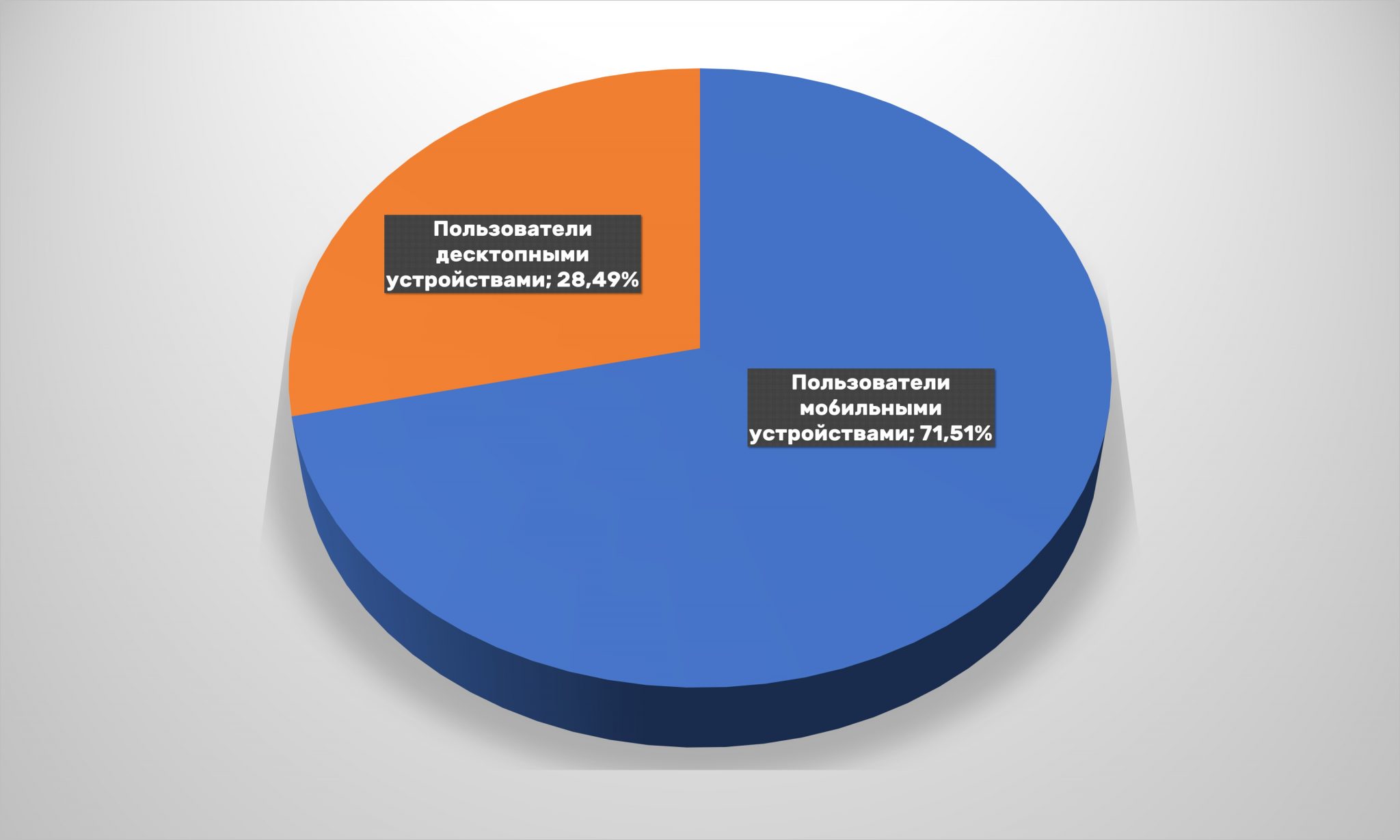

But the importance of developing the m-commerce direction has been confirmed for the second year in a row. However, after the restoration of the visits’ number via mobile devices in 2019 last year only three of seven sectors showed growth in traffic to online-shopping sites: drogerie, fashion and department stores. The biggest leap was made by sellers of goods for beauty and health: from 57.03% to 70.43%. Although the leader in m-commerce is still the Jewerly segment, despite a slight decrease in traffic.

Last year it was made least of all visits from mobile devices to sites of sporting goods’ sellers: 55.46% against 74.49% a year earlier.

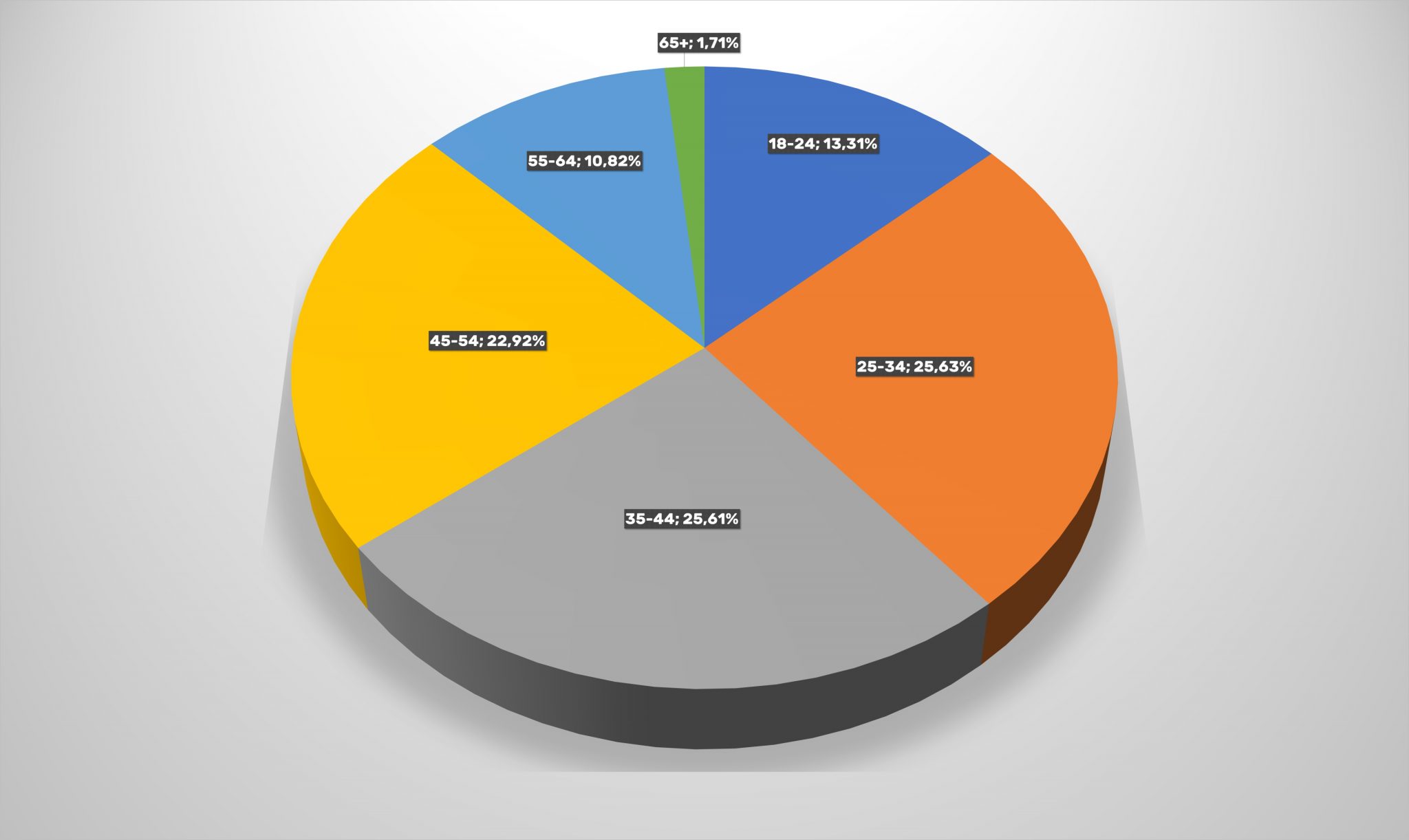

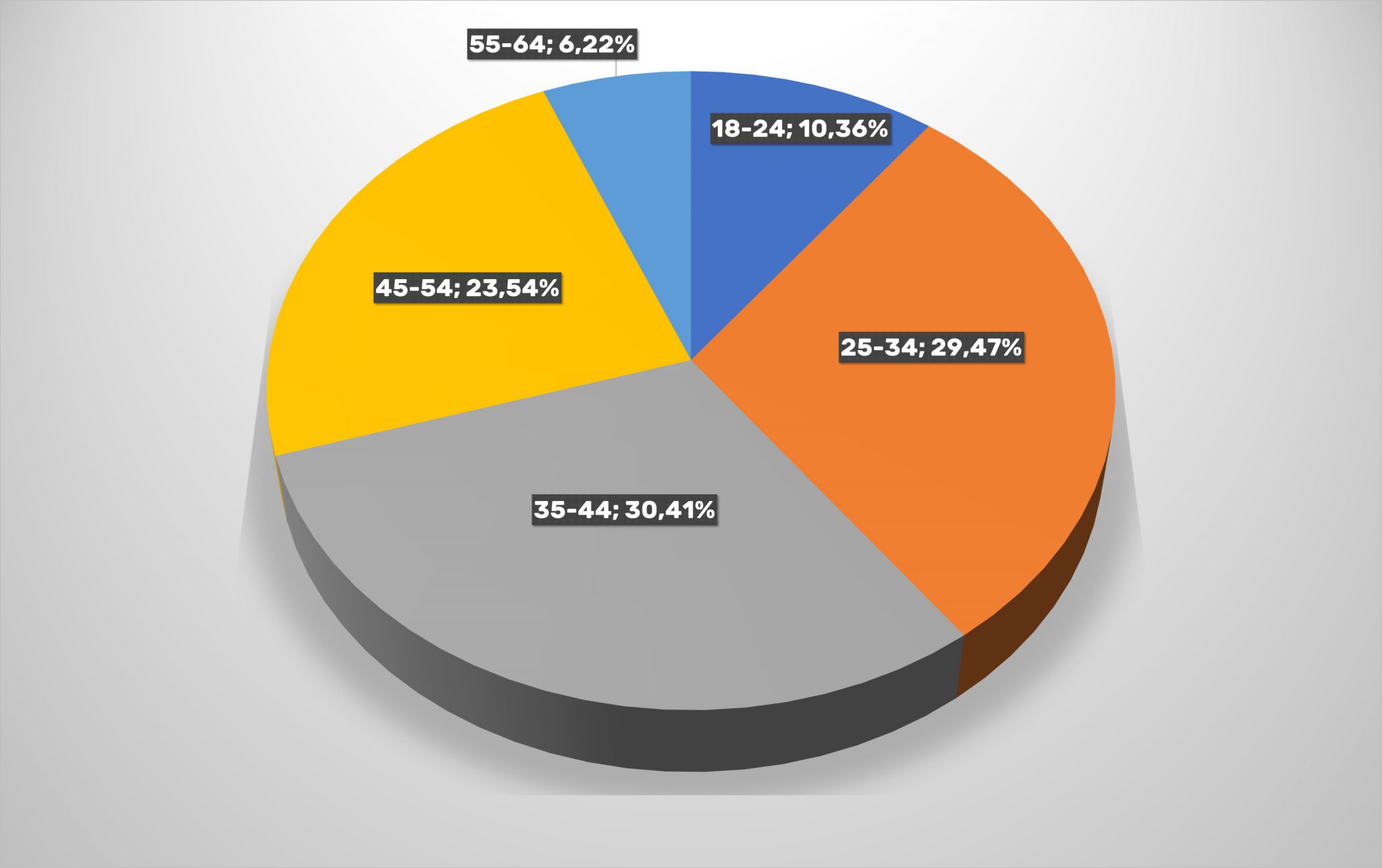

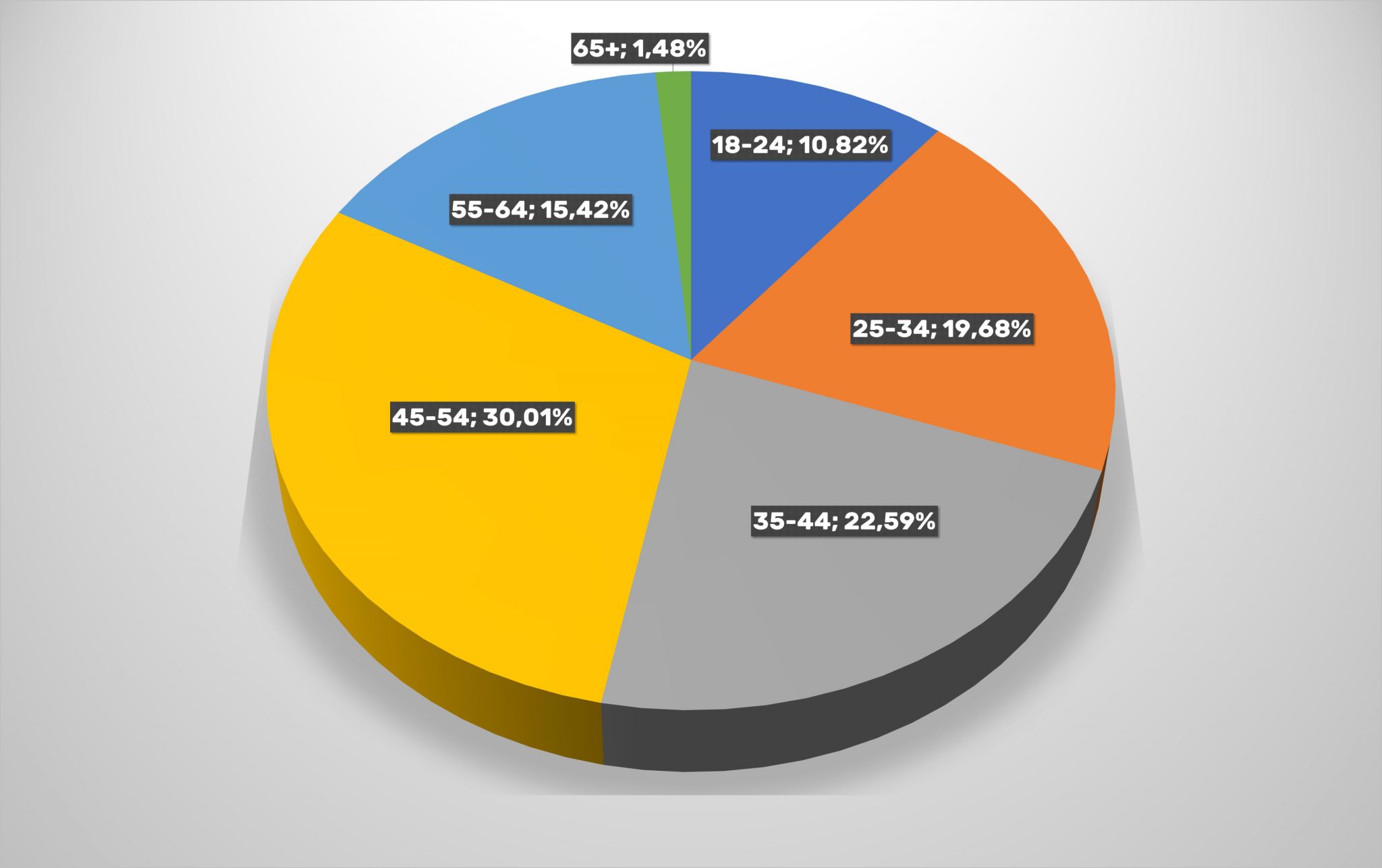

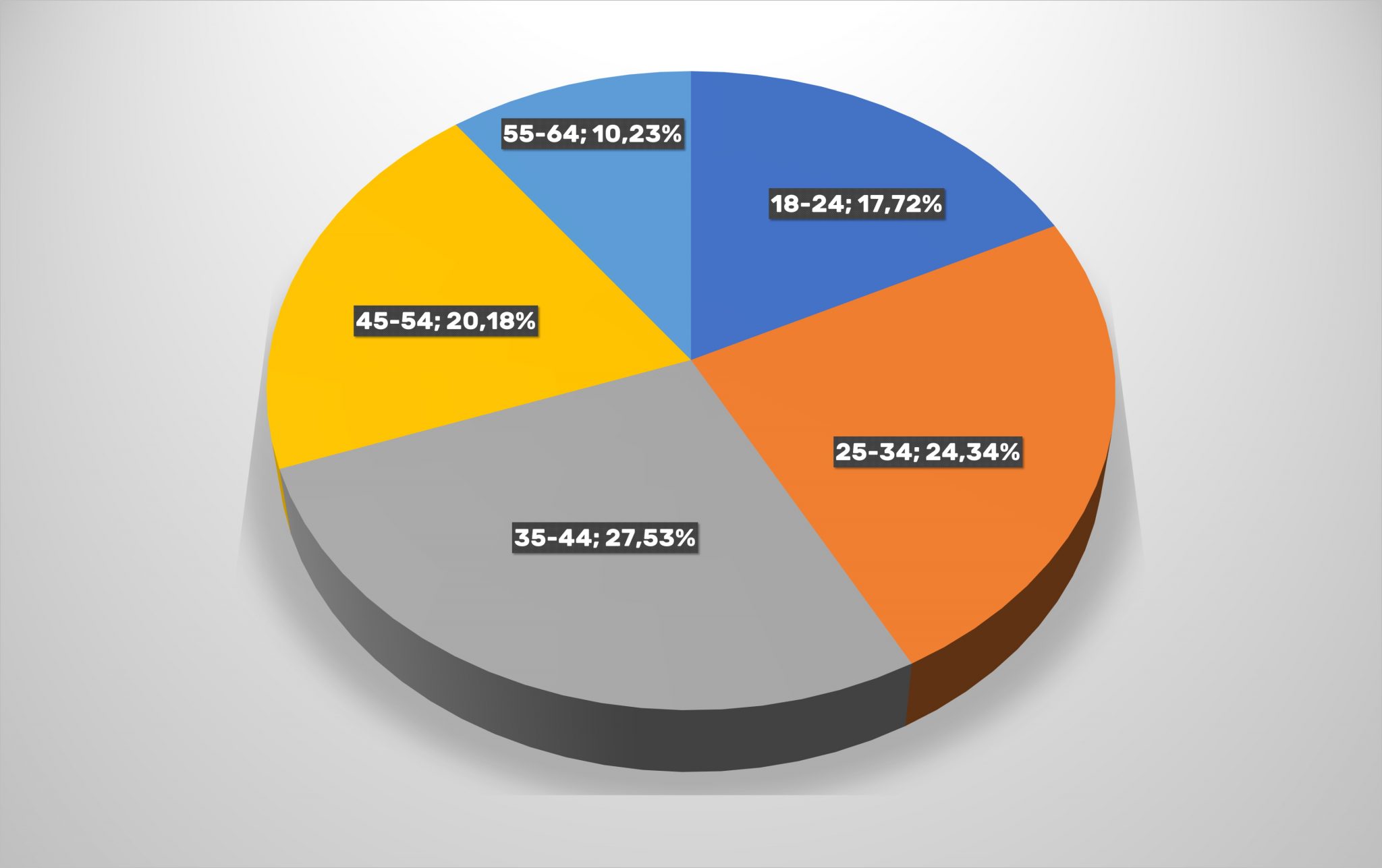

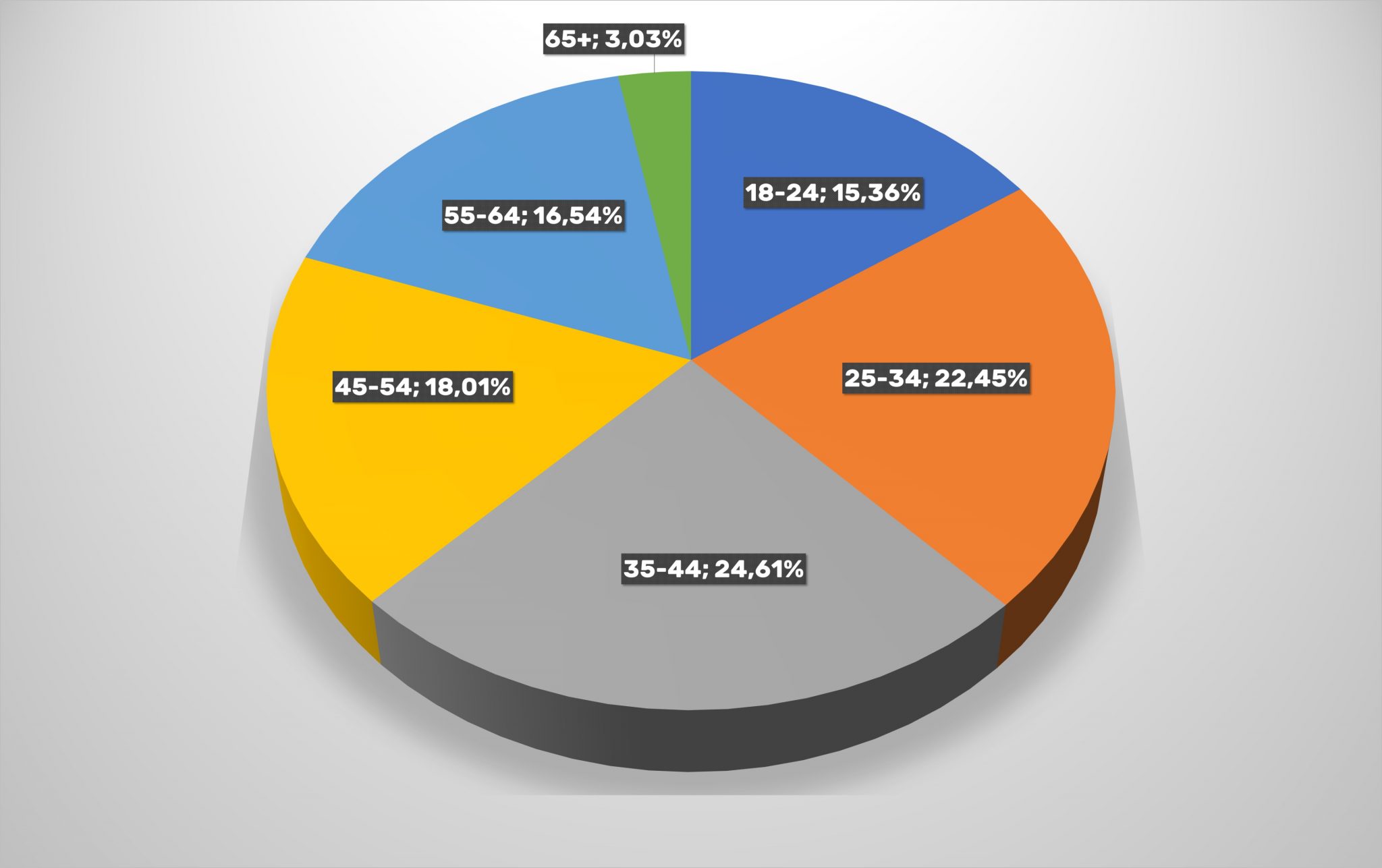

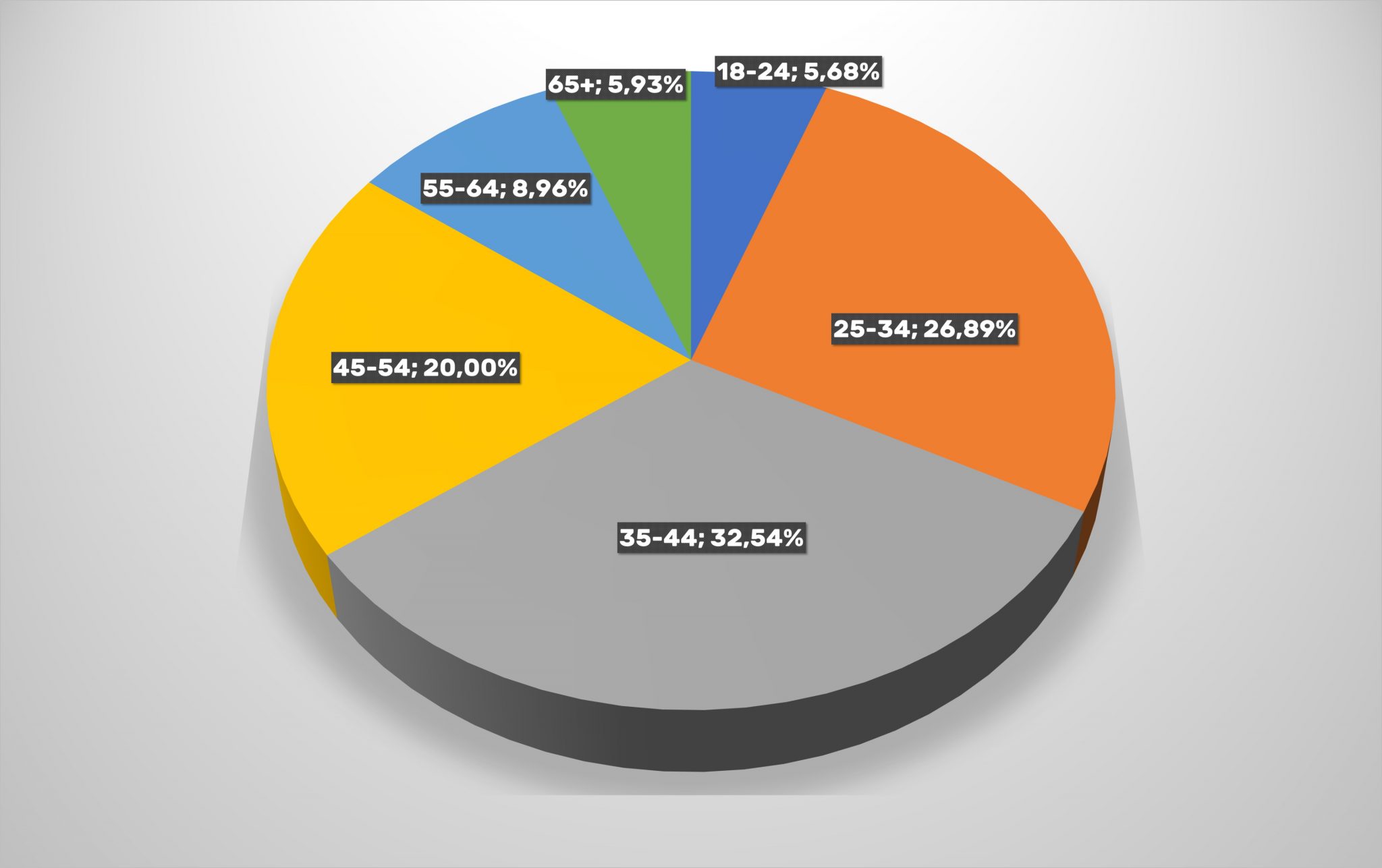

The users’ general age slice has remained approximately the same, more than 50% of online-store customers are people from 25 to 44 years old, another 36% are in age categories 18-24 and 45-54. The older generation (over 55) provides Ukrainian online-retailers with a little more than 12% (for comparison, in 2019 this users’ category accounted for exactly 10% from the online-stores’ traffic). It is worth noting that older people began to use the Internet more often, including due to quarantine restrictions. This affected the growth of the users’ audience over 45 years old and the reduction in the share of young and middle age’ users’ categories.

Department Stores

If we will consider individual segments of the domestic e-commerce in more detail, practically “under the microscope”, then it can be found many curious, and partly unexpected trends.

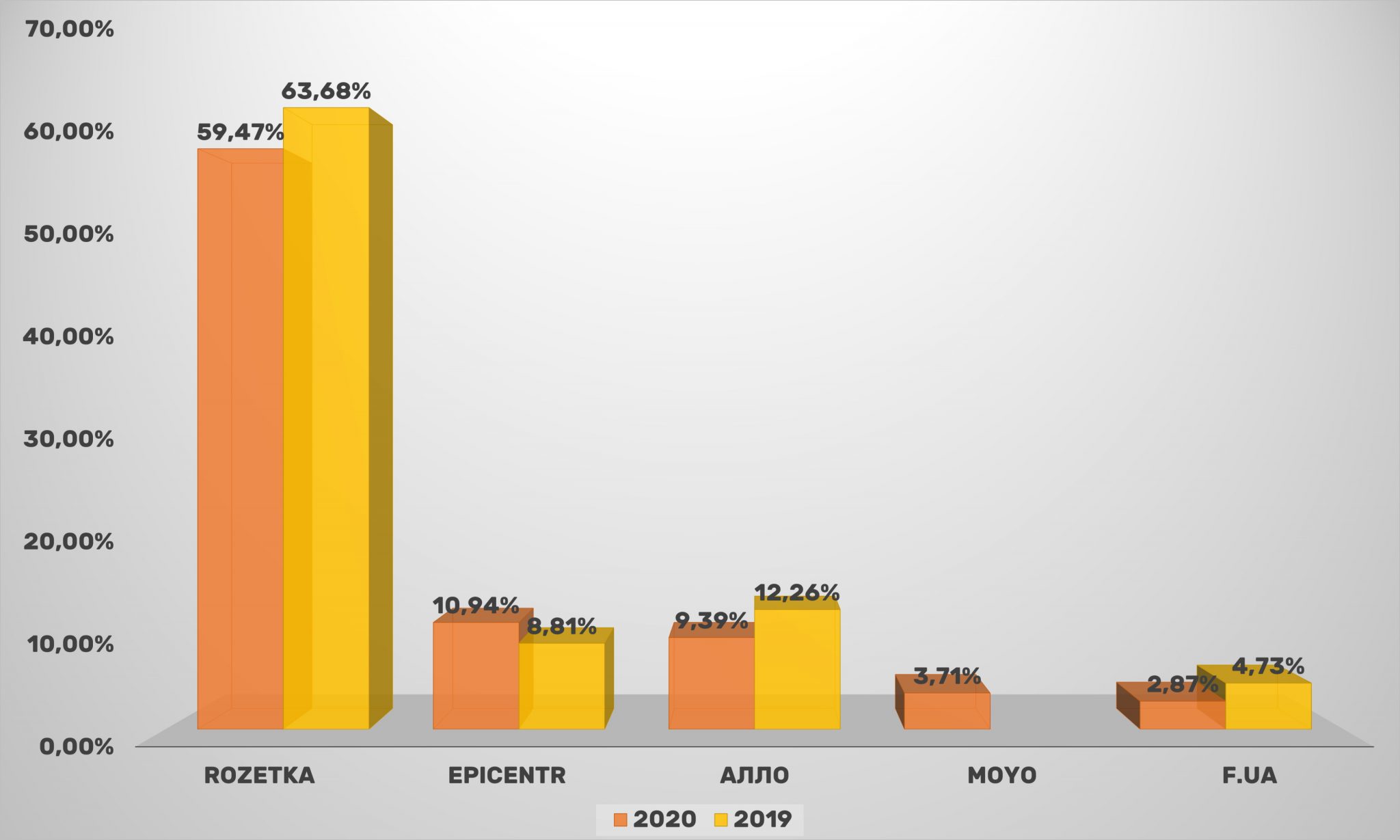

Rozetka.ua is a confident leader among department stores, far ahead of all competitors.

It is worth clarifying that the audience coverage in the diagram below (as in the following cases) is indicated as a percentage of the total segment traffic, and not only among named key players.

So, the largest Ukrainian marketplace Rozetka, despite a decrease in coverage, still controls about 60% all visitors to department online-stores. Over the year, the marketplace’ coverage has decreased by more than four percentage points. The trend of visitors’ loss continued on the ALLO website, which was moved to third place by the gaining momentum Epicenter.

It is also worth paying attention to the leaving from the Leading Five Kasta.ua, which first entered the Top-5 of universal online-stores last time. MOYO returned to its place. Most likely, precisely because the demand for fashionable things’ purchase in 2020 has slightly decreased. Whatever it was, but in 2020 the “passing barrier” was lower, as the share of other marketplaces continues to slowly decline (with the exception of Epicenter).

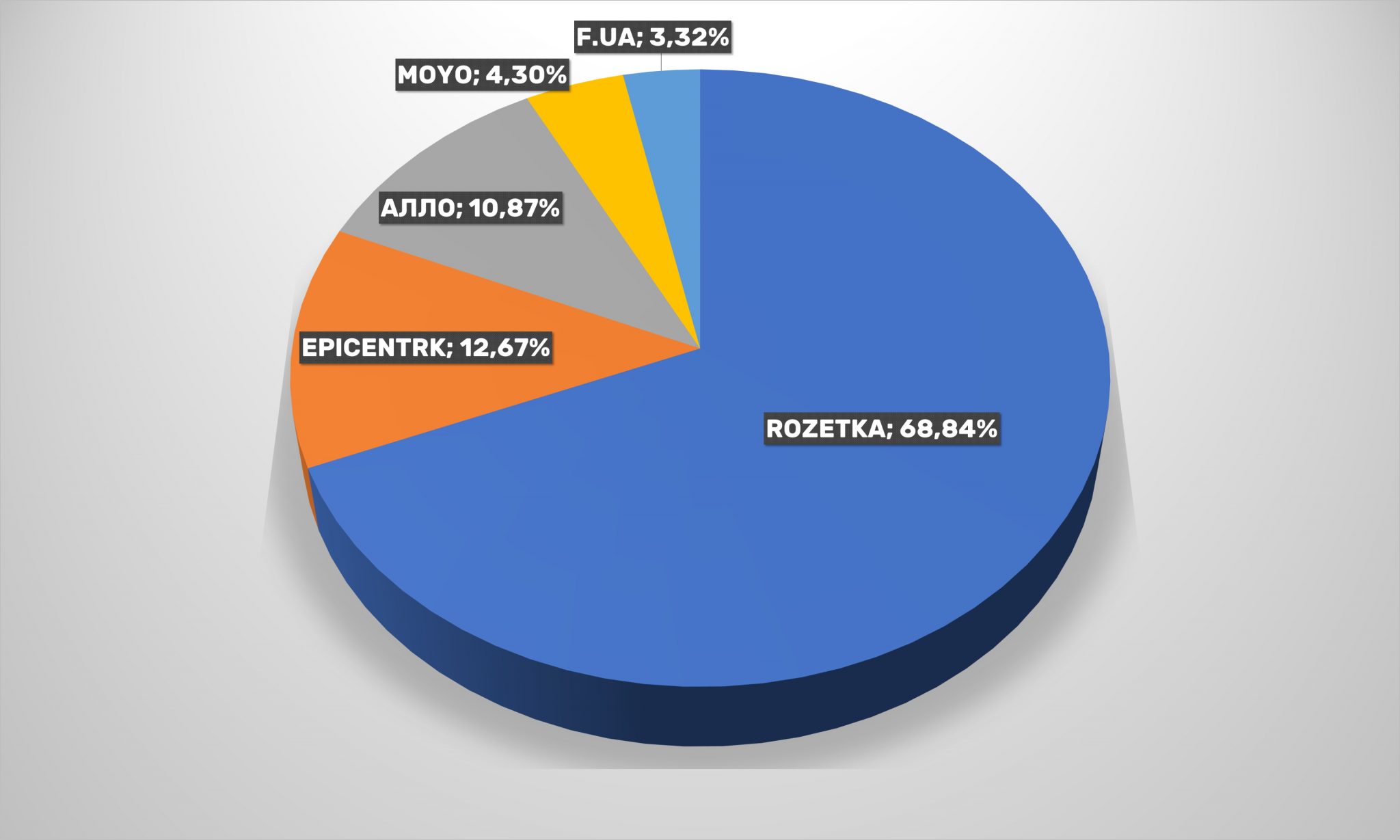

Positions of Vladislav Chechetkin’ brainchild is also unshakable in audience coverage’ terms among Top-5: over 68.84%. But Epicenter K is also confidently gnawing off market share from other players.

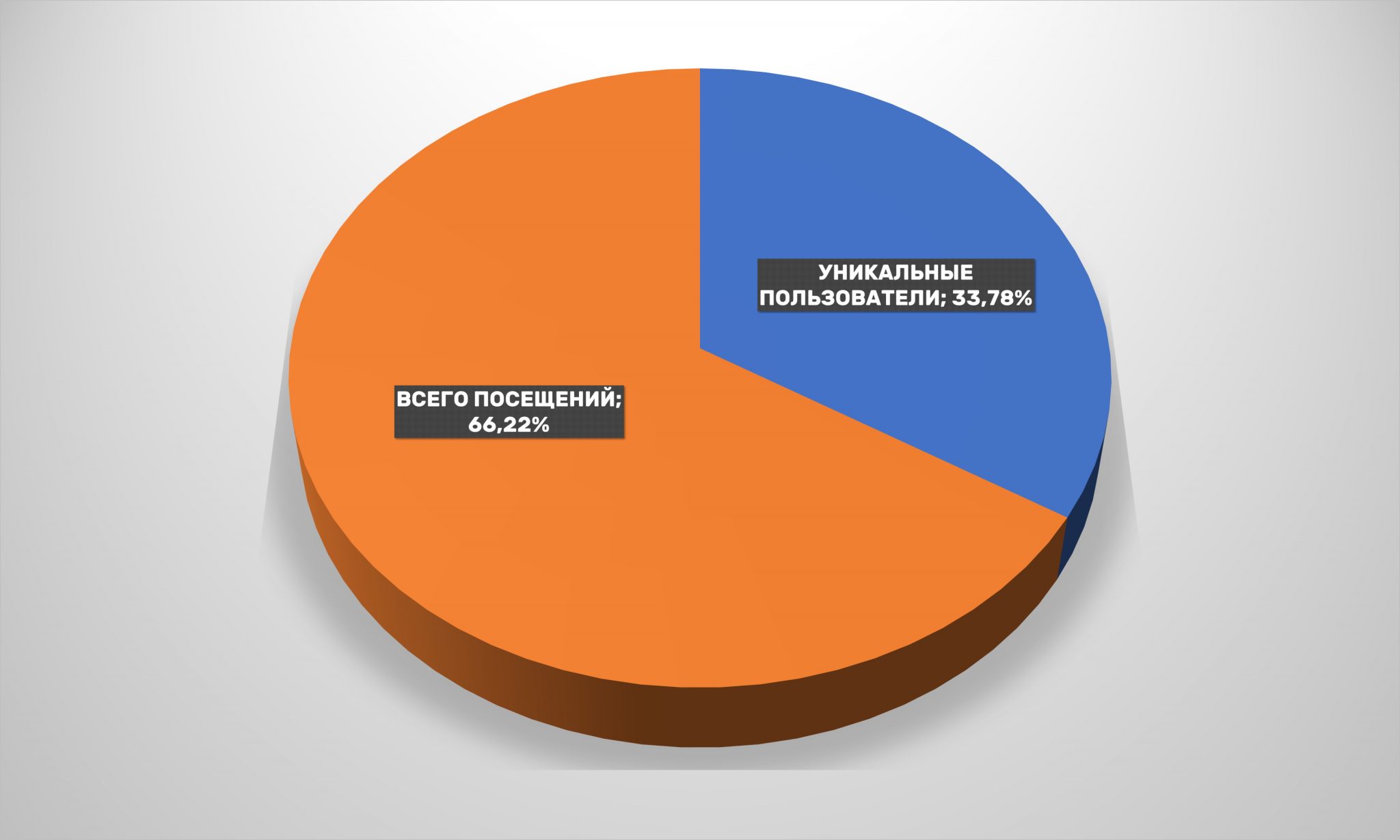

Audience loyalty also remains at a consistently high level: more than 66% users have visited leading marketplaces two or more times during the year. This indicator not only increased compared to 2019, but also exceeded results in 2018 (64.29%).

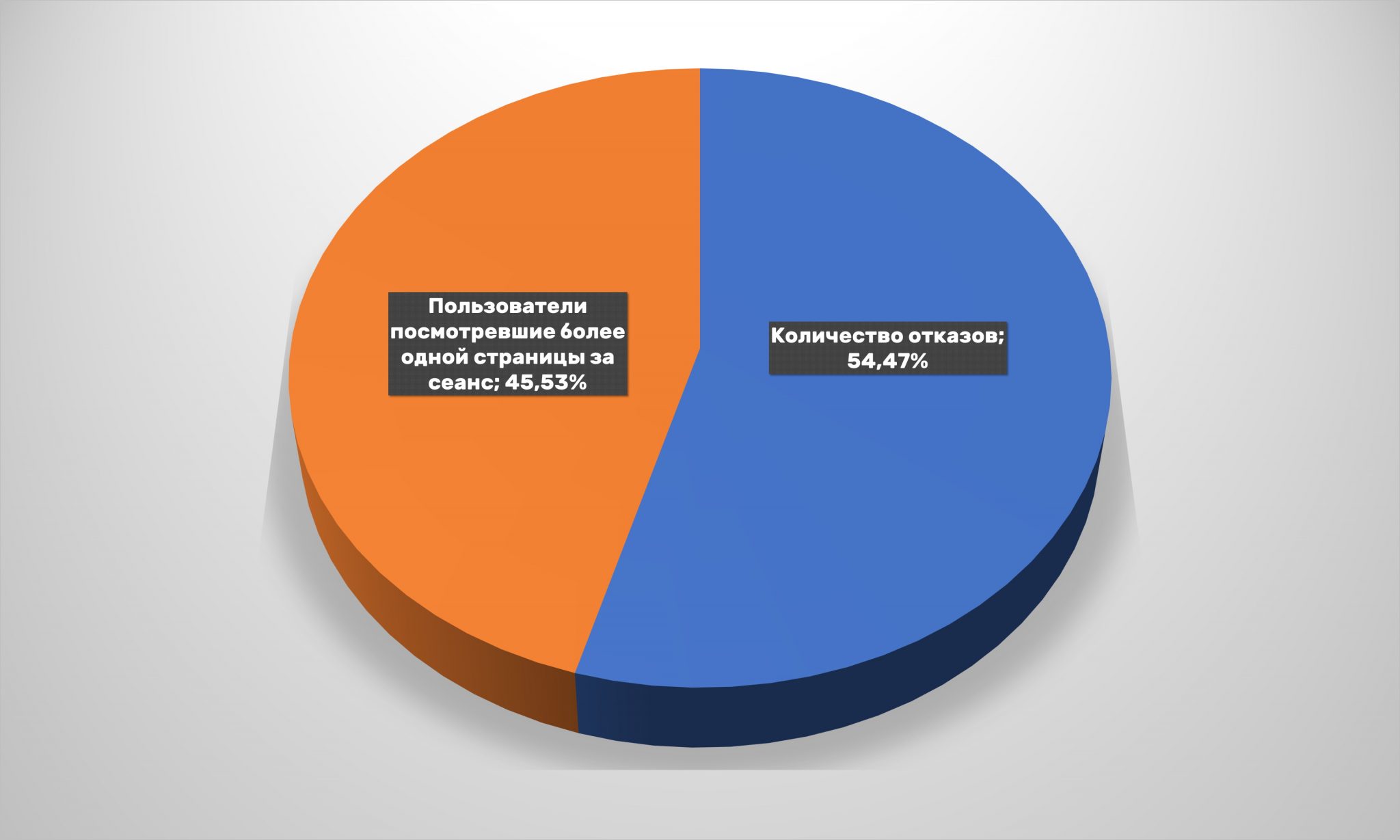

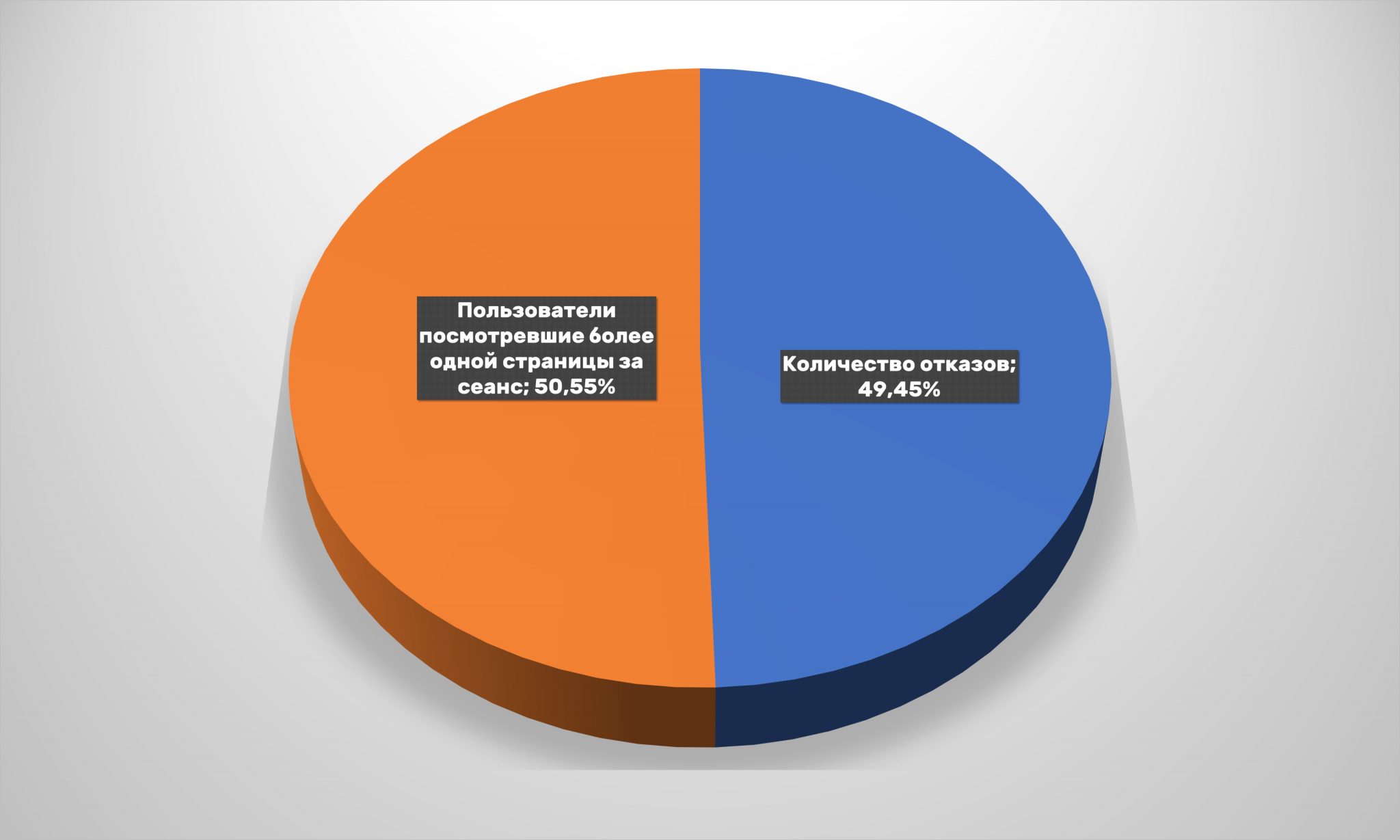

However, more than half of customers leave the site after viewing only one page, which means they are guaranteed without a purchase, since at least one transition must be made to pay for goods. And the number of refusals grows slightly from year to year.

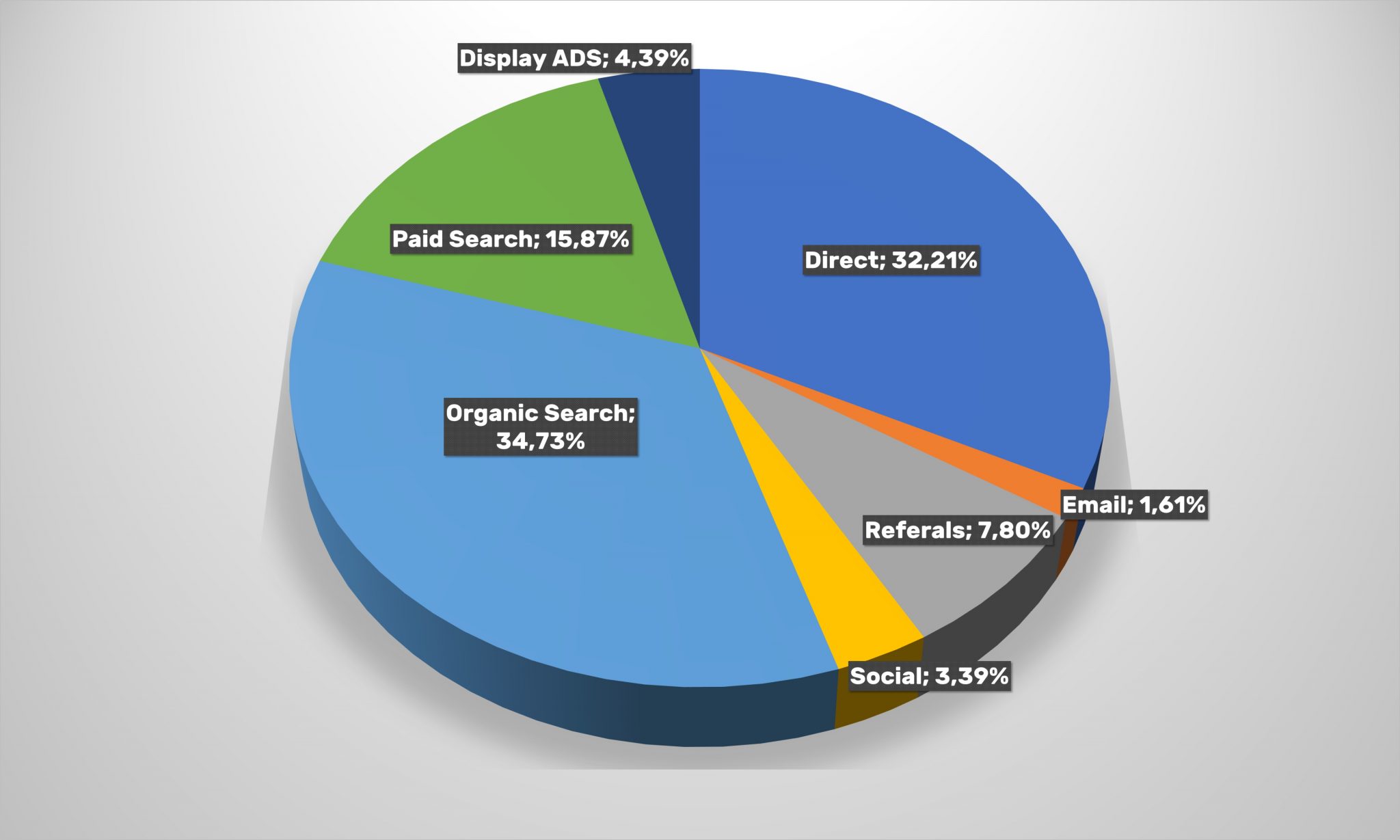

Another important factor is channels for attracting customers to department stores’ websites. The organic search’ role has grown significantly year over year – from 41% traffic to almost 50%. The number of clicks on promoted words here has decreased in contrast to the all-Ukrainian indicator of e-commerce: from 14.7 to 11.9%. The importance of cross-referencing and desktop applications continues to decline.

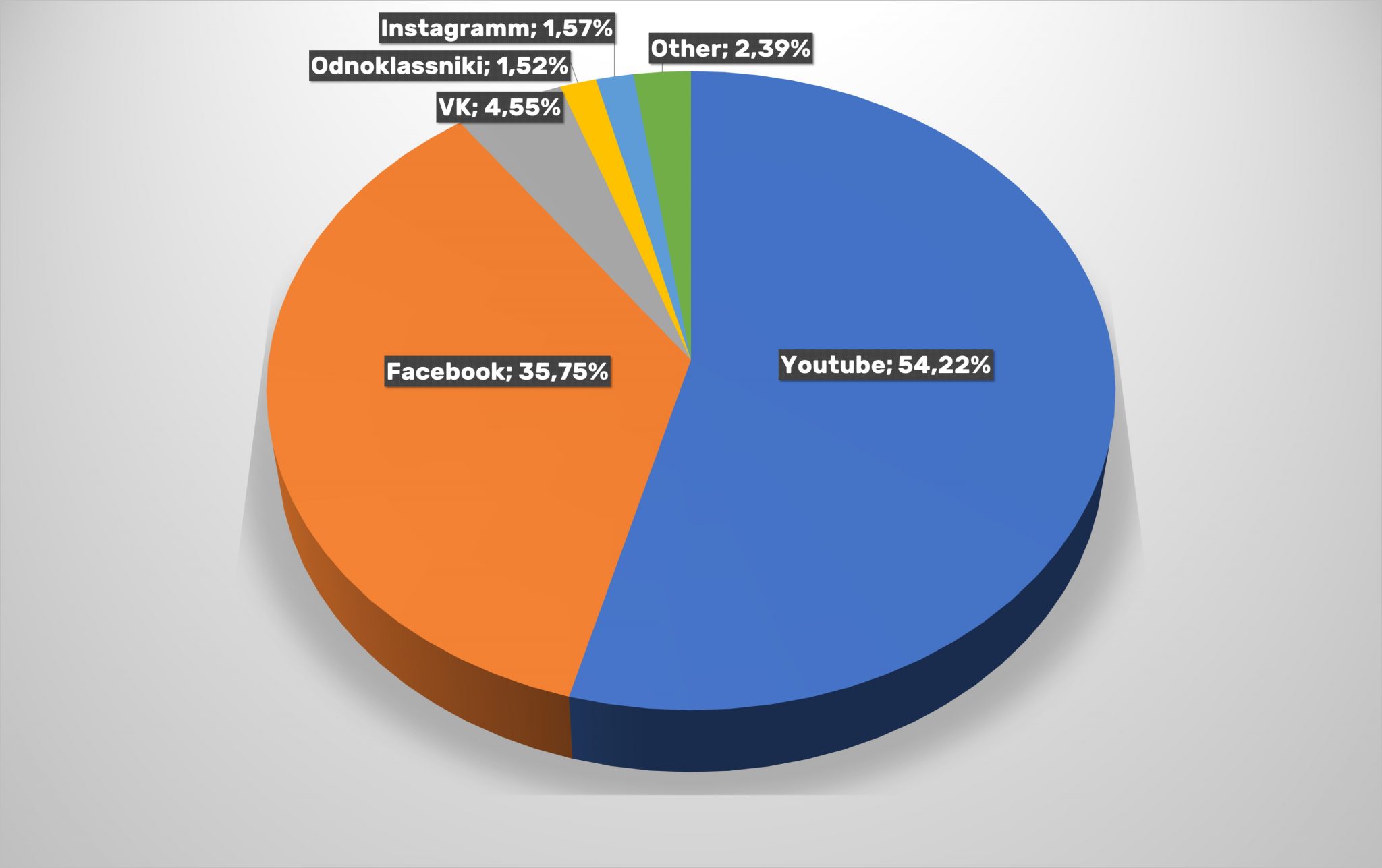

It should be noted that the social chains’ share as a visit channel has almost halved. Herewith, the Facebook’ share was again significantly lower than in YouTube service. And this is after the almost reached parity. Therefore, it is possible that in the future the situation of 2017 may repeat itself, when the video service provided 62% transitions to websites of universal online-stores from social chains.

Users visit marketplace sites approximately equally from mobile devices and from desktop computers or laptops. But for the first time, there are more mobile users.

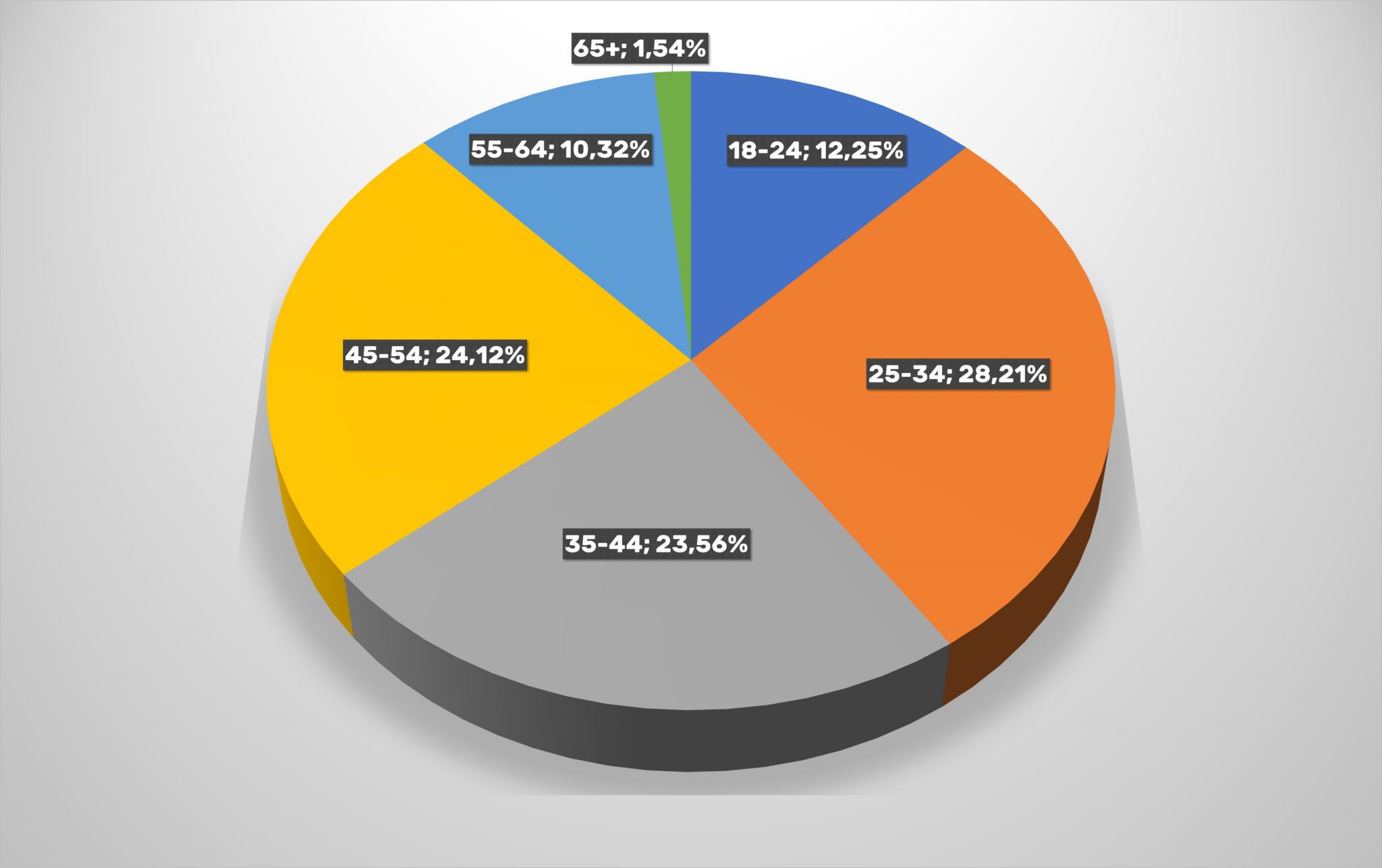

These changes may be explained by the fact that there are significantly fewer older users among online-shoppers of universal stores. Users who are over 55 years old make up a little more than 6%, and before it was almost every fourth. But at once the number of users aged 45-54 grew by 7%.

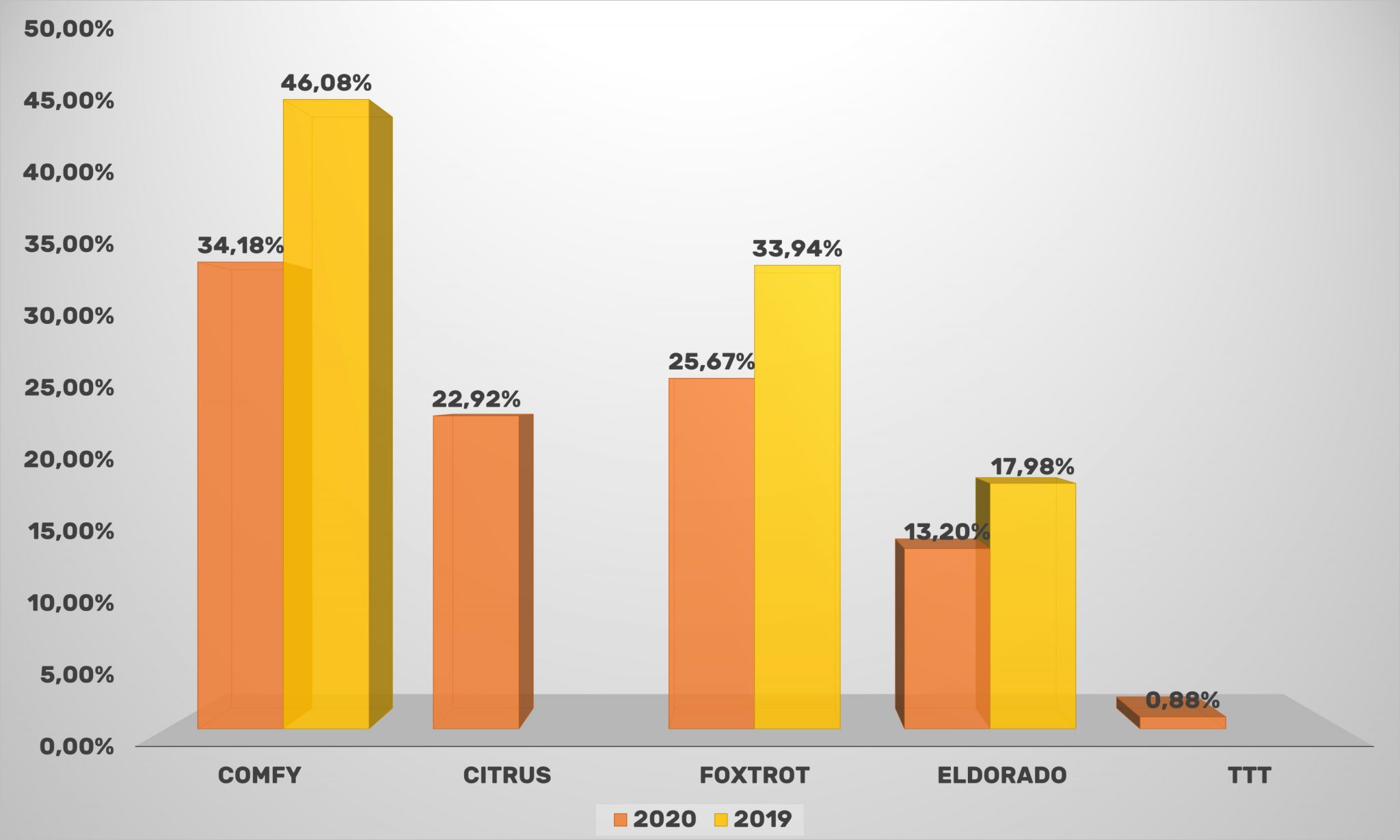

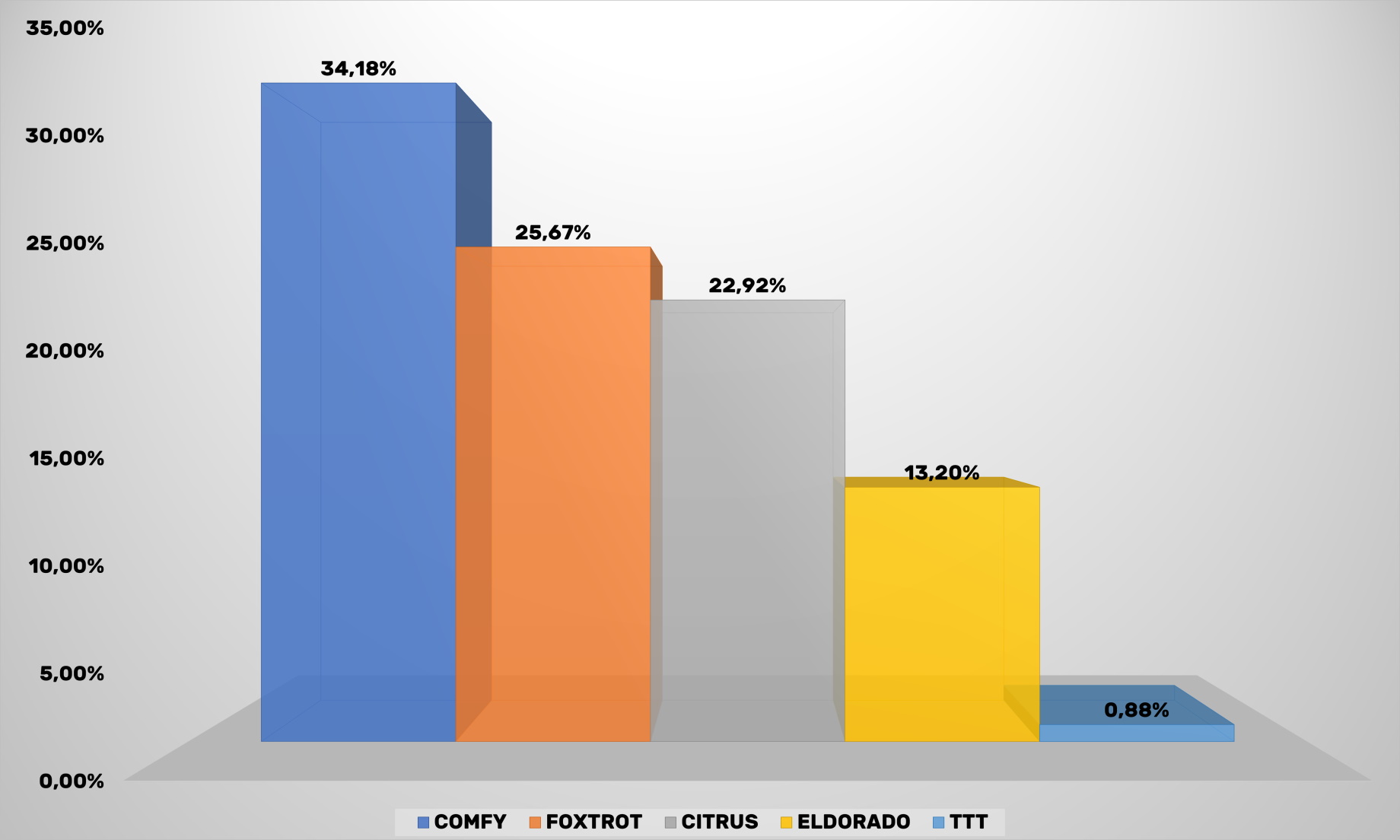

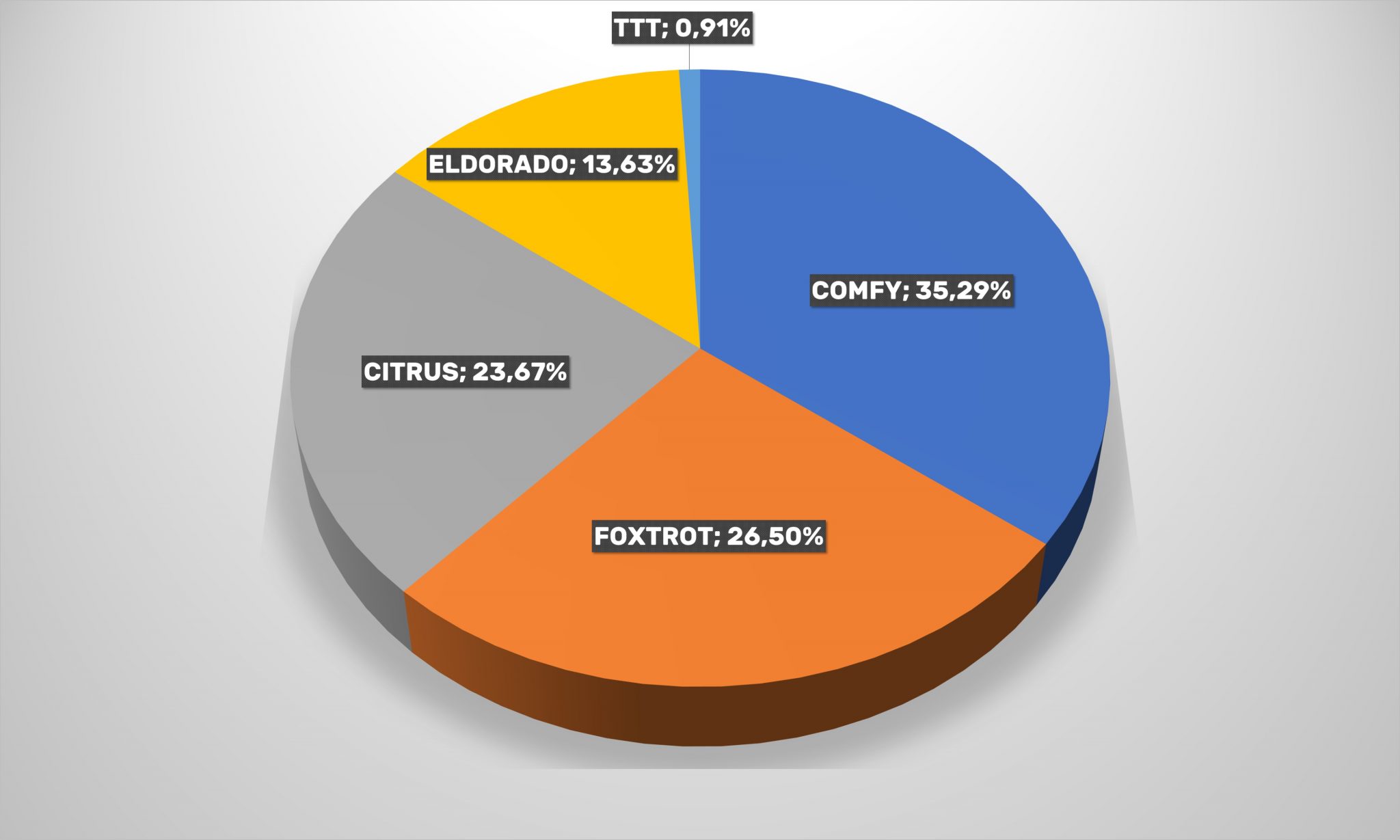

Home Appliances

Citrus and TTT are also noted apart from three main market players in this segment of Ukrainian e-commerce. After regaining lost positions in 2019, the “Big Three” slowed down again, which is largely due to consequences of quarantine restrictions and a general decline in effective demand.

Moreover, the market share of each player is almost the same as the general balance of power judging by the balance of power in the Top-5.

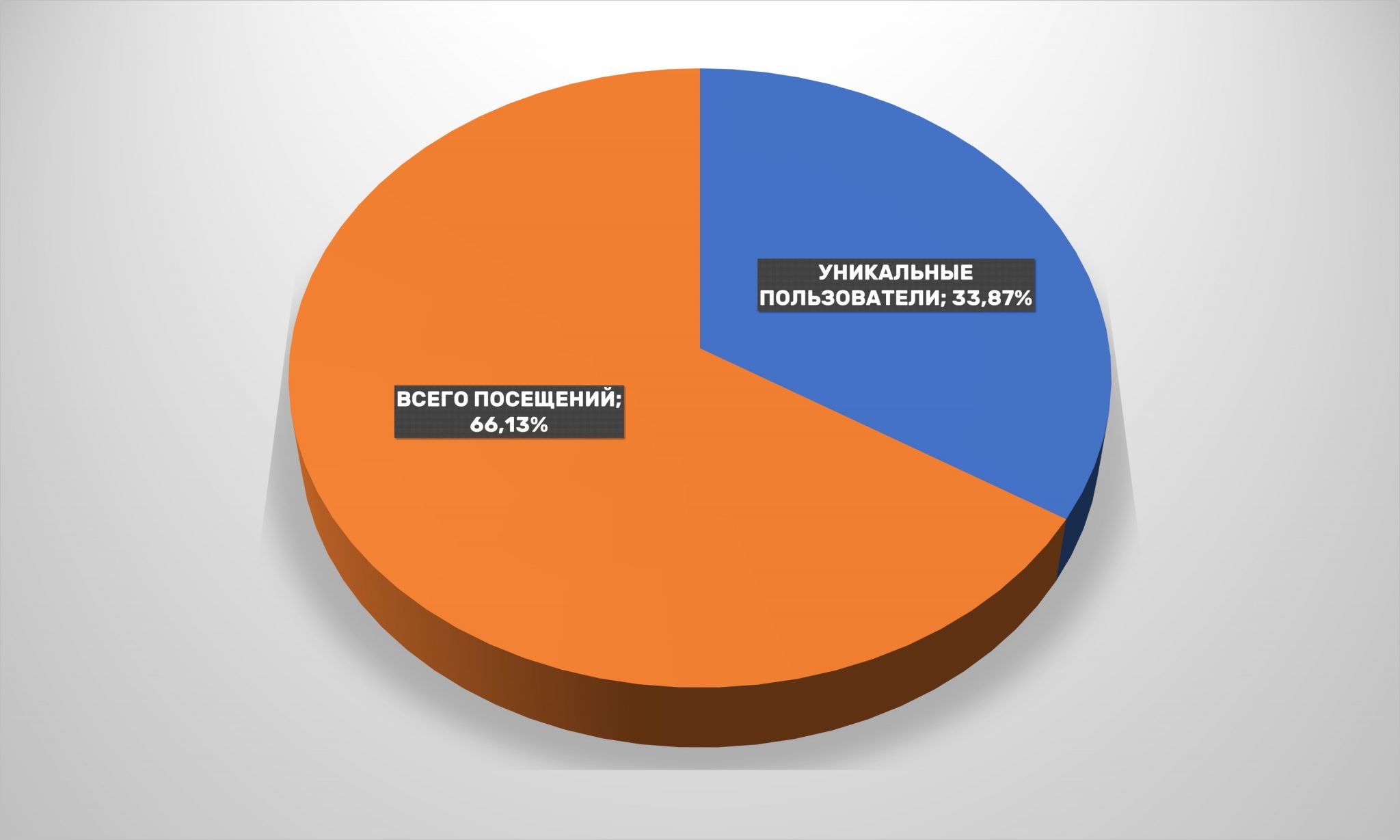

In 2019, users who visited the store’s website once a year and those who visited the portal two or more times shared approximately 50/50. Now there is a clear shift towards those who visit websites of technology’ retailers over and over again.

Herewith, the number of refusals continues to grow – it is already almost 50%. This means that only five out of ten website visitors do not leave, at least without going to another page.

In general, the situation with traffic channels in the category differs from average Ukrainian indicators. There is also a fairly significant share of paid advertising search, as well as an increase in the number of direct visits and a drop in organic traffic.

Social chains, as in the average Ukrainian indicator, provide sellers of household appliances and electronics with only 3.39% from total traffic. It would seem that this direction can be neglected, but all companies operating in this segment pay a lot of attention to SMM strategies. And again, YouTube took the first place, and Mark Zuckerberg’ brainchild came second. The rest can be neglected.

Over the year, companies in this category reduced mobile traffic by 4%, but managed to maintain the advantage of mobile traffic over desktop, achieved in 2019.

It is not surprising that most solvent categories of citizens prevail aged 25 to 55 there are among online-buyers of household appliances and electronics. The rest make up about a quarter of clients. However, it is worth noting that the customers’ share over 55 has doubled.

Fashion

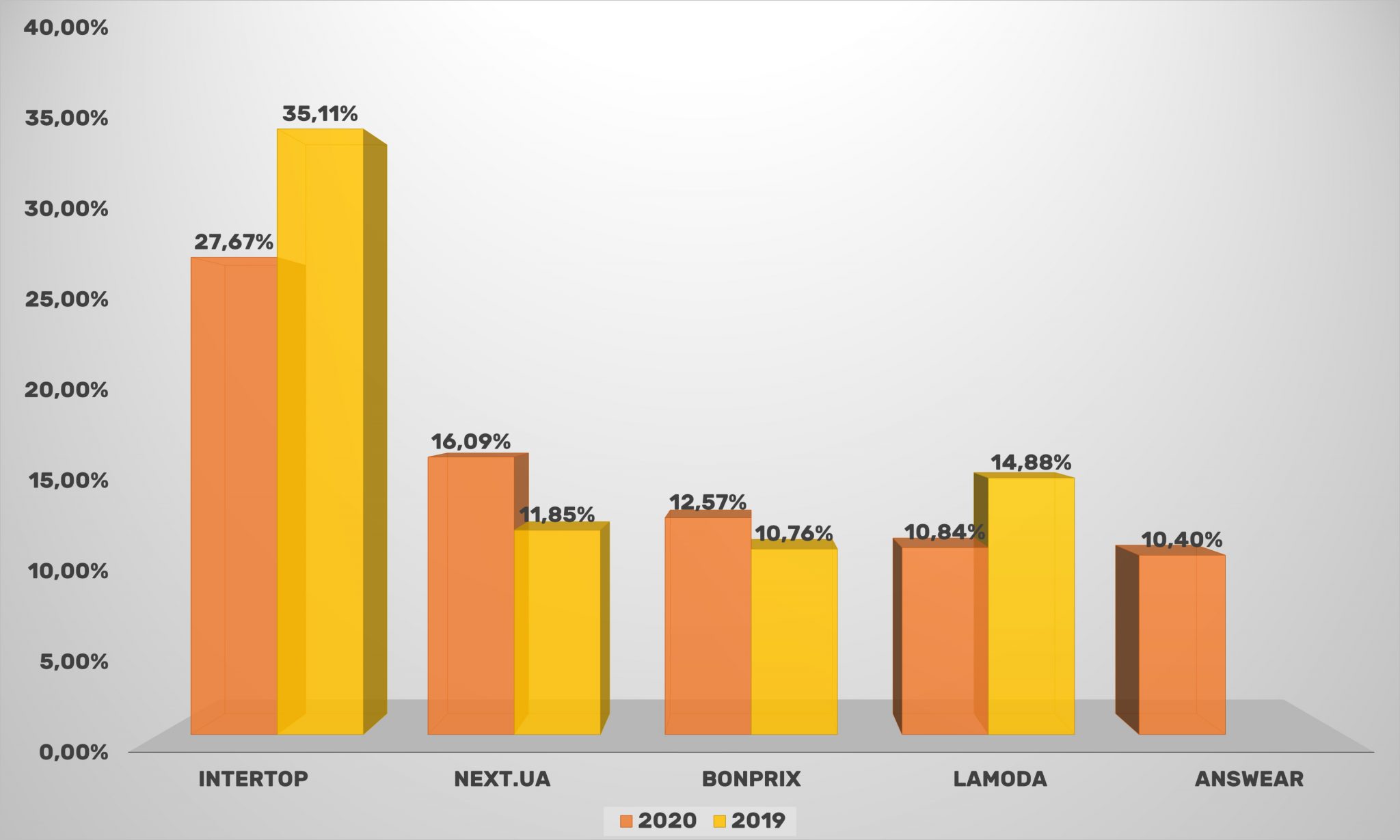

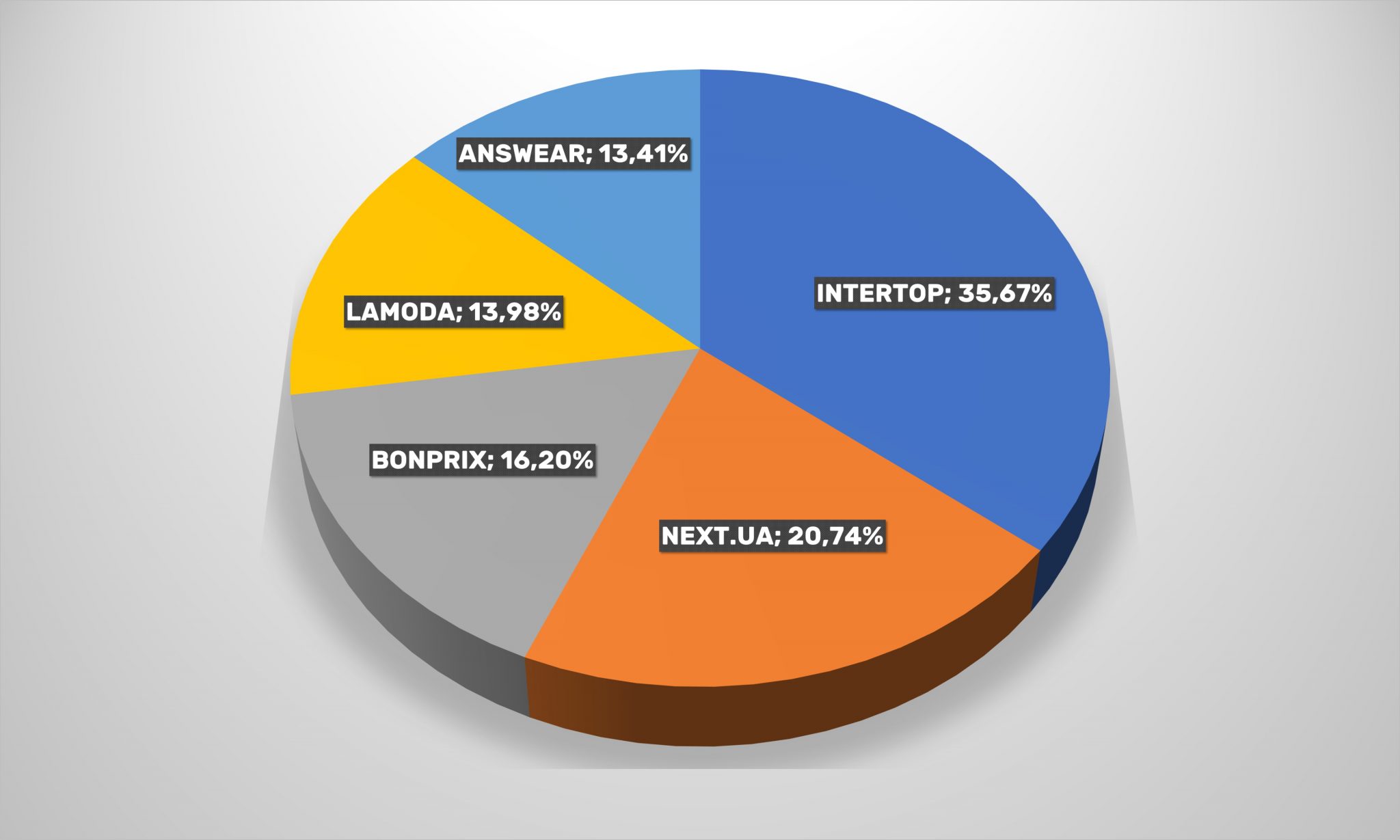

Since earlier Kasta.ua officially announced its work in the marketplace format and moved into the department stores’ category, a new player, Next.ua, appeared in Top-5 fashion operators of Ukraine on the Internet. In 2020, the participants’ list was replenished with the Answear online-store. LeBoutique dropped out of Top-5.

Only Intertop sells mainly its products among leaders in this direction. The rest have both own purchases and offers from third-party sellers. It would not be correct to exclude it from the rating of online-stores and refer only to marketplaces because a significant percentage of goods are its own stocks.

In general, only Next.ua and Bonprix have increased its coverage from former Top-5 fashion industry companies represented in the Internet Ukrainian segment.

Intertop, which took a leading position after Kasta.ua “transitioned” to another category was unable to continue the growth of the audience’ coverage last year. However, the continued focus of the MTI Group on developing the e-commerce business has allowed Intertop and its brands to maintain its lead over competitions.

In particular, Volodymyr Tsoi’s company reduced its coverages from 41 to 36 %% visitors to Ukrainian online-stores offering clothes, shoes and accessories. Its closest competitor in terms of coverage is Next.ua.

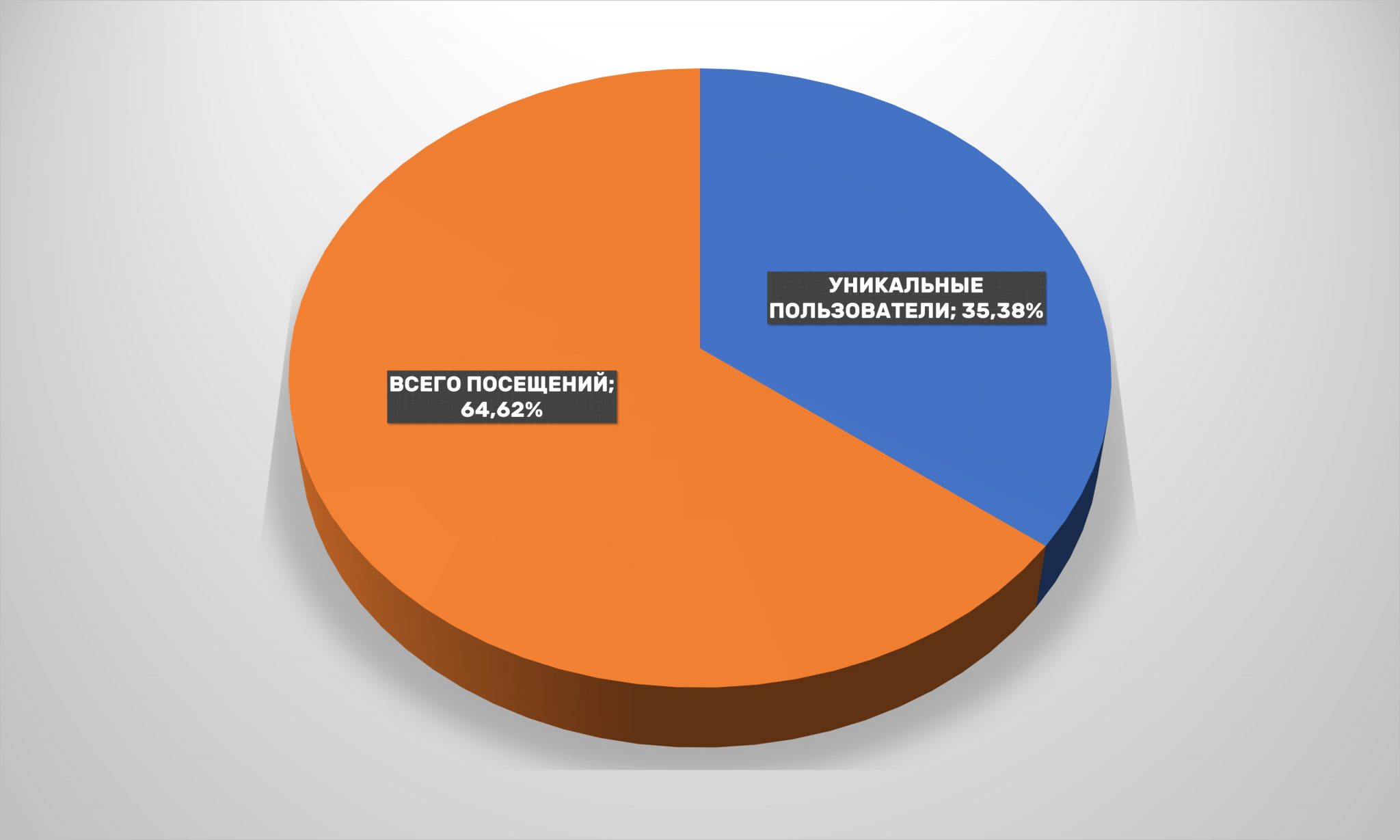

Herewith, the visitors’ loyalty to selected brands is growing. Almost 65% from them visit retailer websites more than once a year. Compared to last year, the indicator increased by 5%, albeit a little, but the tendency cannot but rejoice.

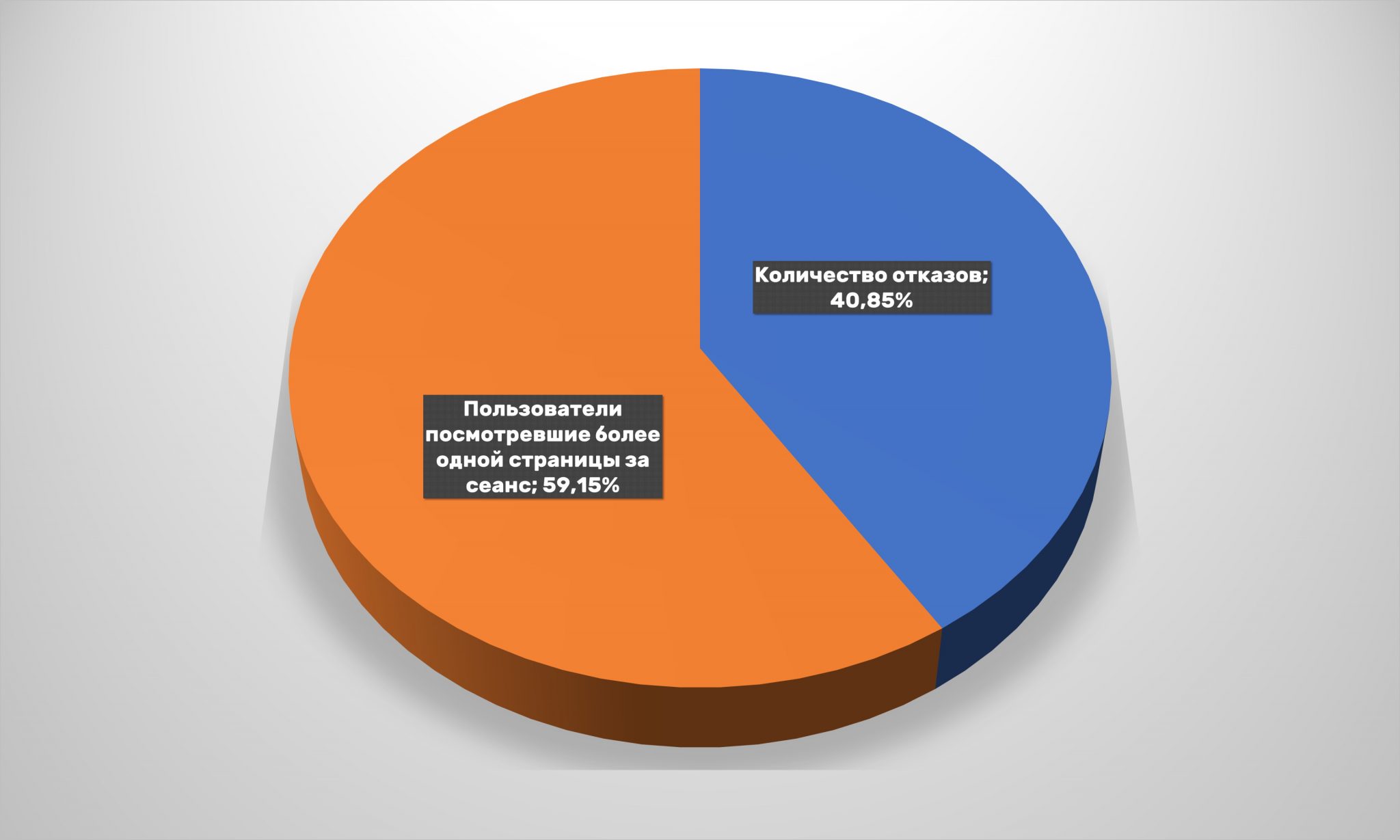

The number of refusals, although increased by 5%, is still within acceptable limits. High loyalty, good browsing’ depth, and a small proportion of users leaving the site immediately provide a good opportunity for high conversion among online-retailers of clothing and footwear.

True, fashion-operators working on the World Wide Web have to make a lot of efforts in order to achieve such indicators. The visits’ share from search engines is noticeably lower than in the market as a whole, but direct transitions, paid advertising, and applications, on the contrary, are higher. That is, marketers of fashion companies have to be creative in order to attract users.

At the same time, transitions by referral links have noticeably dropped and the effectiveness of e-mail newsletters has slightly decreased.

Here Facebook unlike trends in other segments has consolidated its status as the main traffic channel from social chains over the year, increasing its share by 7%, significantly ahead YouTube. In 2017, the situation was similar, but last year the abundance of video content played own role, and the service from Google was able to break out into first place. However, it was not for long.

Surprisingly, VKontakte and Odnoklassniki, formally banned in the country, still provide fashion-stores with more than 16% of transitions from social chains. While it is encouraging to see an increase in the share of other traffic sources.

The number of visits to online-clothing stores’ websites from mobile devices is increasing. And this trend has been continuing for several years. Now mobile traffic accounts for two thirds.

Also noteworthy is the high percentage of buyers from 45 to 64 years old – they are already more than half of all visitors to online-fashion stores. Young people under the age of 35 seem to prefer other buying channels – it is to retailers on a note.

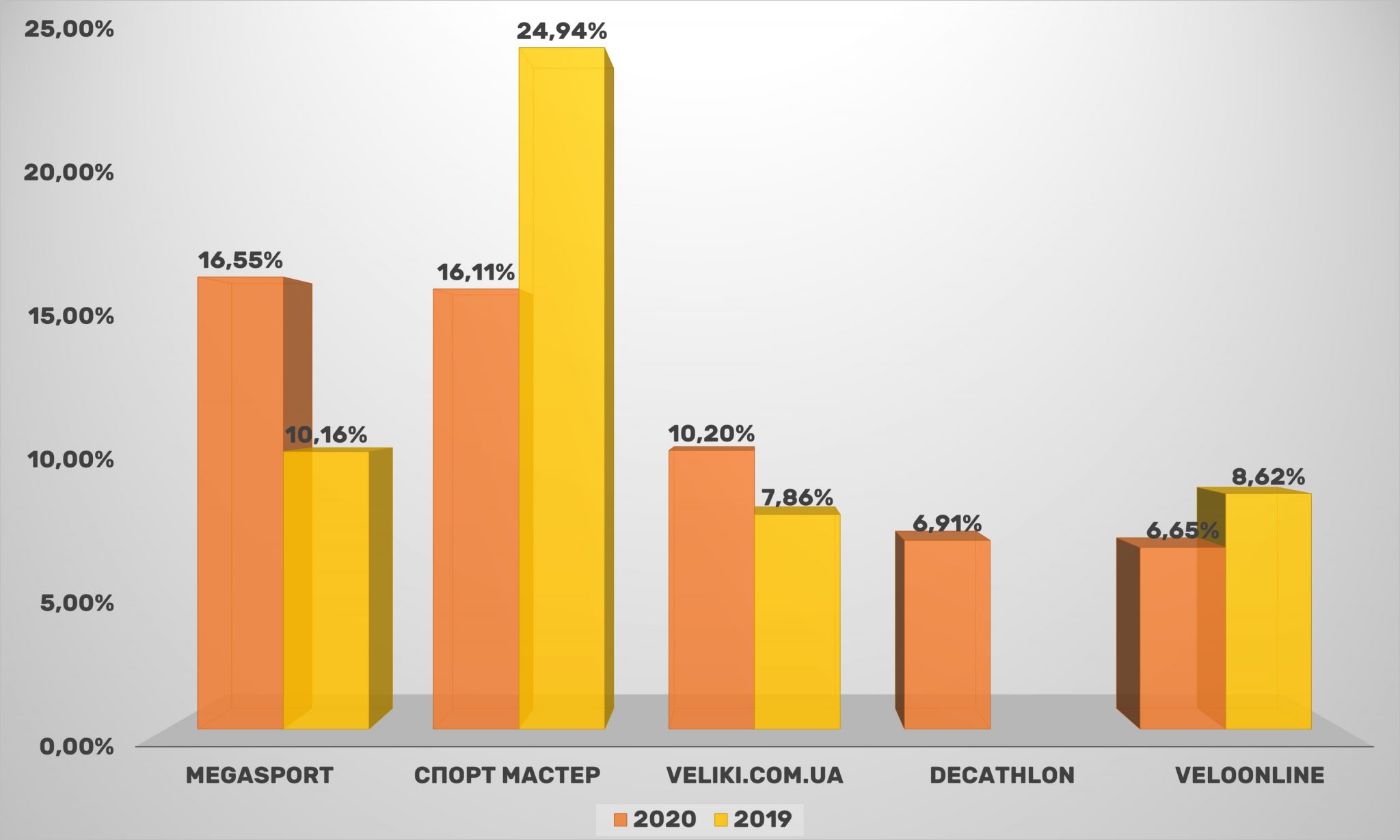

Sports goods

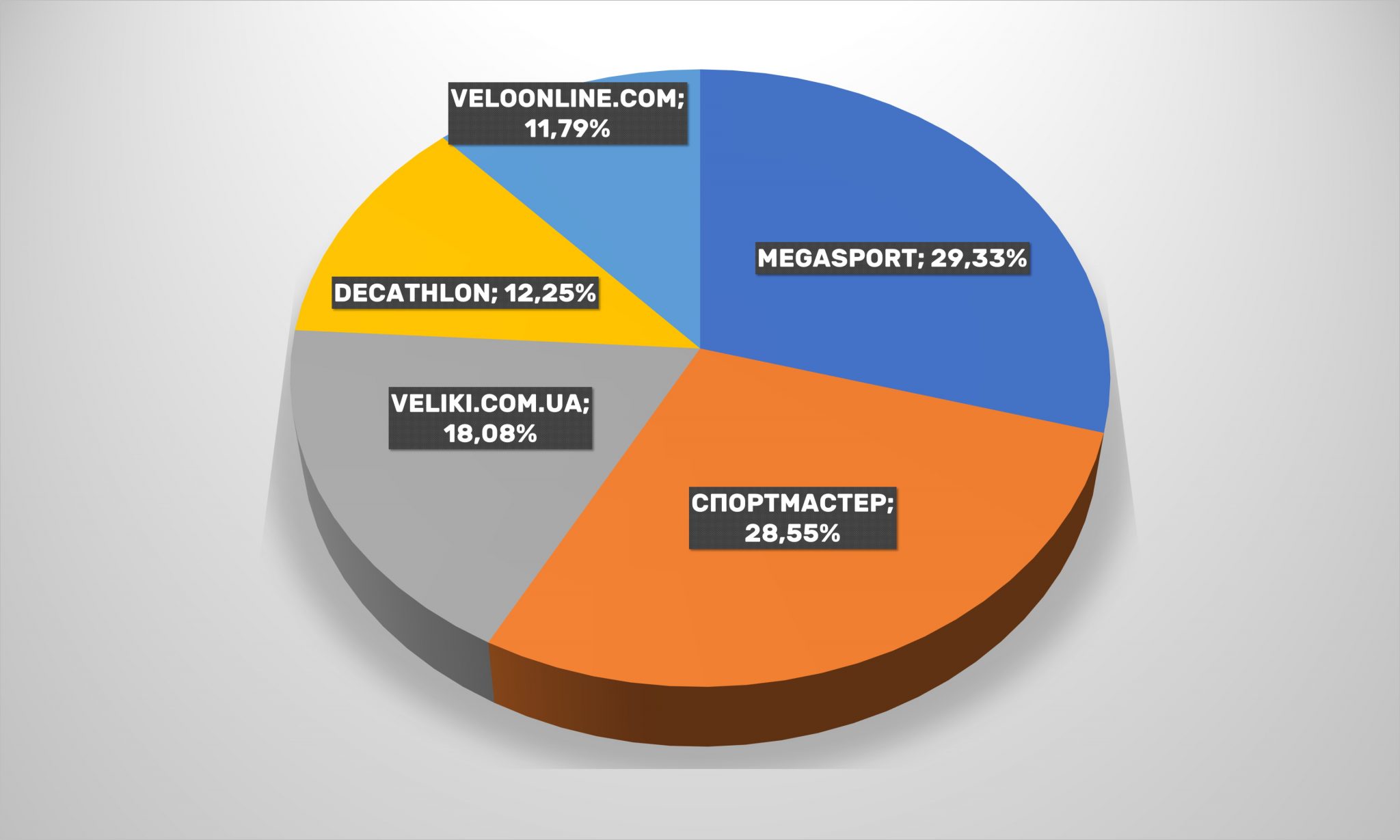

Only Sportmaster remained in this category from previous market leaders, and Drive Sport dropped out of Top-5 stores. The newcomer of the previous rating Megasport broke into leaders, slightly outstripping Sportmaster in coverage. Veliki.com.ua took the third place, which is confidently catching up with leaders.

We also note the appearance the new player Decathlon in the Top-five, who burst into the leading group. Thus, the intensive process of updating the category continues, which indicates active competition in the market.

Herewith, newcomers immediately “bite off” a solid share from market old-timers, if taking into account the division of audience’ coverage among five leaders. Obviously, the last luminary Sportmaster will have to make a lot of efforts to maintain its position and not yield to debutants.

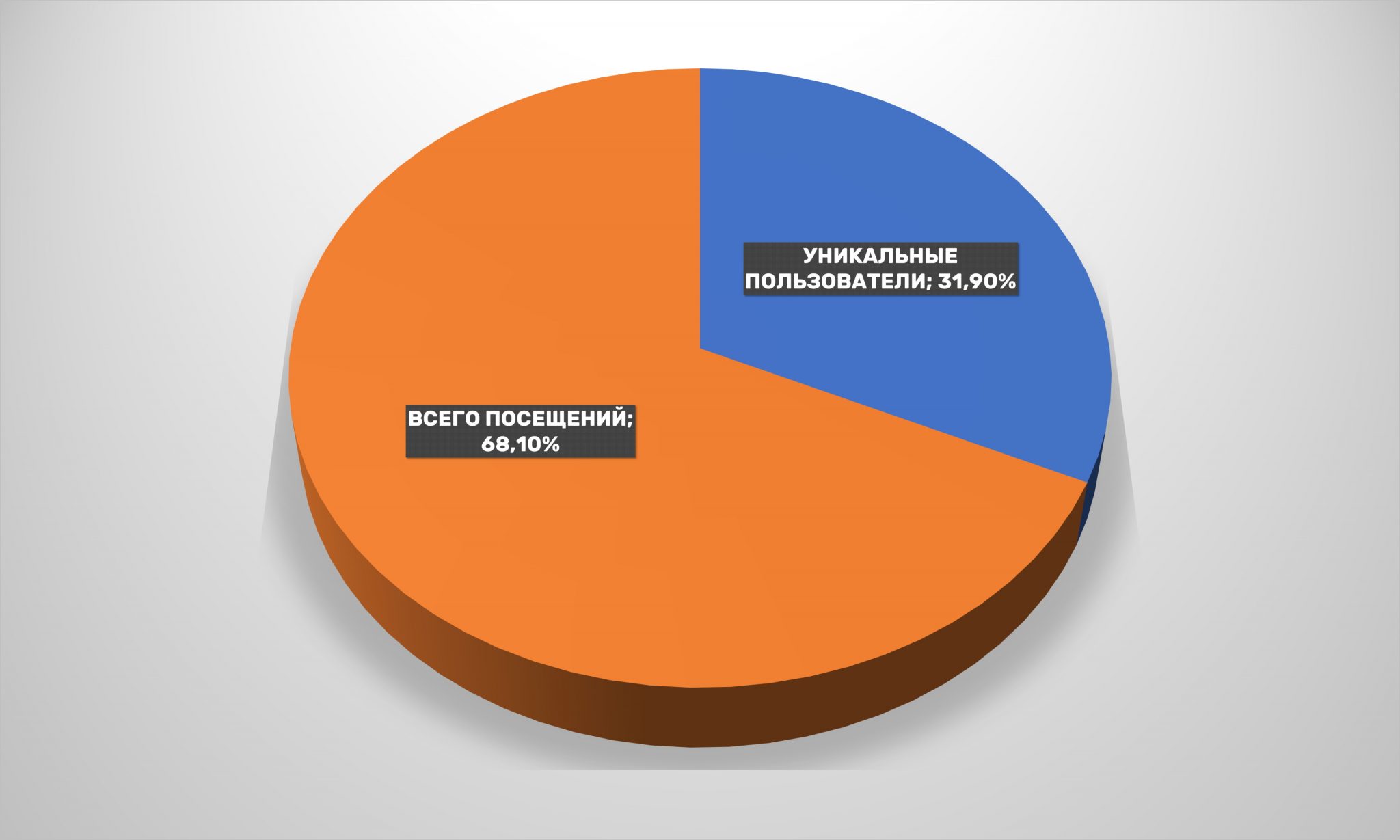

The situation with unique / repeated visits is no different from the average in Ukraine: two-thirds of a loyal audience, but there are also enough newcomers.

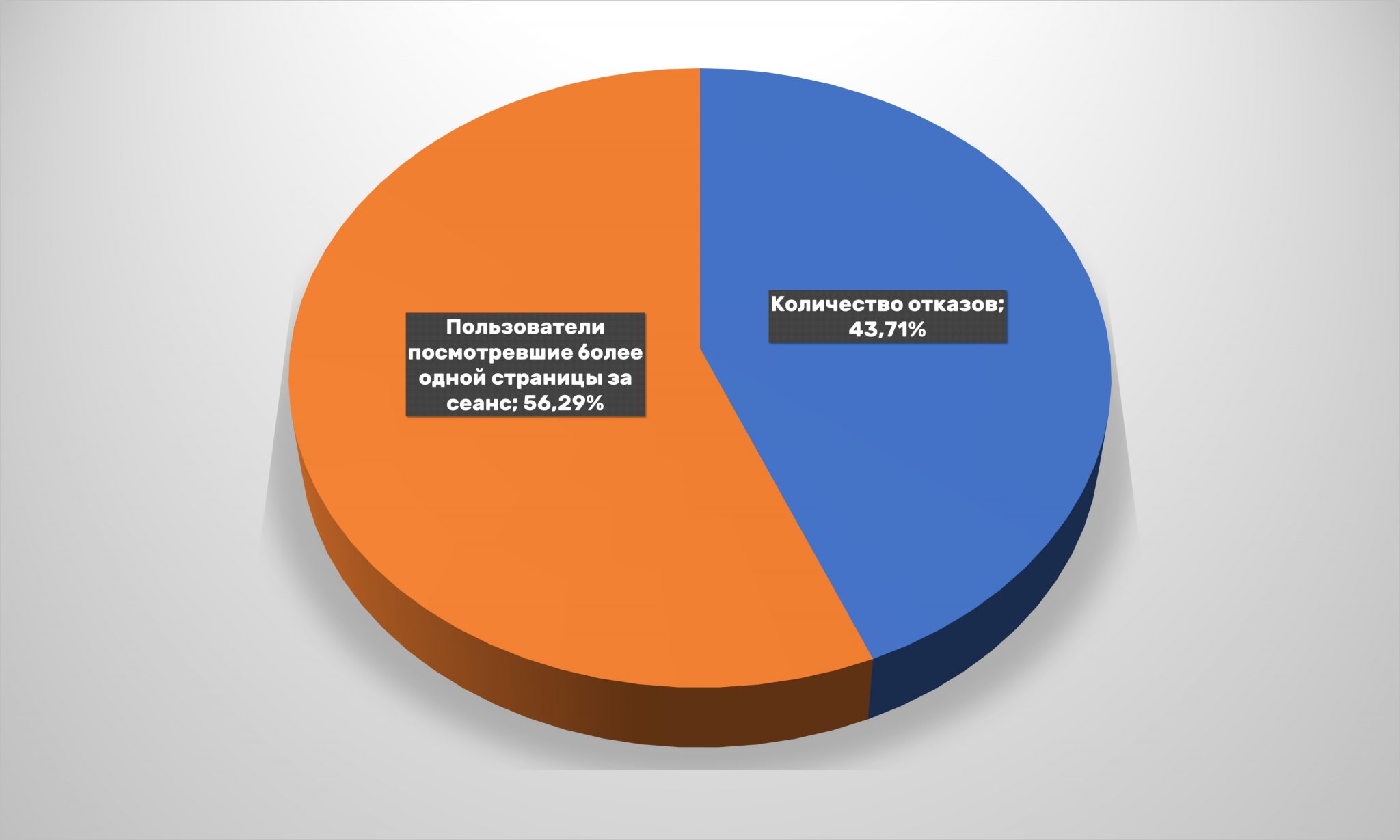

The number of failures has decreased. As a result, significantly more than half of users continue their journey through the online-store, which means they are likely to make a purchase.

What is regarding visit’ channels – more visits from search engines on organic free search have increased, while the share of direct visits is also growing. There are a lot of clicks from paid advertising, but clicks to other sources have noticeably dropped.

In particular, the share of clicks from social chains fell by half: from 8 to 4%. YouTube remains the main generator of traffic from social chains among sporting goods – now it is almost half of all visits to sites as in most other categories of Ukrainian online commerce. At the same time, Facebook increased its share, but it still lags behind its “colleague” by almost 10%.

The majority of users still visit online-stores in this category from mobile devices. However, over the year, the share of “mobile” customers fell back from an impressive 75% to “regular” 55%.

This is likely due to the growing older audience. So, the number of users over 45 years old grew by 8% at once, to a third of all buyers. The number of young buyers under the age of 35 decreased by the same amount. It turns out that older people cared more about their physical fitness than young people. And this is also possibly the impact of the pandemic.

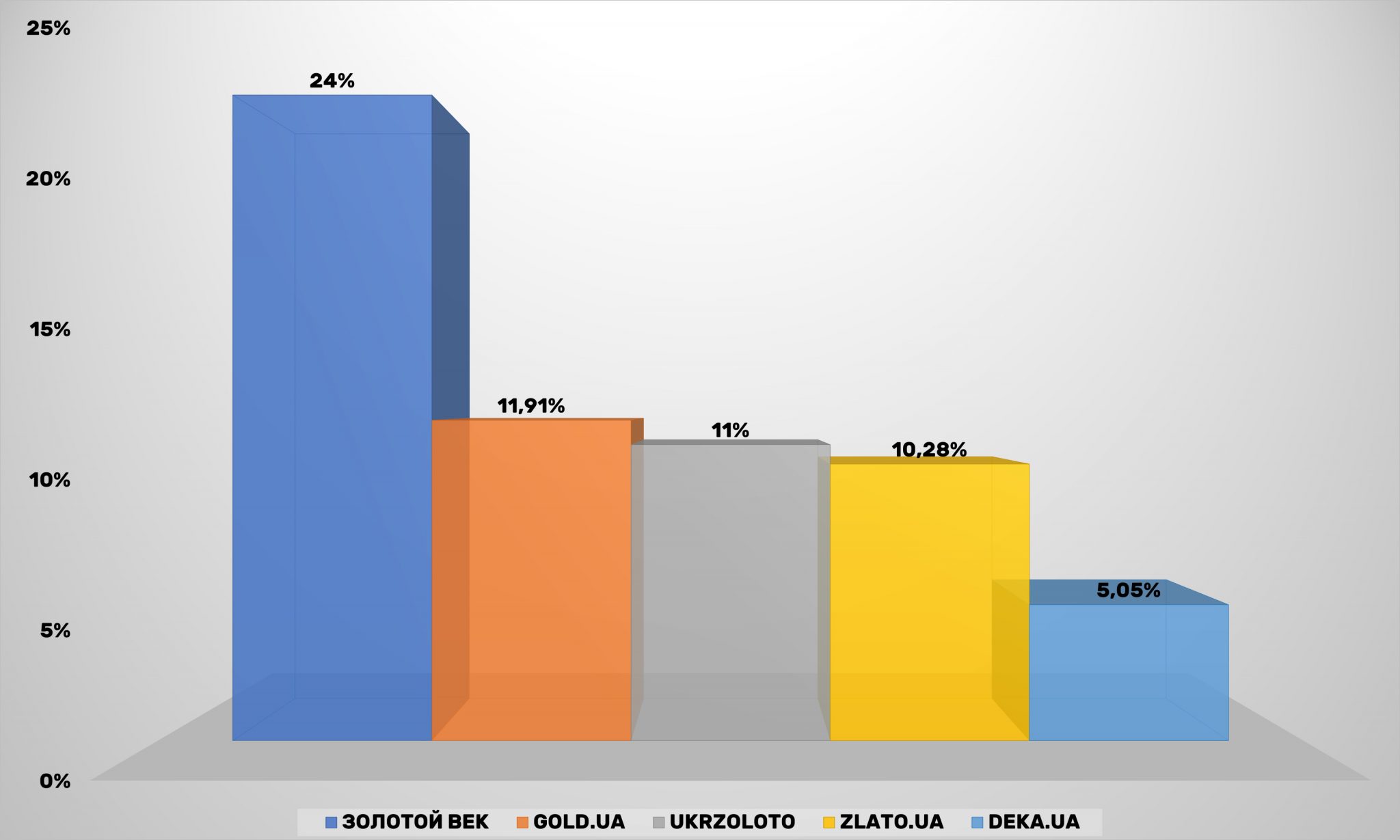

Jewelry retail

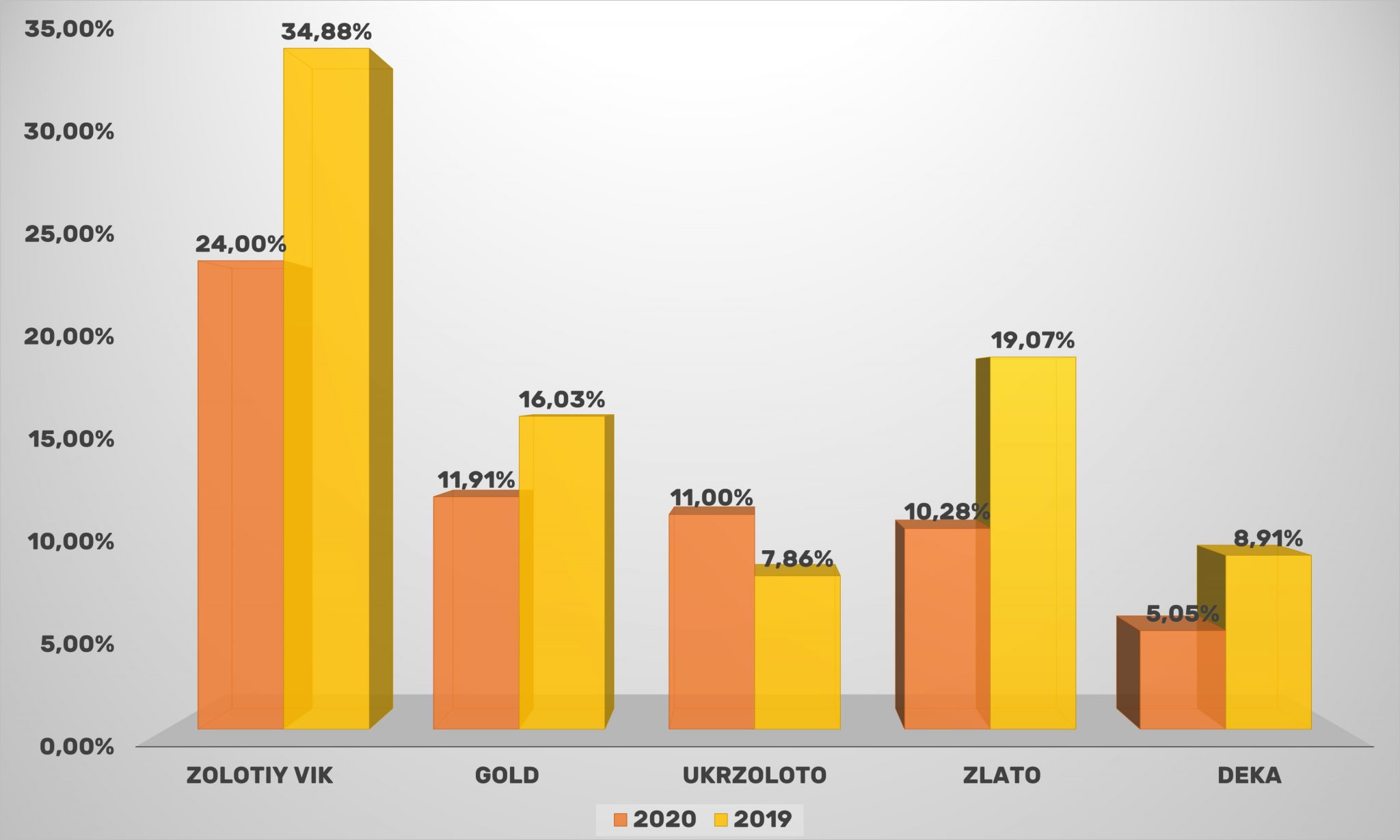

There are also permutations in this sub-segment of domestic e-commerce: a new player Ukrzoloto appeared in the Top-five instead of Oniks.ua, immediately taking the third place in coverage’ terms. Last year was not the best for buying jewelry, so the market leader Zolotyi Vik significantly reduced performance, which narrowed its gap from closest competitors. Only the newcomer Ukrzoloto showed good indicators, and all others recorded audience’ losses.

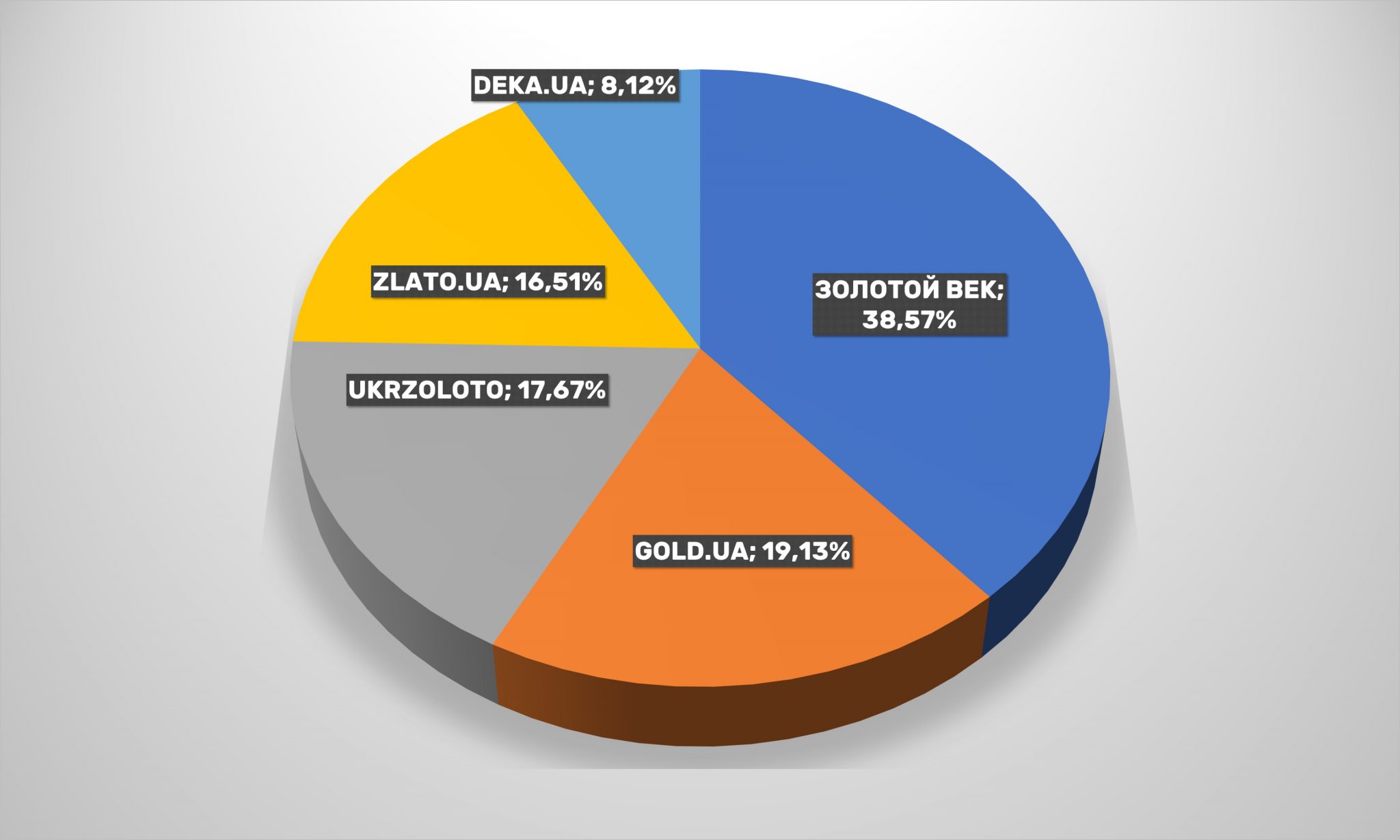

Now the “Big Three” of online-jewelry retailers in Ukraine looks like this: Zolotyi Vik, Ukrzoloto, zlato.ua. In total, it covers more than 75% of the audience among the first five online-jewelry and accessories stores.

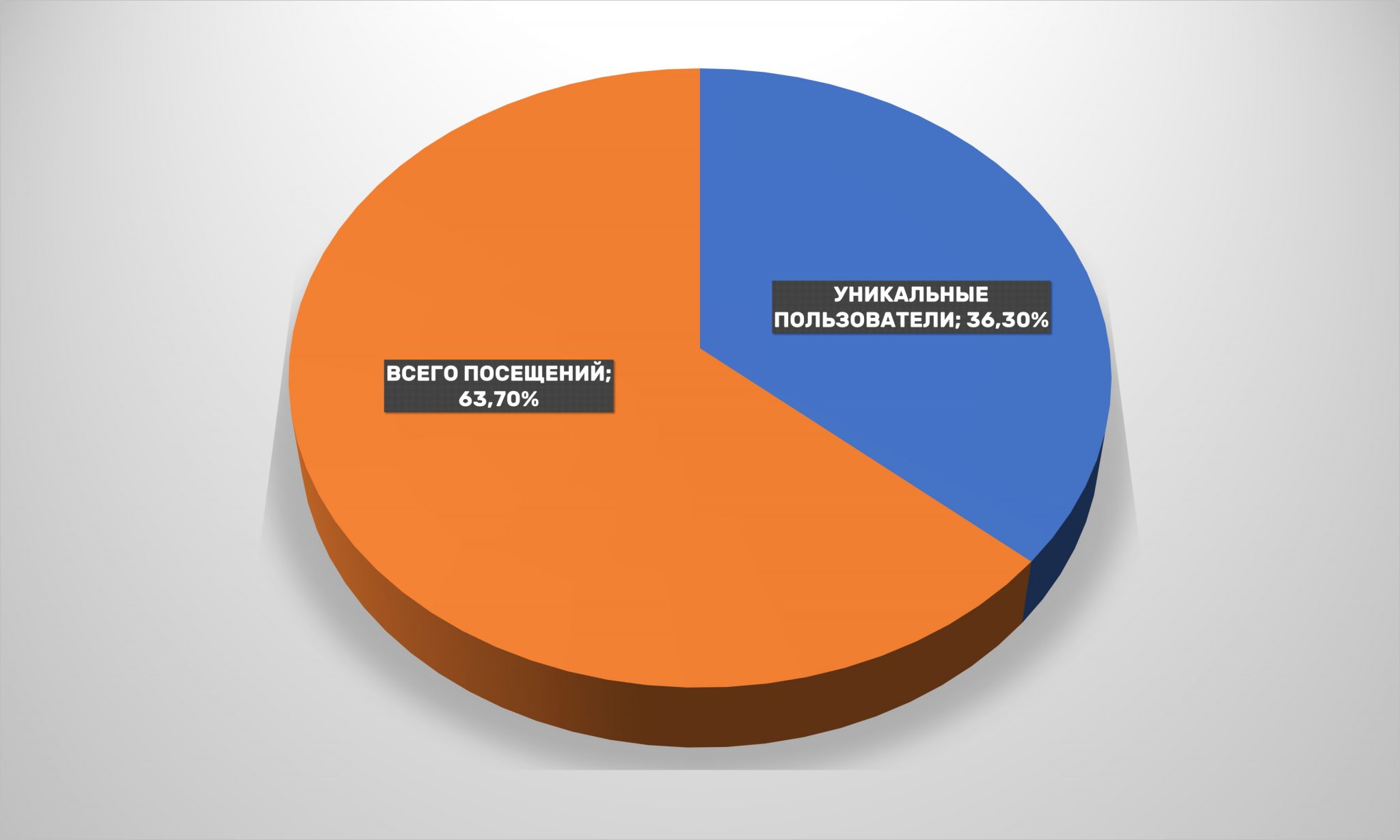

Moreover, more than two-thirds of users visit company websites more than once a year. For 12 months, the loyal audience has practically not changed.

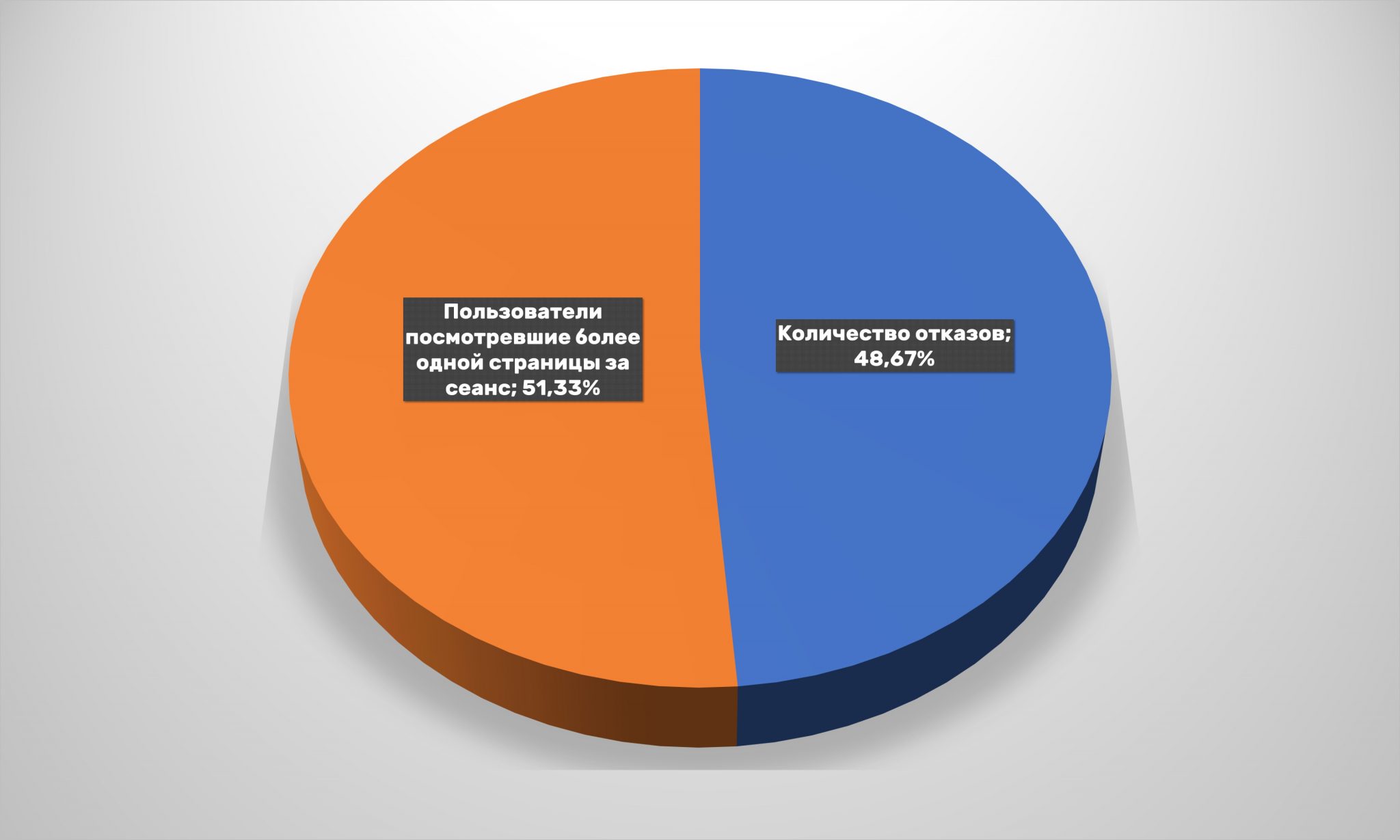

At the same time, retailers managed to stop the growth in the number of bounces, stabilizing this figure at around 49% potential buyers. But back in 2017, only 31.29% users left the portal of jewelry retailers from the first page. It seems that Ukrainians often just stopped by to admire creations of jewelers.

Transitions from search engines and from advertising results in it’s clearly stand out among visit’ channels. There are not so many direct calls. Most likely, users are looking for a product in google and similar systems, and do not go directly to retailer’s websites. SEO and search engine optimization for jewelry market players should come first. Nothing has changed over the year in this sense.

Although social media accounts for less than 3% of total traffic for online-jewelry and accessories stores, it should not be forgotten. Facebook is important, first of all, for jewelers, but YouTube has grown by only 1% compared to last year. This tendency is somewhat different from the general Ukrainian tendency, where the dominance of video services is again in trend.

The share of users who visit jewelry online-stores from mobile devices as well as in sports goods has slightly decreased – from 76 to 72%, which nevertheless is one of best indicators among all segments of Ukrainian e-commerce.

The age group of 25-44 clearly stands out among users who visit online jewelry stores. However, over 12 months, their share decreased from 59 to 47%. On the other hand, representatives of the older generation, especially those over 55, have become noticeably more active as in the segment of sports goods. Their share has more than doubled. This is who online-marketers and advertisers should bet on.

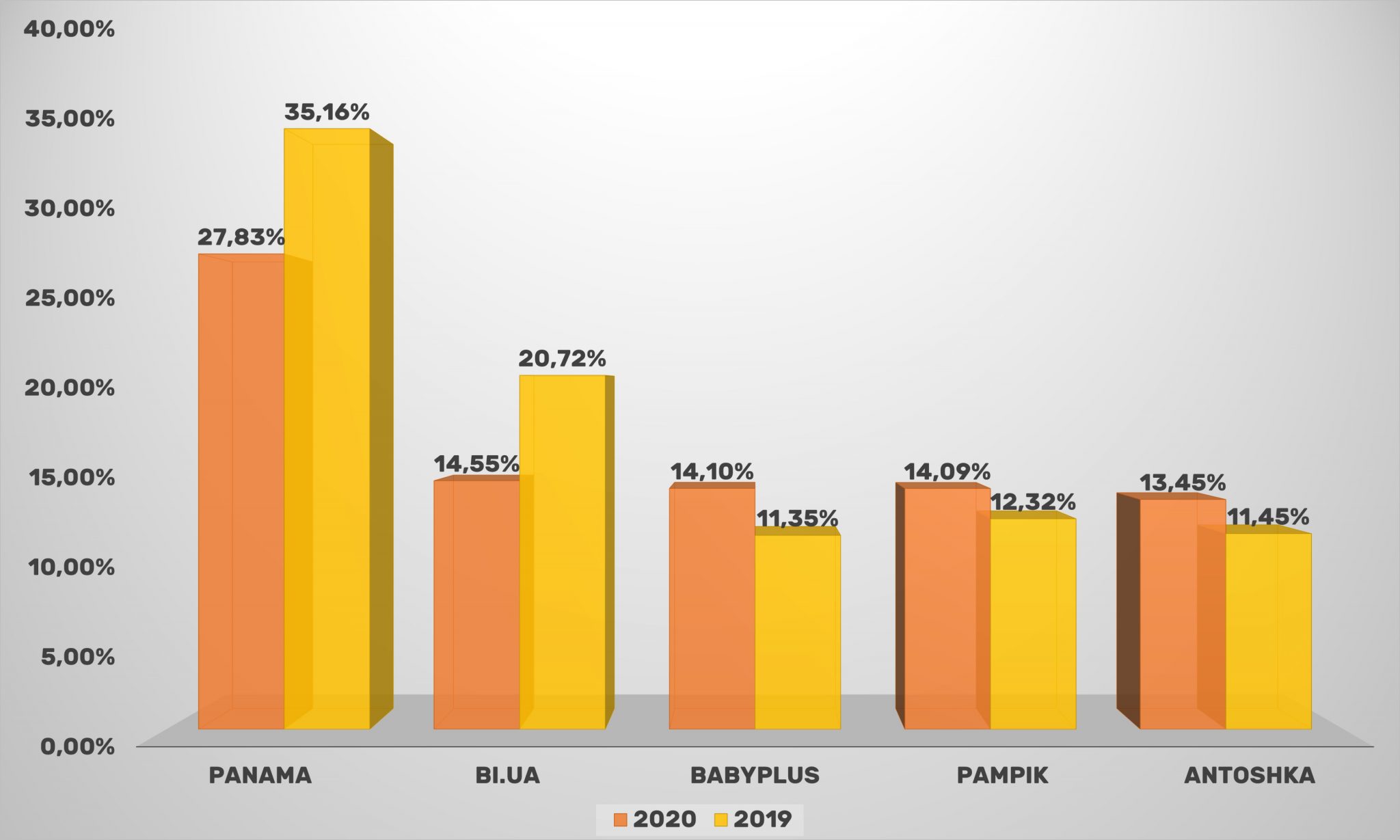

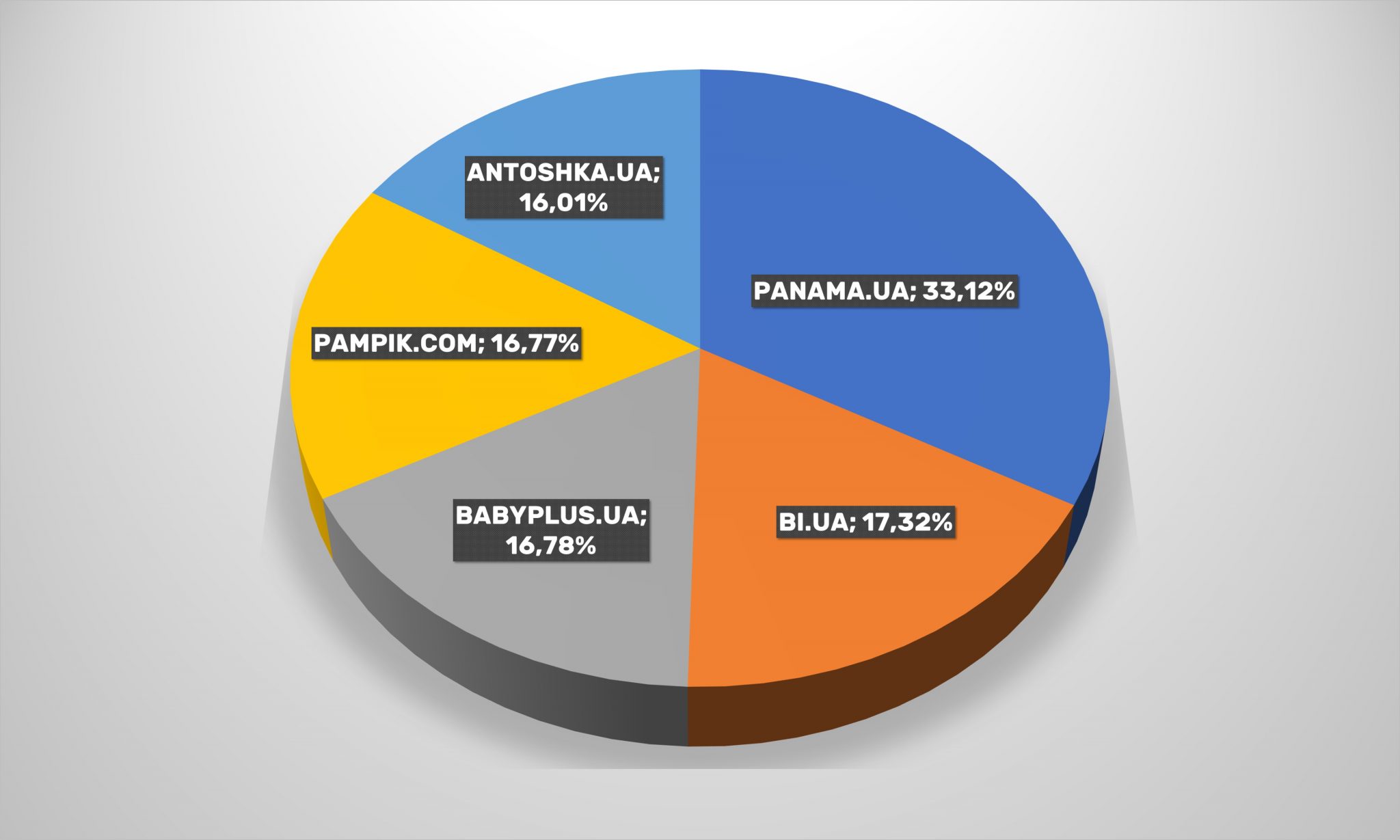

Goods for kids

There are no significant changes in the segment of online-retailers of goods for children. Is that babyplus.ua again pulled up to leaders, moving from fifth to third place. Old-timers of the market – Antoshka and Pampik – have also strengthened its positions. And last year’s leaders, Panama and Budinok Igrashok, albeit with losses, retained first and second places.

On the other hand, Antoshka and Budinok Igrashok are not classic online-stores, but omnichannel retailers, so for it the World Wide Web is only one of sales channels, although it proved its importance during the coronavirus crisis. Therefore, the fact that it is inferior in some parameters to companies presented only online is not surprising.

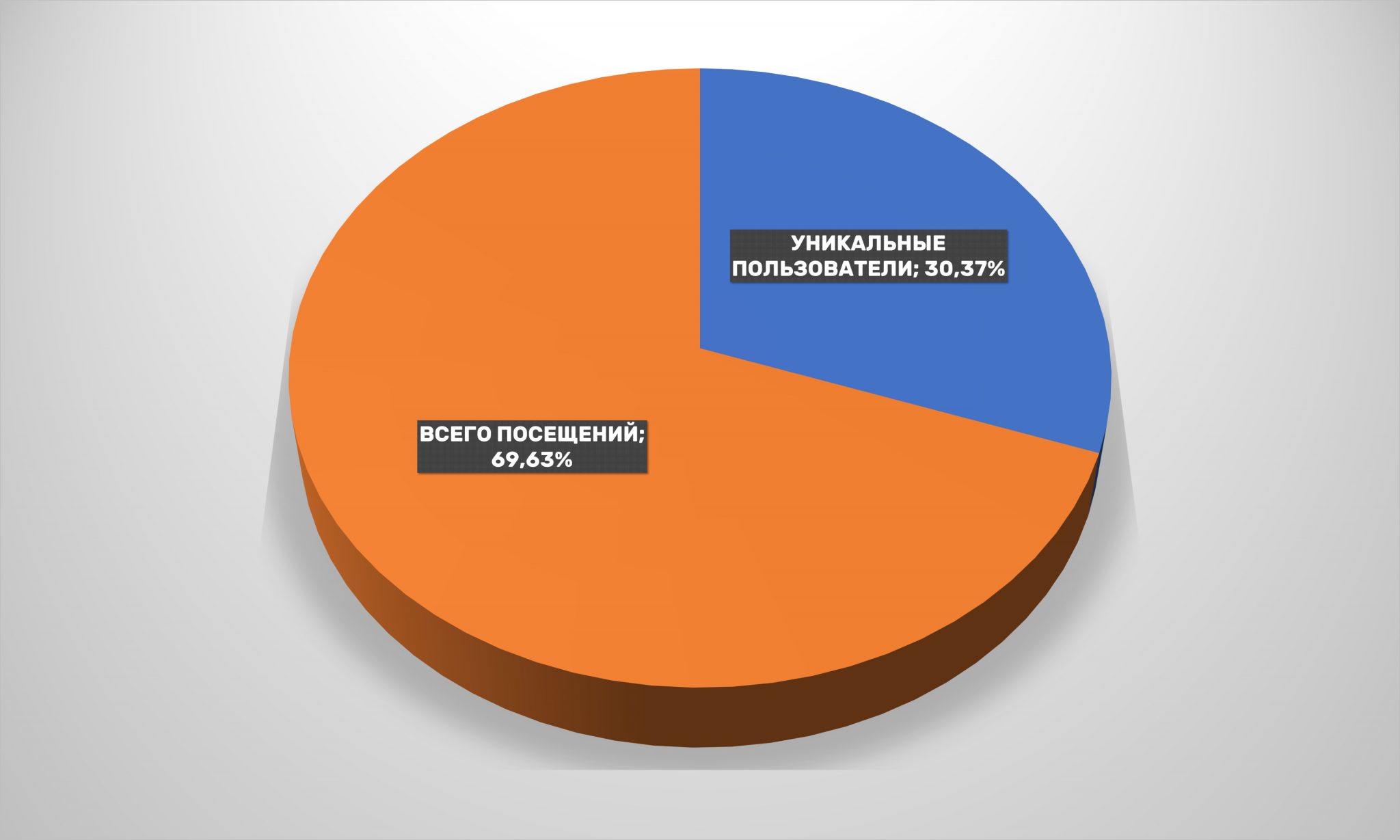

The number of repeat visits, and hence the loyal audience, has grown significantly over 12 months, while the number of unique users has decreased.

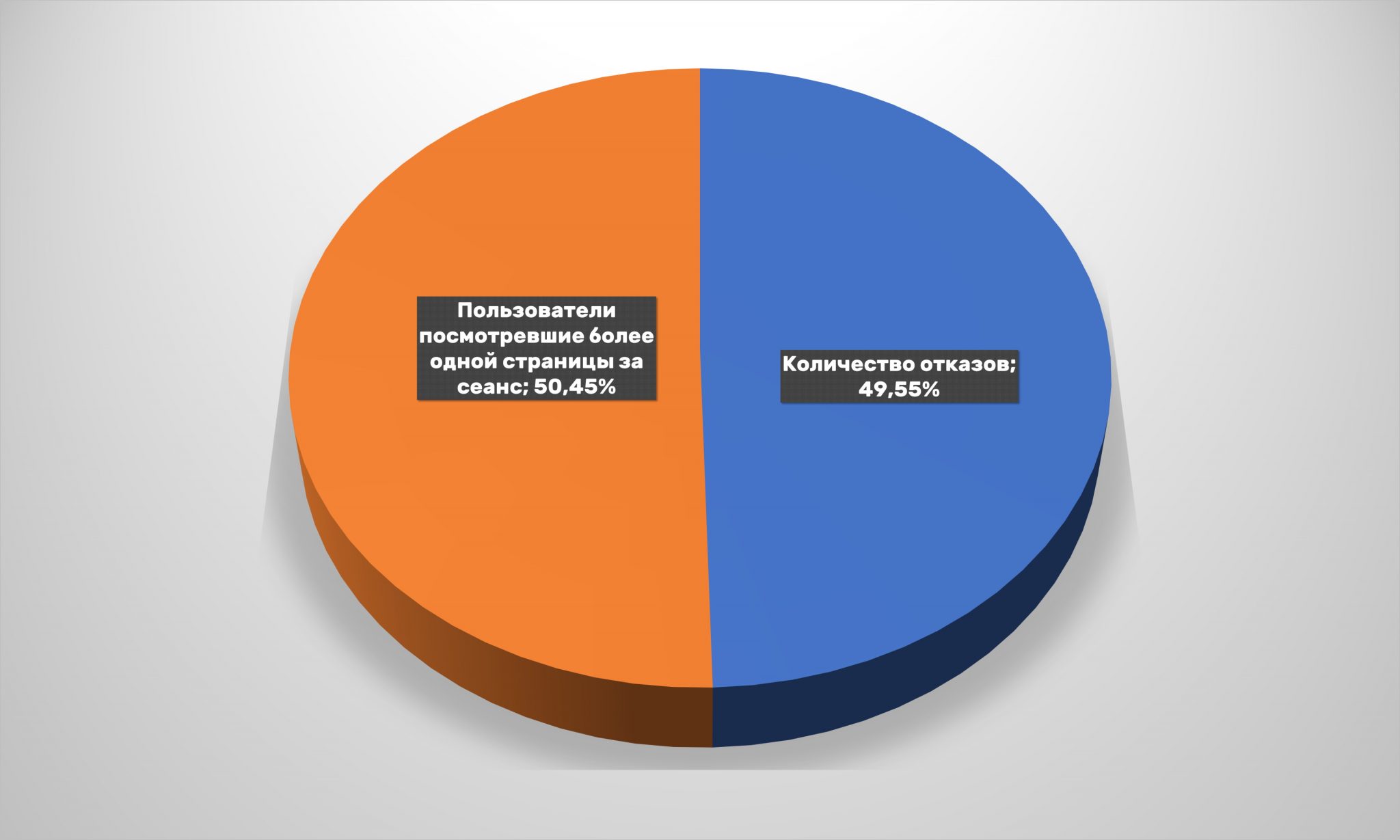

Also, the number of bounces, that is, visitors leaving the site without a purchase, has slightly decreased. But changes are not critical: about 50% of refusals are the norm for Ukrainian e-commerce.

If we compare main channels of customer visit to online-children’s clothing stores with 2019, the share of transitions from search engines has increased and direct visits have decreased. Retailers in this segment continue to increase paid traffic both through search engine promotion and direct advertising. It is in line with the mid-market trend.

And Facebook is losing its previous position relative to YouTube in the category of goods for children: now transitions from video hosting provide almost 46% traffic from social chains, and through Facebook – only 36%. But the share of conversions from Instagram has almost tripled, although now it is less than 3%.

There is also a decrease in the share of mobile device users compared to 2019, but this does not in any way negate the m-commerce and 4G’ onset.

This is not surprising, because main buyers of this goods’ category are people from 18 to 45 years old. Another thing is surprising. Older generations have become more active in the category of buyers of children’s clothes. Probably grandparents who buy goods for their grandchildren, as well as uncles, aunts and other relatives over 45 made up almost 35% of the audience.

Cosmetics and drogerie

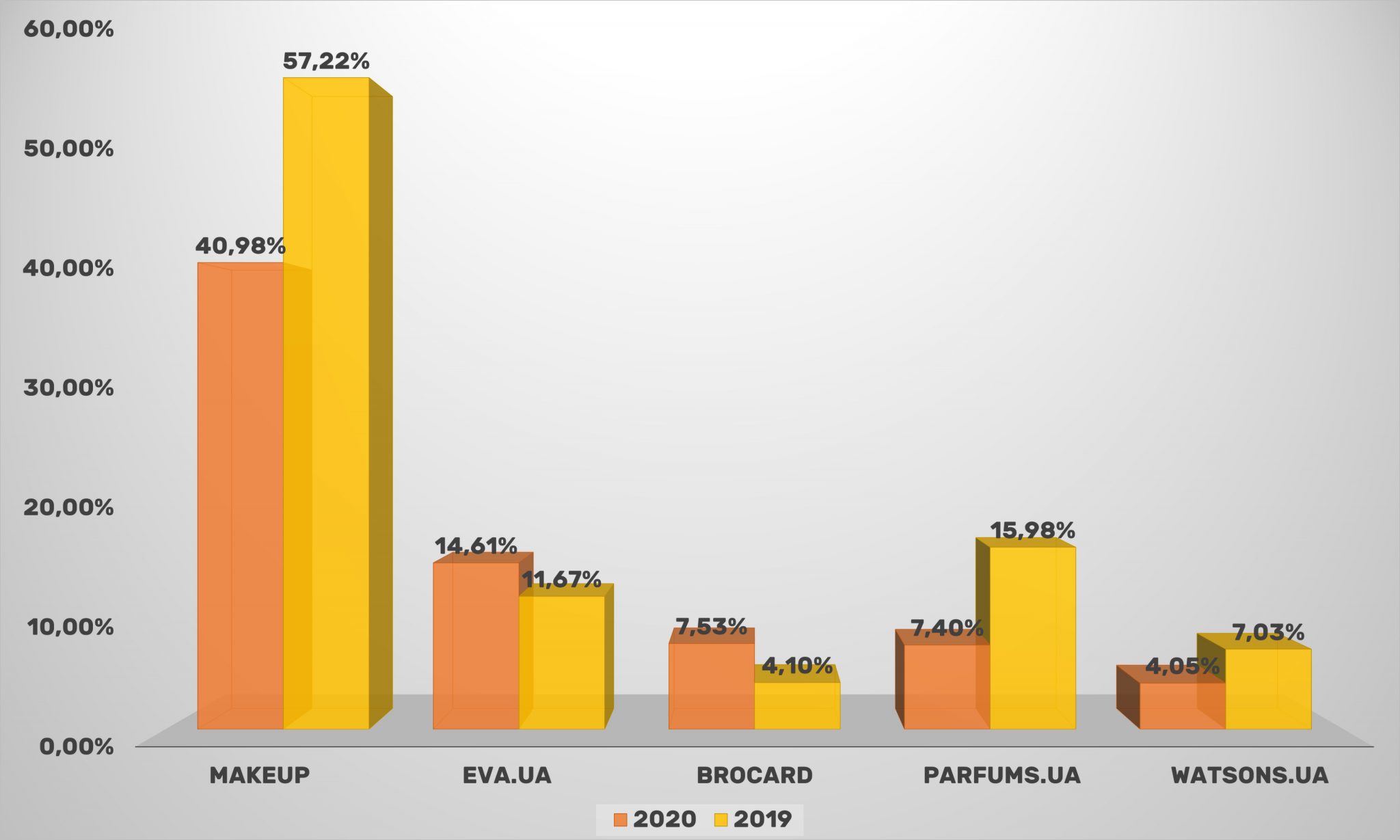

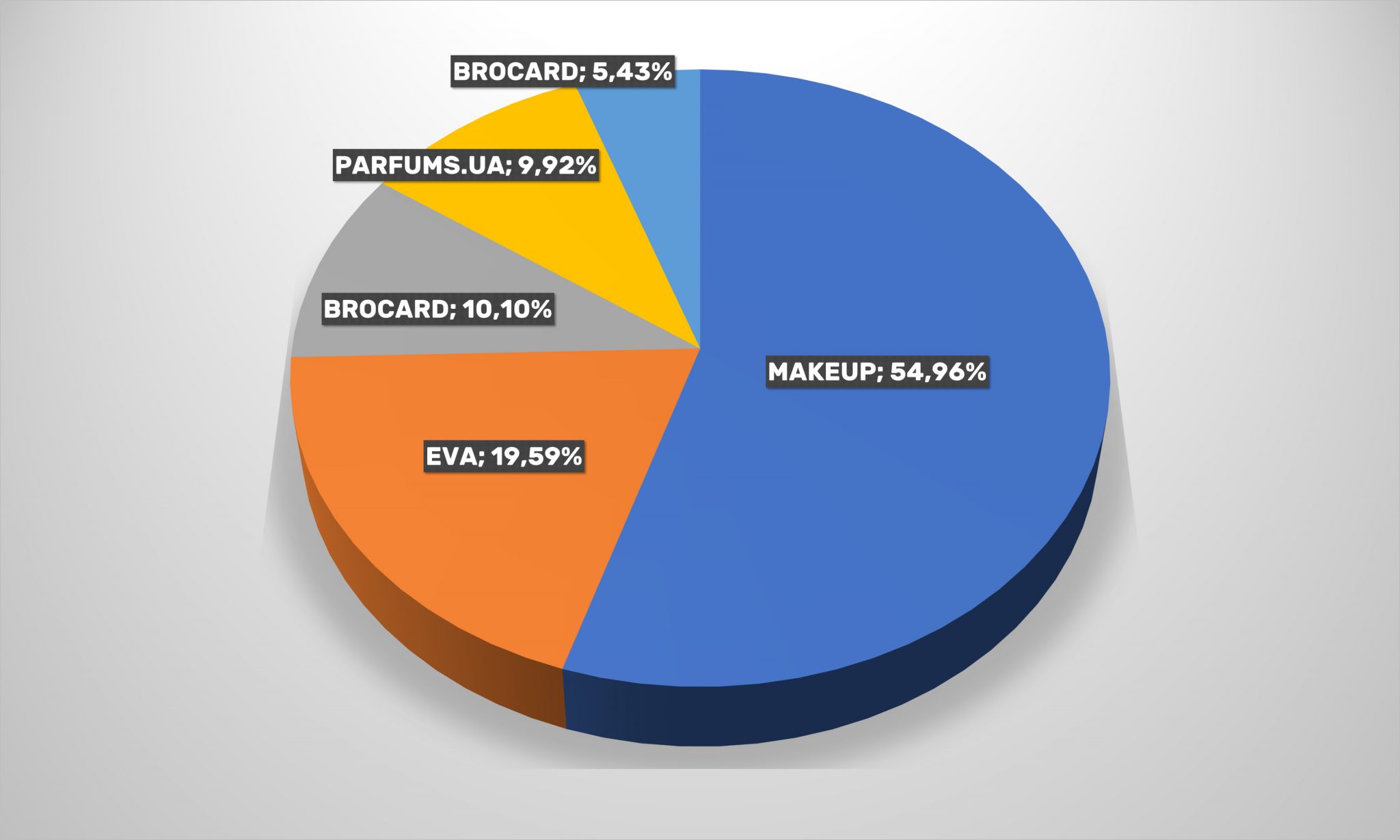

The composition of five leading retailers in this segment has not changed, although some players have lost its positions to more successful competitors. It is important to note that omnichannel retailers such as the largest offline health and beauty chain EVA and Brocard were able to gain a foothold in the Top-5 at the second and third places, beating traditional online-stores in its area. The unconditional leadership in the segment is maintained by makeup.ua, although it reduced its coverage to 41%. At the same time, parfums.ua, which exactly repeats the dynamic of the leader, dropped from second place immediately to fourth.

Nevertheless, makeup.ua out of the “Big Five” alone covers almost two-thirds of the audience, so the rest will be problematic to approach it, even taking into account the new distribution of players’ forces.

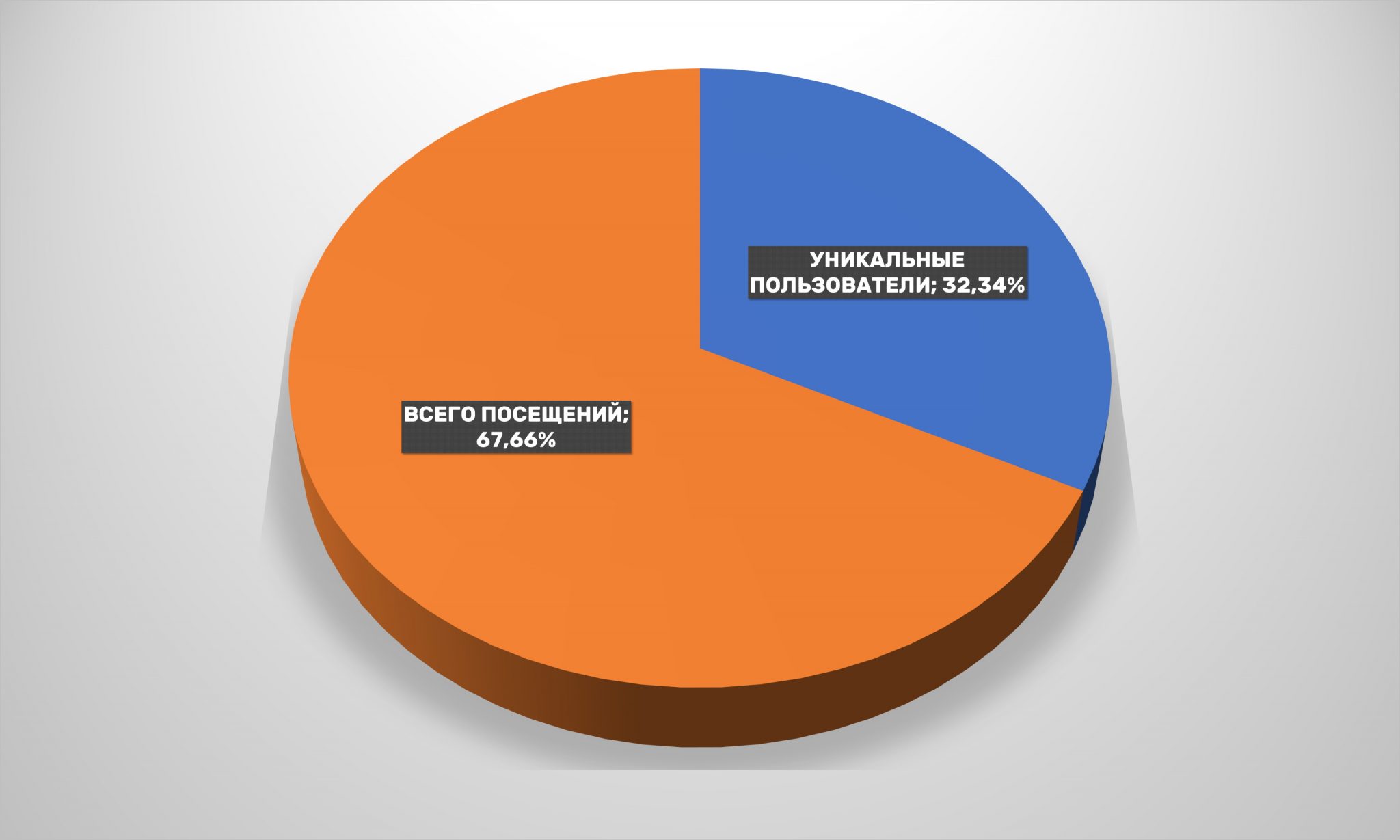

The buyers’ loyalty of drogerie online-stores can be envied by many – almost 68% repeat visits, which is about 5% higher than a year earlier. Stability is a sign of class in this case.

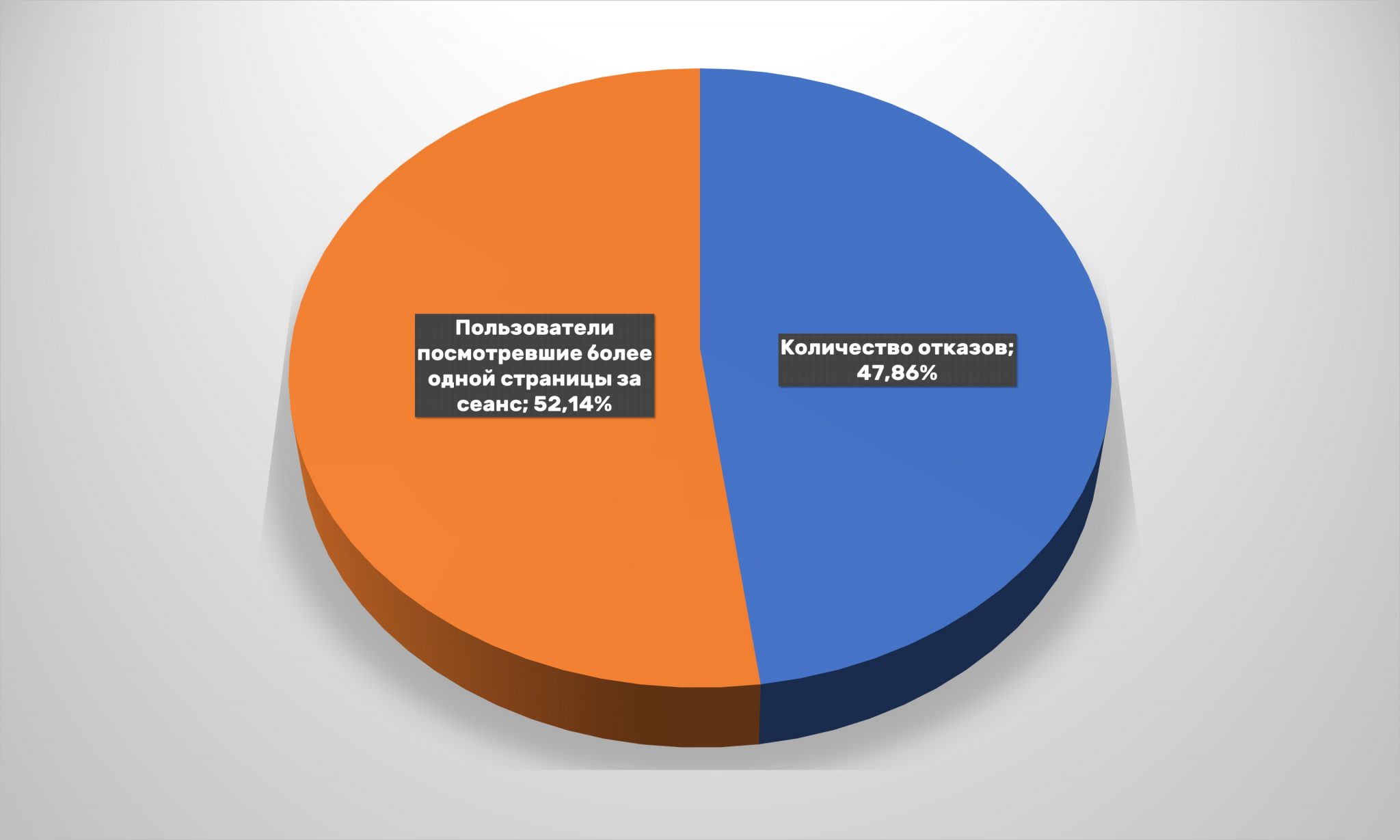

But the concern should be the increased number of refusals – 48%. There is a steady trend here for fourth year in a row.

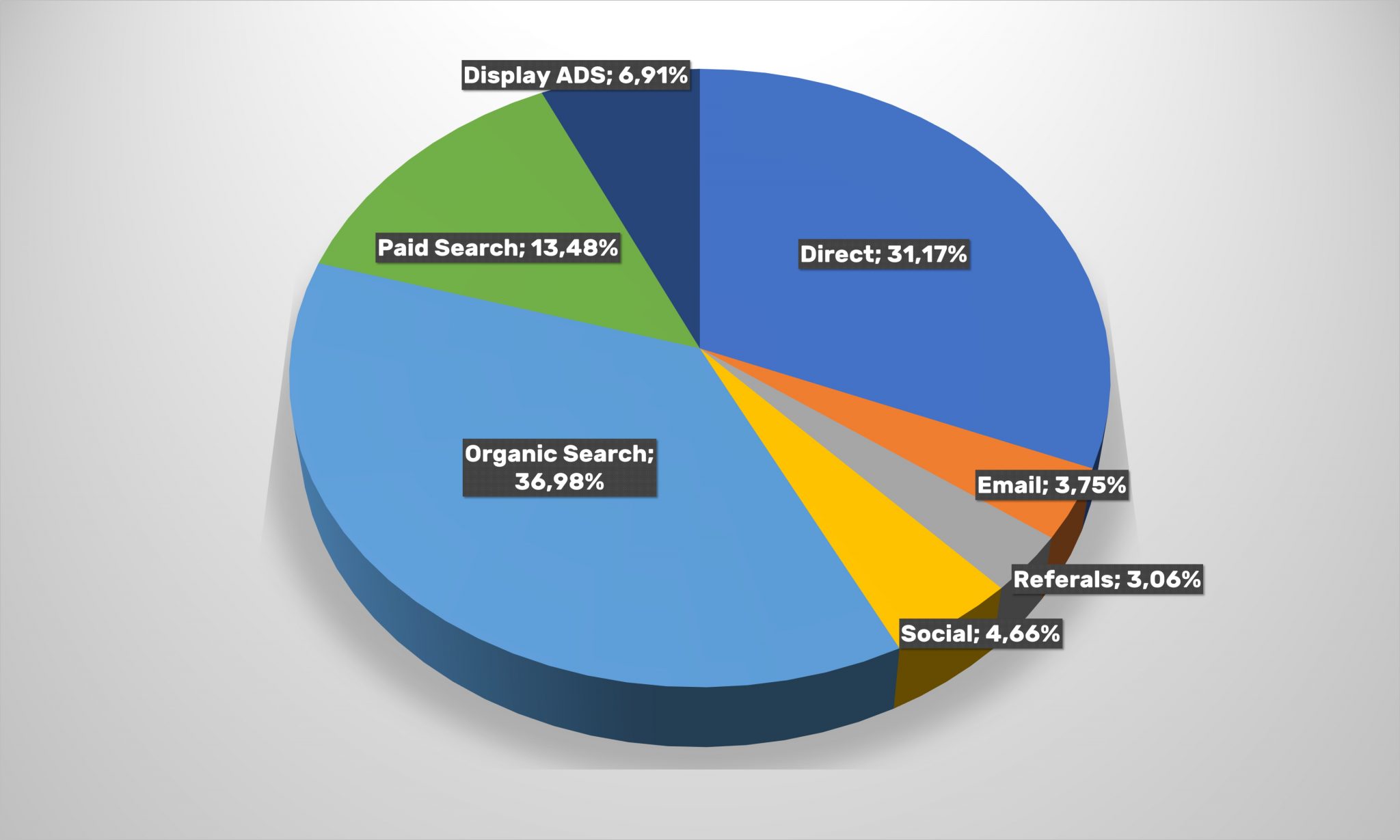

Main visit channels are traditional: organic search and direct visits. In total, it provides 68% traffic. The growth of paid traffic is also noticeable.

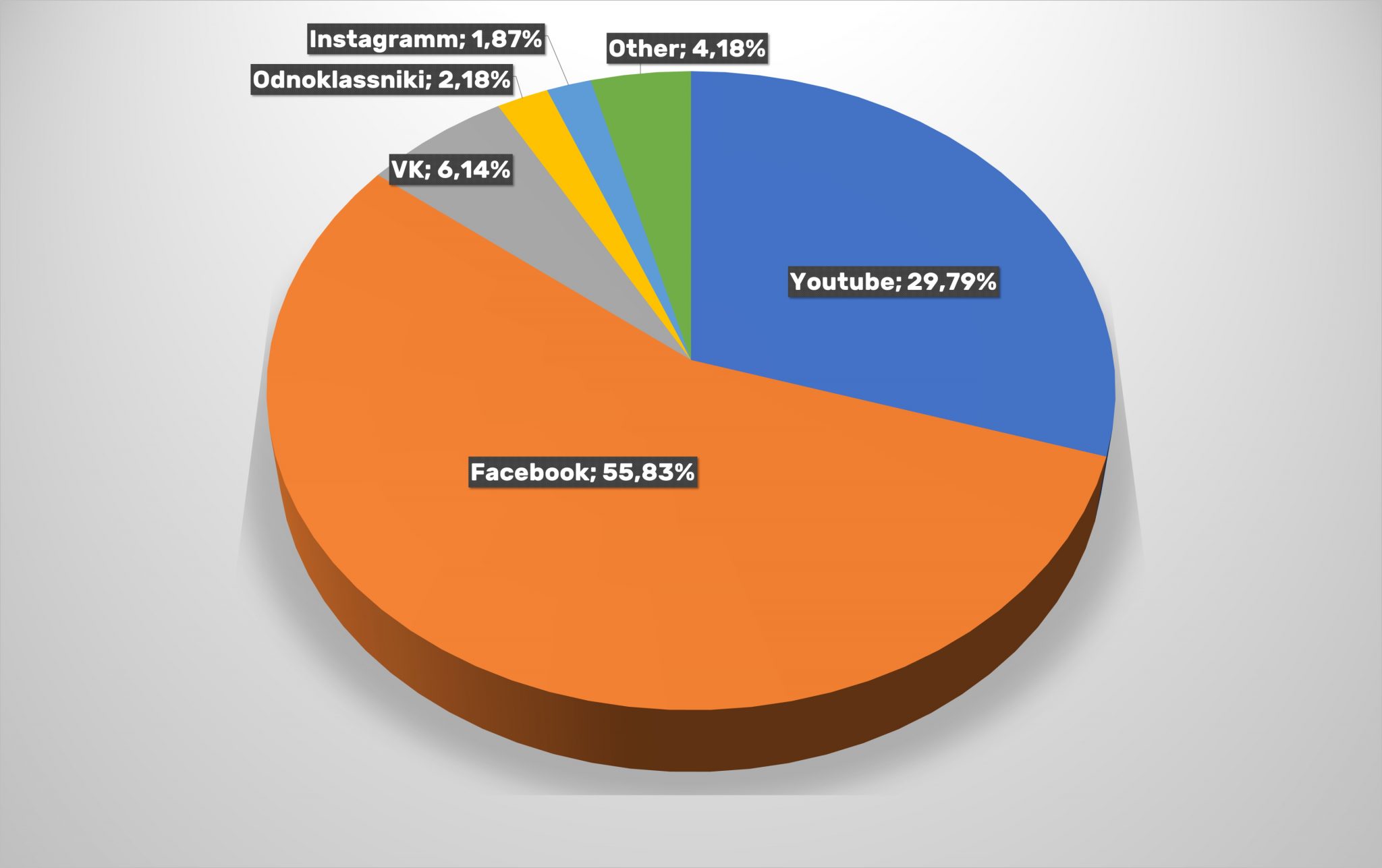

Facebook brings the lion’s share of conversions from social chains to online-retailers of the drоgerie segment – almost 56%. In this case, it is the most effective tool for attracting consumers to the site. The ratio of remaining channels remained practically unchanged.

The number of mobile device users has also remained unchanged compared to 2019, what rest of retailers from other segments might envy.

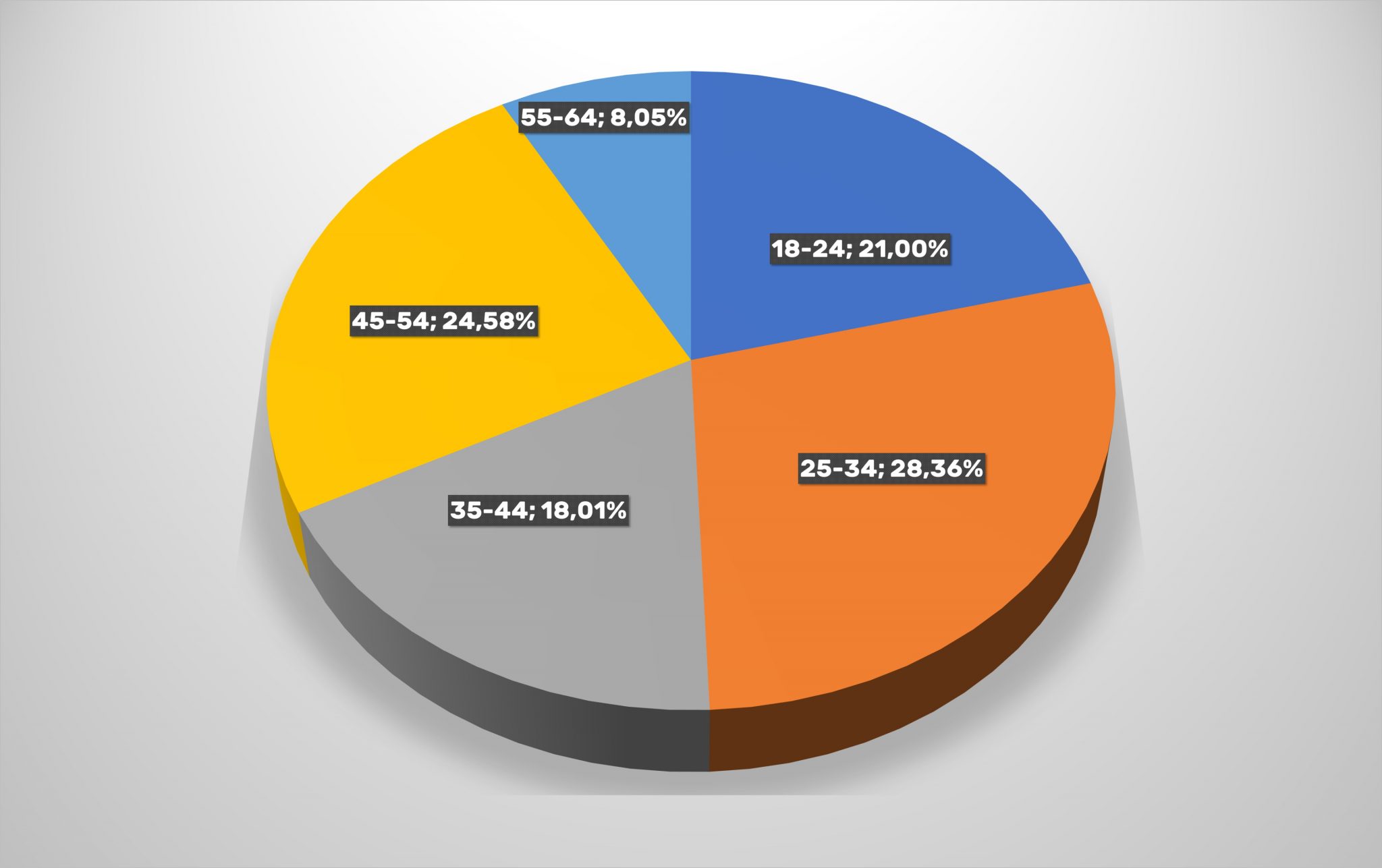

The age range of cosmetics and health products online-stores’ buyers is quite diverse. Almost all consumers buy different categories of products online in one way or another. Except for age 65+, the interest is caused by a sharp decline in the share of buyers from the 35-44 age category (from 33% to 18%) and an active growth of a younger audience.

Read also –

Special project “E-commerce UA”: how online-stores’ key indicators changed over the year